This week’s article is the next in a series of Guest Posts written by Howard Rogers, the Director of Natural Gas Research at the Oxford Institute for Energy Studies.

I published a paper in 2012 on the subject of CCS entitled (appropriately I thought) ‘Gas with CCS in the UK, Waiting for Godot?’. This line of research was prompted by a desire to get to the bottom of why such a potentially significant weapon in the quest for CO2 abatement, despite gaining the approval of all key climate change policy bodies, has to date not one commercial scale power sector application in operation globally.

Commercial vs technological challenges

The most common explanation is that of ‘technology challenges’. This is factually incorrect. Not only have the individual building blocks of the CCS chain been successfully employed in the upstream, petrochemical and refining sectors for decades, but commercial scale CCS chains have been deployed in the fields of natural gas processing and fertiliser manufacturing.

Whilst technological progress would certainly improve efficiencies and lower costs – especially in the CO2 separation stage – there are no barriers to making the process work, at scale, with coal or gas – fired generation plant. This is true whether we are considering pre-combustion (where the coal or gas stream is reacted with steam to form a mixture of CO2 and Hydrogen) or post-combustion (where coal or natural gas is used in a conventional generation plant and the CO2 extracted from the flue gas before it is vented in a stack). Pre-combustion configurations tend to require more complex process plant and lack the operational flexibility of post-combustion alternatives. This is likely to be important in the future where coal or gas fired generation with CCS could be required to provide flexible buffering or back-up to intermittent wind and solar generation.

The question of cost

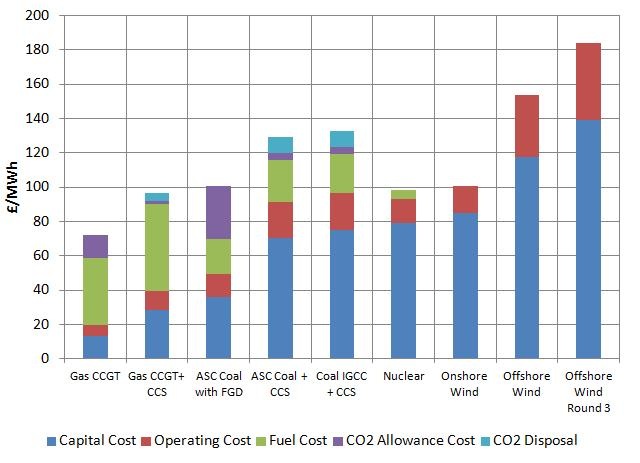

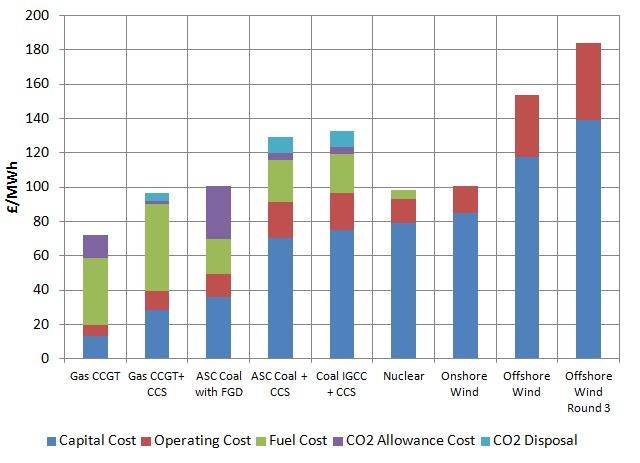

We therefore come to the question of generation cost. As the following figure shows, the ‘levelised cost’ of generation from gas with CCS is similar to that of nuclear and onshore wind. Even the more expensive coal with CCS is more economically attractive than offshore wind. So if gas with CCS is similar in terms of generation cost with ‘mainstream’ low carbon generation technologies, why has it not been adopted at a commercial scale to date ?

Here I believe the issue is one of the commercial complexity of establishing a power generation with CCS ‘chain’. In order to successfully construct a commercial scale power sector CCS scheme it is necessary to ensure that the commercial arrangements for the power generation and CO2 separation, CO2 transportation and CO2 storage stages are covered by a ‘web’ of commercial agreements which appropriately apportion risks and rewards along all stages of the CCS chain. As current wholesale power market prices are set by unabated fossil fuel generation with currently only weak CO2 cost signals, it would be necessary that governments provide a level of assurance, not just on future power generation revenue, but more specifically on the difference between generation revenue and fuel costs. This is a level of complexity which has never yet been attempted in power markets which until recently have been run under an orthodox market framework.