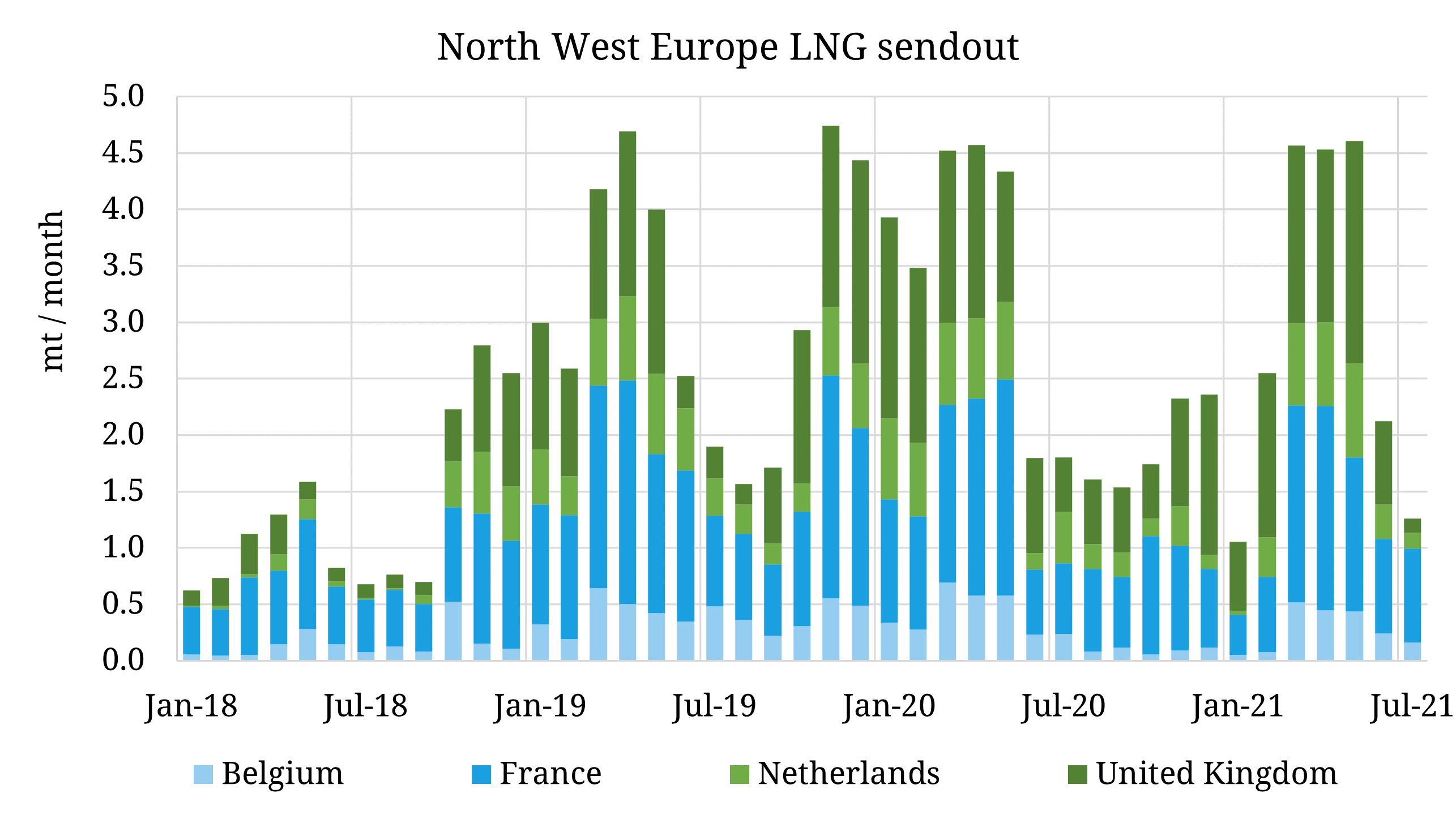

While soaring TTF prices have had the desired impact on the power generation stack in Europe, reducing demand from coal to gas switching, they have not had a similar impact on increasing share of LNG imports. High Asian demand in peak summer has instead seen JKM maintain a sufficient premium to attract marginal LNG supply away from Europe (with cargoes changing hands above 16 $/mmbtu), seeing July sendout in the North West European sink drop by over 70% from May to lows not seen since 2018, and 30% below 2020 levels heavily influenced by tank-top fears and US LNG shut ins.