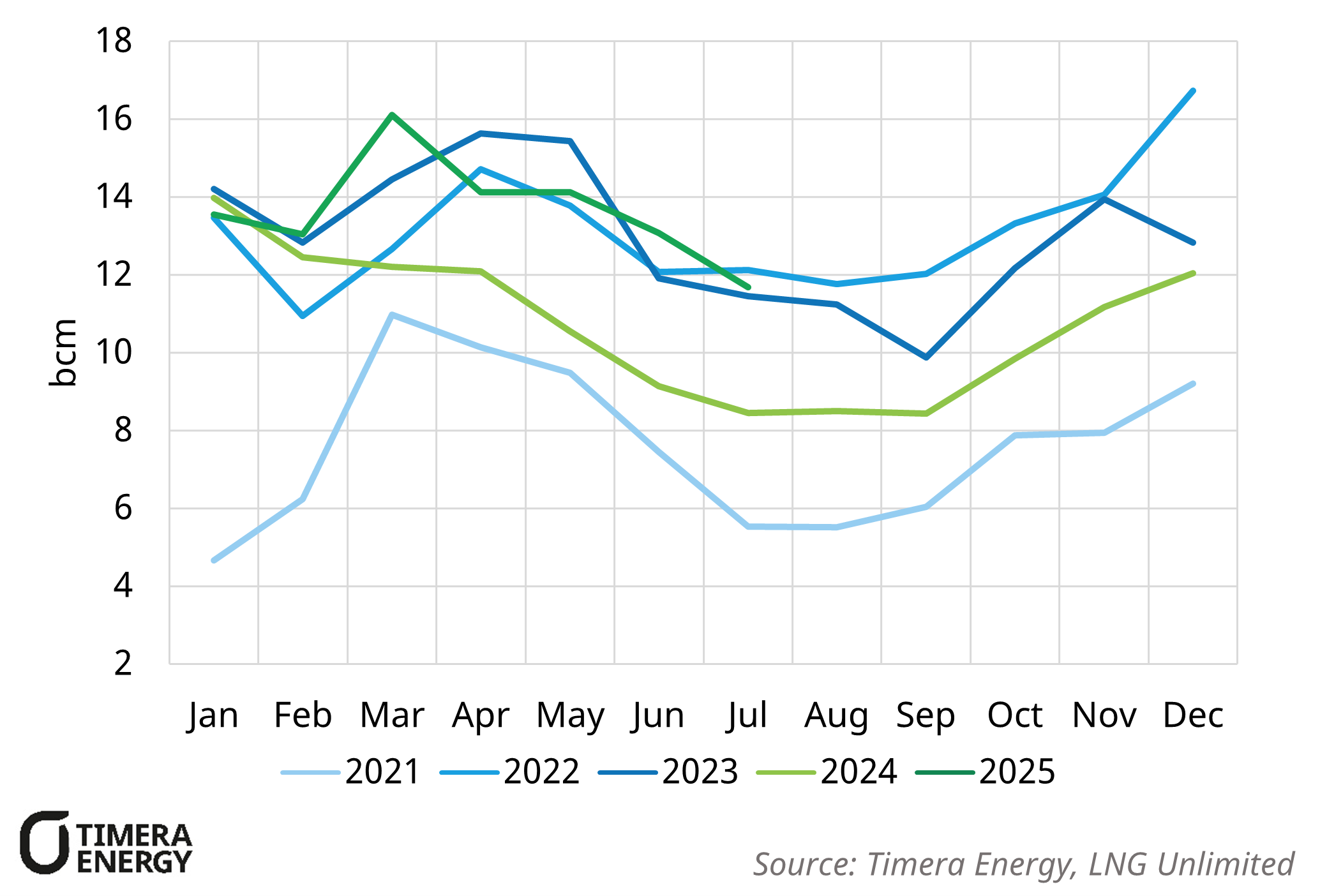

Through the first seven months of 2025, European LNG imports have increased ~21% year on year and are trending in line with record levels seen in 2022 and 2023.

This comes on the back of stronger winter demand and a reduction in Russian pipeline flows following the expiry of the Ukrainian transit agreement at the end of 2024.

Stronger gas demand over winter accelerated underground storage withdrawals, increasing the need for higher LNG imports over summer to support both increased injections and to offset RU piped losses.

Summer to date, injection rates have been supported by stronger LNG receipts, with Apr-July deliveries up 12.7 bcm year-on-year. This is helping keep the EU on track to meet the proposed 83% storage threshold, and has narrowed the 2025 storage deficit vs 2024 from ~25 bcm in early April to ~17 bcm by late-July.