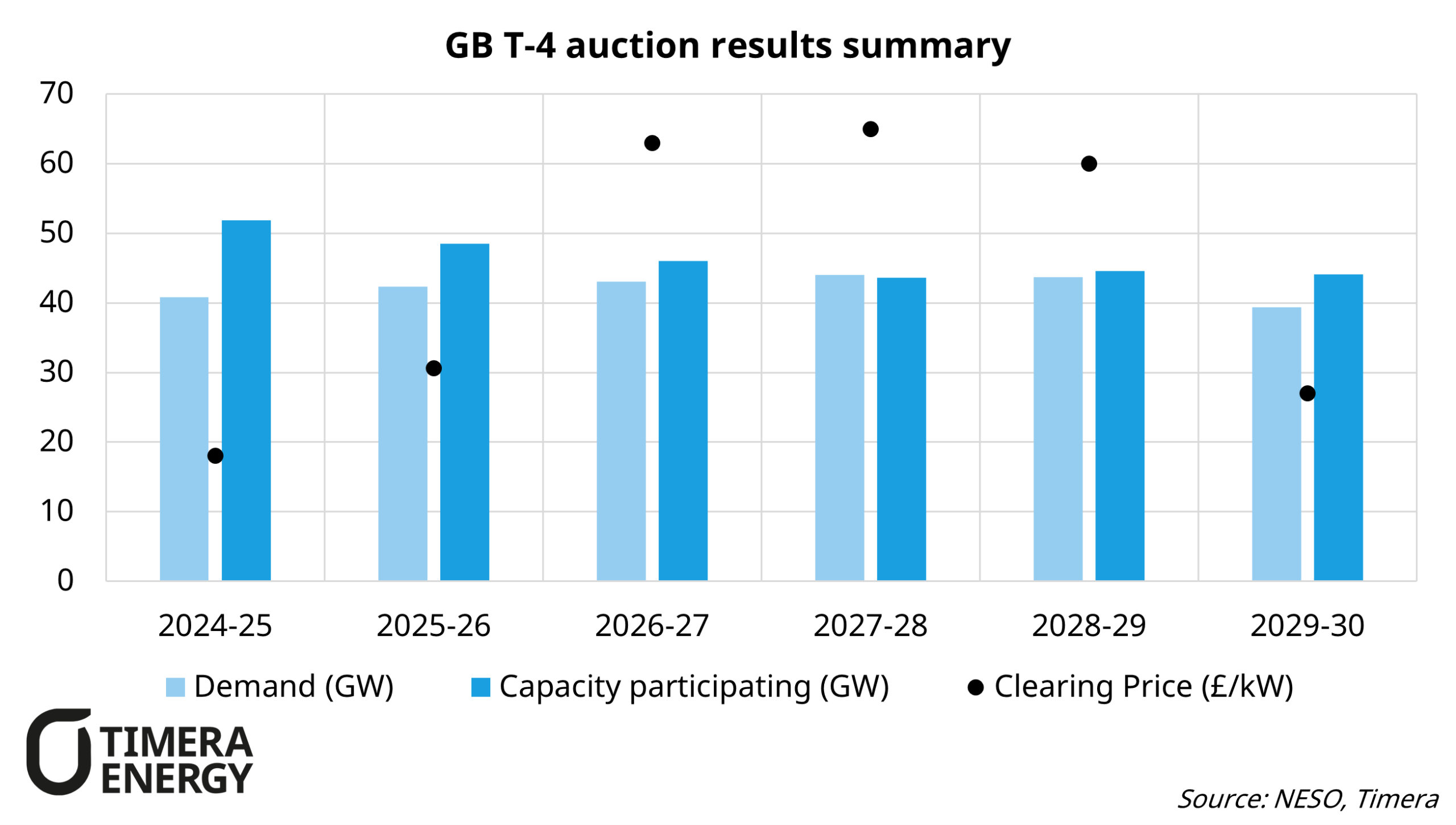

The GB T-4 Capacity Market auction for the 2029/30 delivery year cleared on Tuesday at £27.10/kW, a significant drop from the £60-65/kW range that has been observed over the last two auctions. 40.1GW of derated capacity secured contracts out of ~44GW that entered.

Recent auctions were defined by tightness as high demand targets set by government combined with a large volume of BESS entering the auction at heavily de-rated capacity factors, meaning each MW of batteries contributed relatively little to the overall auction liquidity. This kept prices elevated.

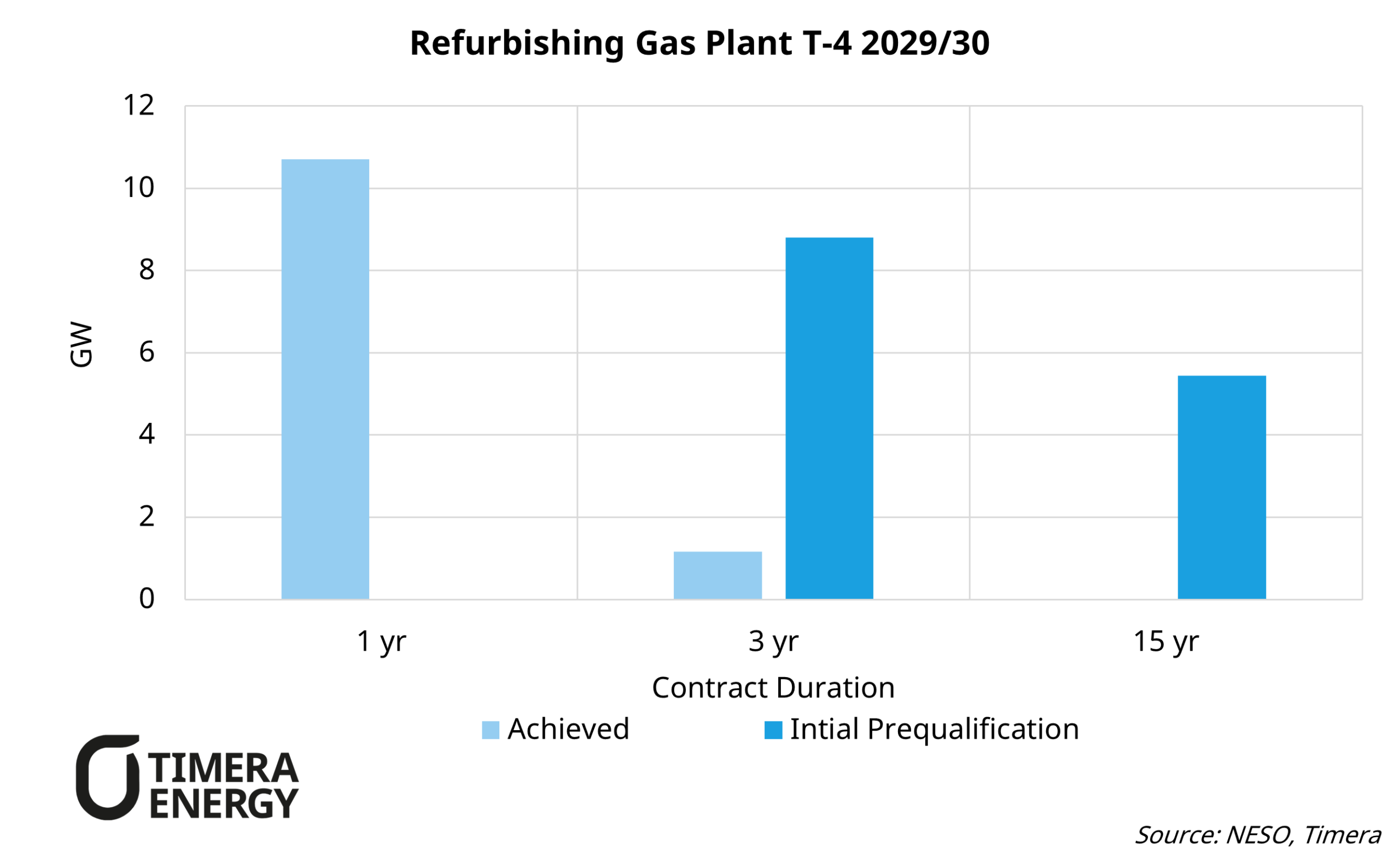

In this most recent auction the dynamic as shifted first with a lower demand target of 39.4GW relative to last year’s 43.7GW. As well as this, around 14GW of gas plant entered under refurbishment agreements, initially prequalifying for both 3-year and 15-year contracts as shown in the chart. This was directly enabled by a recent CM rule change that reduced the CAPEX threshold for 3-year refurbishment agreements from £170/kW down to £65/kW, opening the door to a much wider pool of plant to qualify for multi-year deals without committing to a major overhaul.

However, with the price clearing at £27/kW, the economics for multi-year refurbishment commitments didn’t stack up for most participants. Only ~1.5GW gas plant took a 3-year agreement with ~11GW opted for 1-year contracts instead opting to extend plant life into the early 2030s ahead of eventual retirement, rather than committing capital to significant refurbs.

Another key feature of this year’s auction is that no new-build gas cleared, while 178MW of new build gas in T-4 2028/29. Some plant may have been holding out for the introduction of a higher price cap for dispatchable capacity in coming years, which government ruled out in recent weeks. For most others, the price was simply too low relative to rising CAPEX as gas turbine costs have been pushed up by supply constraints driven partly by surging data centre demand globally.

~1.2GW of derated BESS cleared, compared to ~1.75GW derated in the prior auction. The drop in capacity is partly because some projects were knocked out following TM04+ reforms that disqualified capacity with delayed grid connection dates. Out of ~4GW of nominal capacity cleared, 2hr projects dominated, though just over 1GW was 4hr+ in duration, reflecting a growing investor shift towards LDES as BESS capex falls sharply. This is a trend expected to continue, with longer duration projects likely to take a larger share in coming auctions.

Total BESS with CM agreements now sits at over 30GW by 2030 if everything in the pipeline is commissioned. Overbuild risk is a growing concern, particularly as gas plant life extensions and nuclear uplifts continue to provide firm supply and dampen the price volatility that BESS revenues depend on.

What this means for GB power markets

Gas remains central to system security into the early 2030s with a wave of 1-year life extensions.

New build gas is stuck as between CAPEX inflation & turbine shortages the investment case for gas in the CM remains challenging for now.

BESS overbuild remains a key concern for investors with 30GW+ in the CM pipeline out to 2030. We will explore the implications of this in our Q1 2026 GB BESS subscription (out at the end of March) which will include bankable revenue curves, spot year sensitivities and a low scenario to give investors a robust view of the range of outcomes ahead.

If you are interested in our views of the GB gas investment case, GB BESS outlook or our views on wider European markets, reach out to Arshpreet Dhatt (Senior Analyst, Power) at arshpreet.dhatt@timera-energy.com