Since the outbreak of war between Israel, the United States and Iran over the weekend, only a limited number of LNG tankers already in transit have passed through the Strait of Hormuz. The Strait currently appears effectively closed to commercial shipping.

QatarEnergy has also announced the halt of LNG production at its Ras Laffan facilities. This combination represents a severe disruption to global gas supply, with global gas prices moving sharply higher in response.

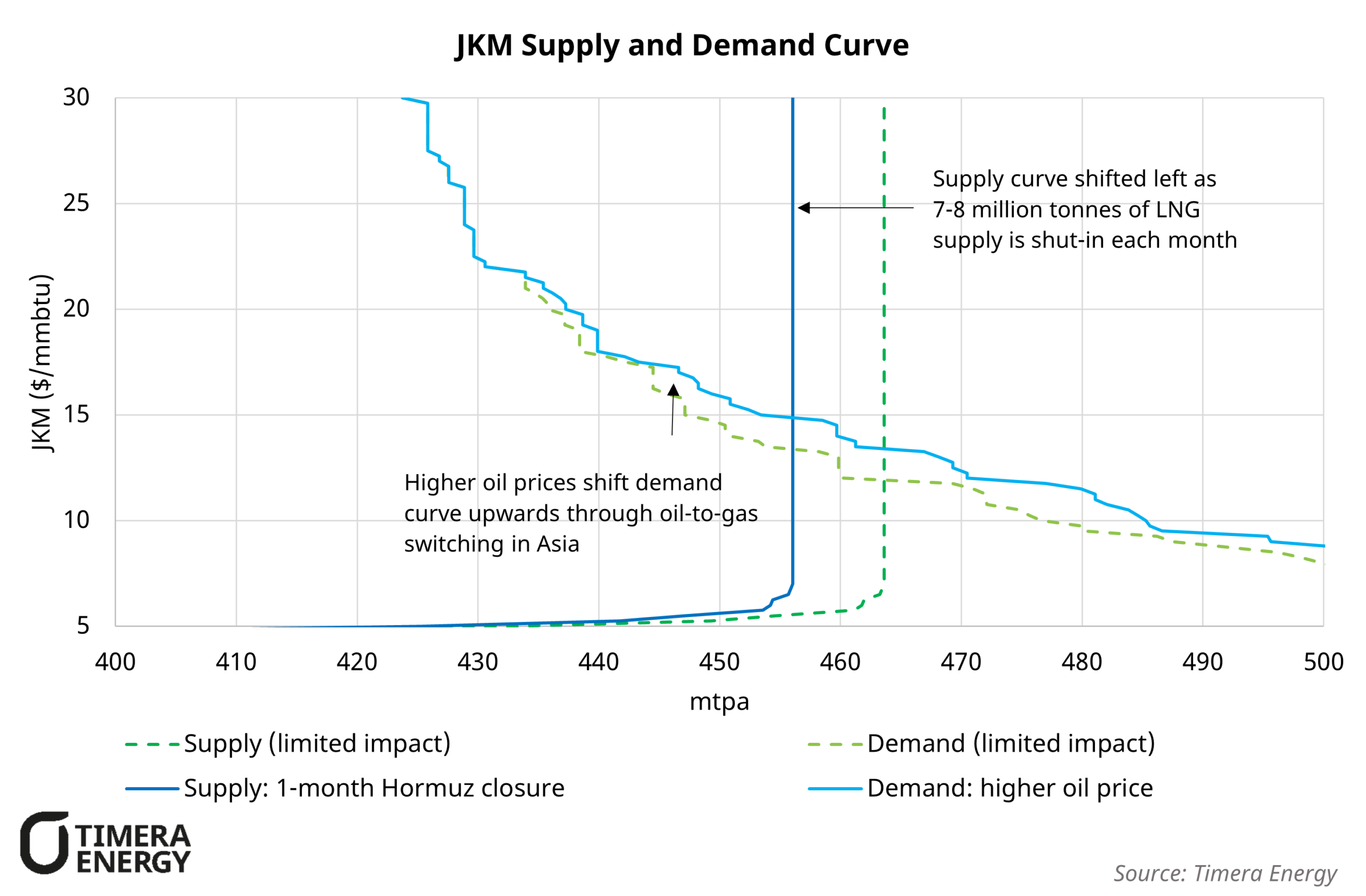

The Strait of Hormuz is a critical global energy transit corridor. All Qatari and some Emirati LNG must transit the Strait to reach global markets. Closure effectively removes more than 70 mtpa of LNG supply (~15% of total supply). This represents a potential shock to gas supply comparable in scale to the loss of Russian pipeline exports to Europe in 2022.

Timera’s 2026 global gas market supply and demand curves, charted in this piece, help to illustrate the potential impact. Stranding Qatari volumes shifts the global supply curve to the left, resulting in higher clearing prices. At the same time, higher Brent prices shift the LNG demand curve upwards, with oil linked switching in Asia currently close to the margin.

The key uncertainty is duration. This includes both the length of a full closure of the Strait and the time required to see export flows sustained at normal levels given the risk of damage to infrastructure and continued disruption to shipping lanes.

Additional risks remain material. Further regional supply disruption, including Israeli gas field shutdowns, Omani LNG production impacts or interruption to Iranian pipeline exports would tighten balances further.

On the basis of the current state of play, we highlight the following key implications for global gas markets:

- Increased competition for available spot cargoes will tighten balances and lift prices across all consuming regions, as reduced supply is cleared through demand destruction at higher prices. Tightness is likely to persist beyond the immediate disruption period, with lower storage levels pushing higher prices along the curve.

- Upside risk is asymmetric, particularly in the near term. With European storage around 30 percent full, reduced buffer capacity amplifies price sensitivity. As seen in the chart, incremental supply is effectively inelastic in the short term, making prices highly responsive to marginal demand shifts. A late season cold spell in March or early April could trigger extreme price spikes.

- As Asia is the primary destination for Qatari LNG, it will need to price above Europe to attract incremental flexible volumes, supporting wider JKM versus DES NWE spreads.

- Global LNG loadings will fall while Qatari exports remain offline, putting downwards pressure on spot charter rates if reduced loadings persist and potentially limiting the extent of JKM versus DES NWE spread widening.

- In Europe, reduced LNG inflows will lower utilisation of regasification capacity, softening DES NWE versus TTF spreads. However, a later normalisation of exports combined with stronger summer refill demand could see regas constraints re-emerge more acutely.

We will release a more detailed assessment of the range of potential outcomes later this week, drawing on our stochastic global gas market modelling framework.

In the meantime, please contact david.duncan@timera-energy.com with any questions.