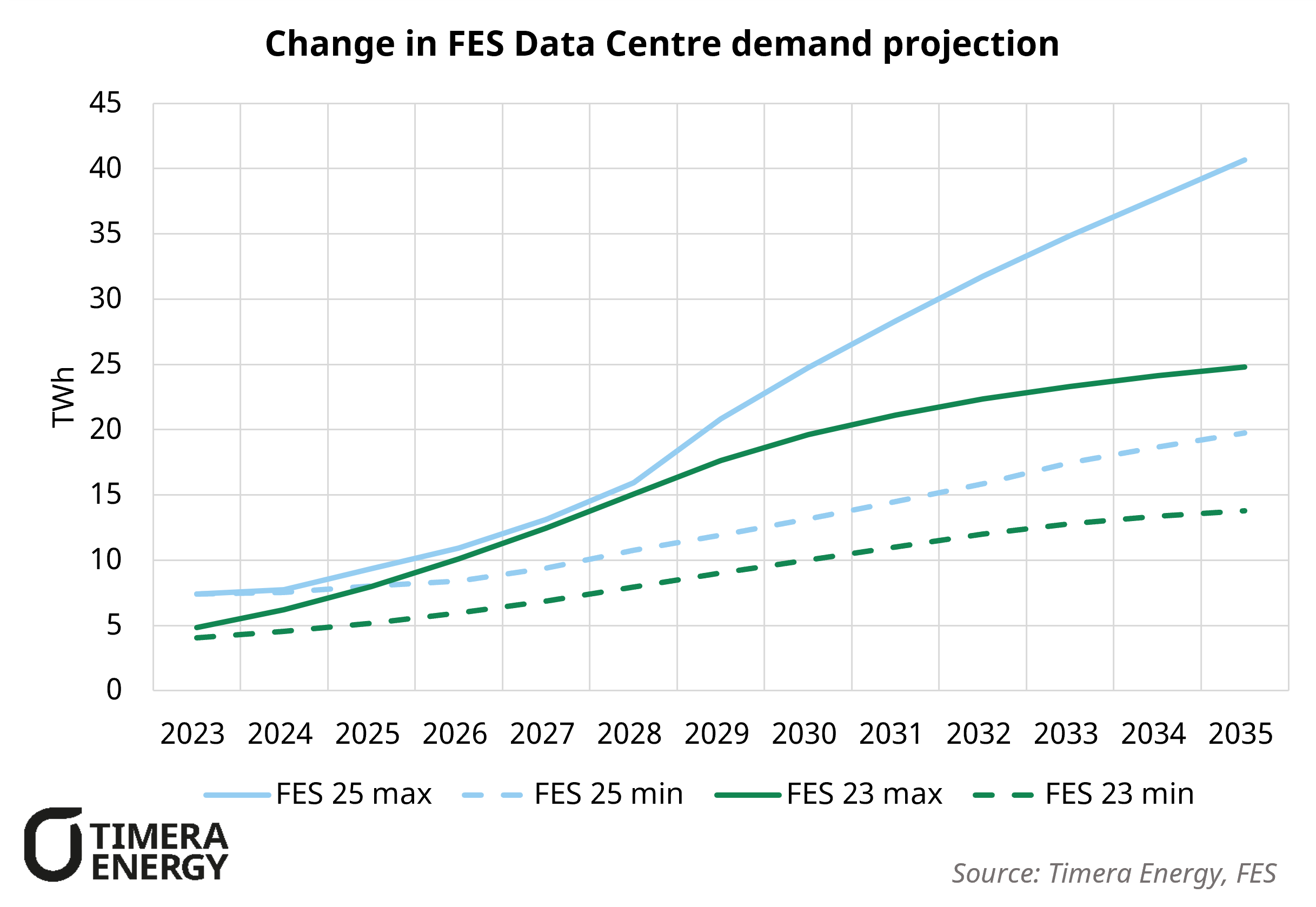

Data centre demand is accelerating across Europe as hyperscalers commit billions of capex to support AI growth. GB is no exception: successive Future Energy Scenarios (FES) have revised data-centre demand higher year-on-year, reflecting faster rollout as AI expansion intensifies. London is now one of Europe’s largest data-centre hubs, with ~1.2GW already operating but the key question going forward is how quickly pipeline capacity can secure grid access and convert into connected load.

In GB, the near-term constraint is grid access. The demand queue has ballooned and includes a large volume of projects that may never progress. Contracted offers reportedly rose from 41GW (Nov-24) to 125GW (Jun-25), with Ofgem identifying ~140 data-centre projects (~50GW) inside that queue. The data centre queue alone is of a similar order of magnitude to GB’s winter peak demand, underlining both the scale of speculative interest and the potential system impact if even a fraction connects. Ofgem has responded with proposals to “curate” the queue via tighter readiness tests and data centre specific financial mechanisms (e.g. refundable deposits or progression fees) to deter speculation and accelerate credible builds.

If reforms unlock delivery, the system impact is structural. Data centres add high load-factor baseload demand, tightening scarcity hours and likely extending the role of gas as the reliability backstop whether via grid supply, private wire arrangements with dispatchable plant, or hybrid structures pairing PPAs with firming and on site backup.

During winter 25/26, GB power price volatility and spreads have been subdued with a backdrop of slow demand growth, ample wind and low gas prices, but data centre led demand growth is a reminder that conditions can turn quickly. Ireland’s trajectory shows how rapid demand growth can tighten the system and force policy responses including emergency generation and requirements for data centres to contract new build renewables and provide flexibility during system stress.

A core theme here is that this isn’t just a market story it’s also a political shift. With economic growth increasingly front of mind across GB and Europe, there is rising pressure to prioritise strategic investment and security of supply even where this creates tension with climate goals, as highlighted by pushback on carbon costs (including Italy’s ETS related interventions). With hyperscalers investing billions into the UK, this could materially influence how the power system develops including the pace and pathway of decarbonisation.

At Timera Energy, we support investment in energy flexibility across the Power and gas sector, providing bankable revenue forecasts, transaction support, route to market support, and quarterly BESS subscription services. Our approach is differentiated by our stochastic modelling suite, which captures distributions of price formation, volatility and scarcity, an approach we’ve set out in a recent Timera blog.

If you’d like to discuss our modelling approach in more depth or our views of GB and European power markets, feel free to reach out to Arshpreet Dhatt (Senior Analyst) arshpreet.dhatt@timera-energy.com.