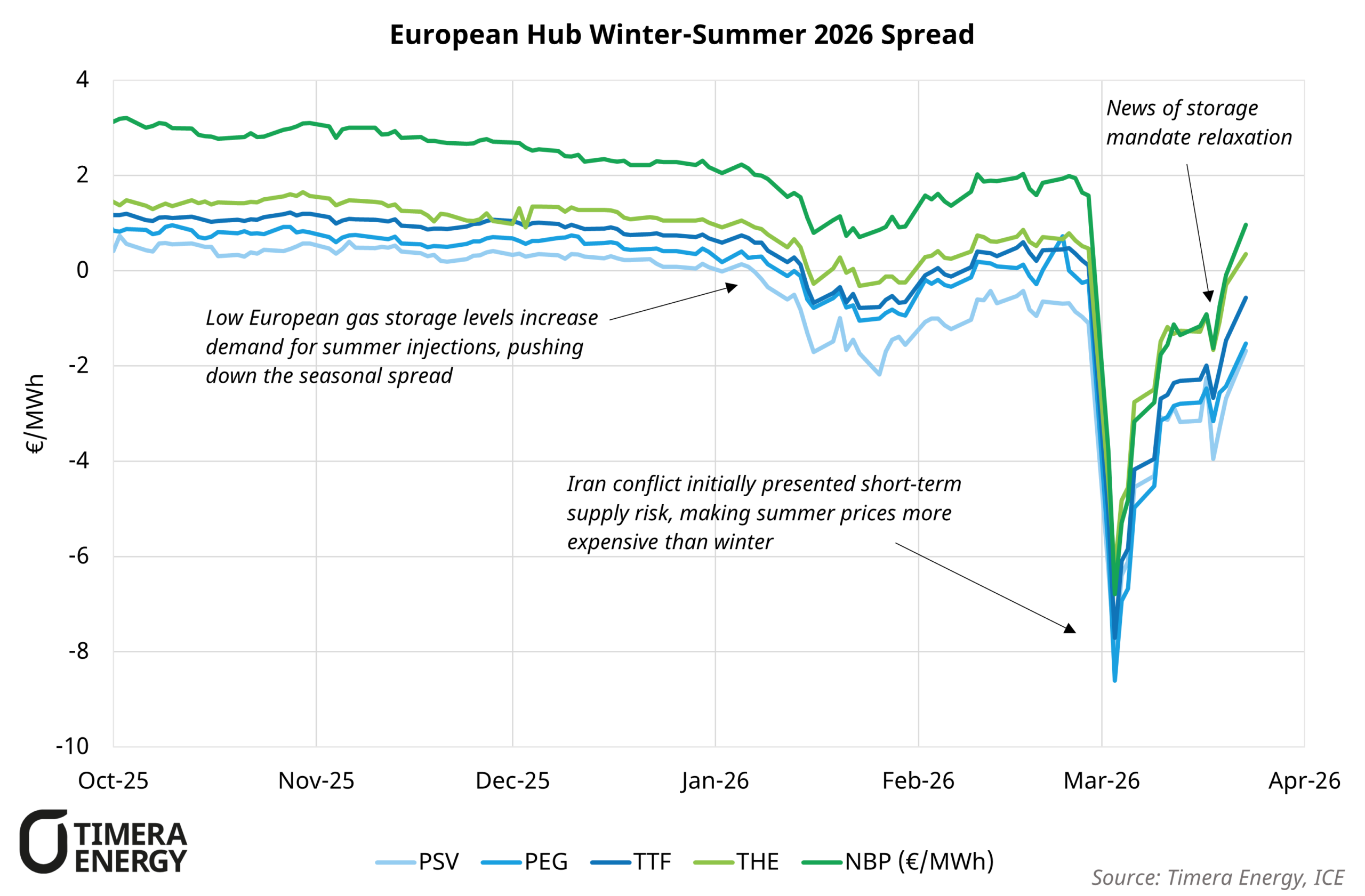

The conflict involving the US, Israel, and Iran initially drove a sharp fall in European gas hub seasonal spreads. The TTF winter summer 2026 spread fell to a low of negative €8.60/MWh on the 3rd March, as markets reacted to the closure of the Strait of Hormuz.

At the outset, the disruption was priced as short lived, with the impact focused on prompt supply. This pushed summer prices above winter, inverting the seasonal spread. However as the situation has evolved, the market has begun to price a more prolonged disruption as Qatari LNG production suffered damage, with further dated contracts strengthening relative to prompt.

A negative winter summer spread implies that the traditional storage trade used to hedge a seasonal gas storage asset in Europe, buy cheap in summer, sell higher in winter, becomes loss making. As a result, there is limited commercial incentive to refill storages. This dynamic has been observed repeatedly, particularly when EU mandated storage targets place overt pressure on summer pricing.

More recently, the EU has given verbal instructions to member states to adjust their mandated fill level from 90% to 80% between the 1st October and 1st December an adjustment permitted under the current mandate during periods of “unfavourable market conditions”. This easing of policy, combined with rising expectations of tighter winter supply on more persistent Middle Eastern disruption, has supported a recovery in Winter Summer 2026 spreads toward zero across European hubs.

Both NBP and THE Winter Summer 2026 spreads have returned to levels that allow for forward hedging of storage capacity (disregarding cycling costs), settling at €0.96/MWh and €0.35/MWh respectively.

If you would like to understand how the conflict is shaping European market prices and storage asset value, or would like to explore our outlook for storage value, please reach out to Arthur Finch (Analyst, European Gas & Power) at arthur.finch@timera-energy.com