“BESS investors may have a new route to market

Italy is moving through one of its most intense windows of energy policy change in recent history.

In this article, we set out 8 important developments impacting power asset valuation and route-to-market strategies for investors:

1. DL Bollette decree – an emergency market policy intervention

2. PSV–TTF liquidity service and the gas and power price impact

3. Power-price interventions: thermal cost relief + REMIT enforcement

4. Grid connection reform and its impact on asset pipelines

5. Data centre connection reform & upside value impact

6. Capacity Market consultation and next MACSE auctions

7. Tolling market dynamics and merchant value

8. FER-Z as a new opportunity for BESS

For each of these, we set out key asset value impacts for investors.

1) DL Bollette: politically driven structural intervention

DL Bollette is an Italian government emergency decree law approved on 18th Feb 2026. It is focused on tackling high energy costs for households and businesses and reshaping aspects of the energy sector.

DL Bolette explicitly targets structural energy cost and competitiveness issues, as well as infrastructure bottlenecks. The decree was the result of the political pressure from Italian industrial consumers facing higher energy costs relative to the rest of Europe.

The decree is mainly targeting the post 2027 horizon. Some interventions are expected to be temporary and dependent on ARERA execution. However, this decree is a clear signal of how strong Italian energy policy intervention may be.

Investor takeaways:

- Policy and regulatory risk remains a core investment case driver for Italian power assets

- Quantifying the impact of different policy outcomes on asset & portfolio risk / return distributions is important

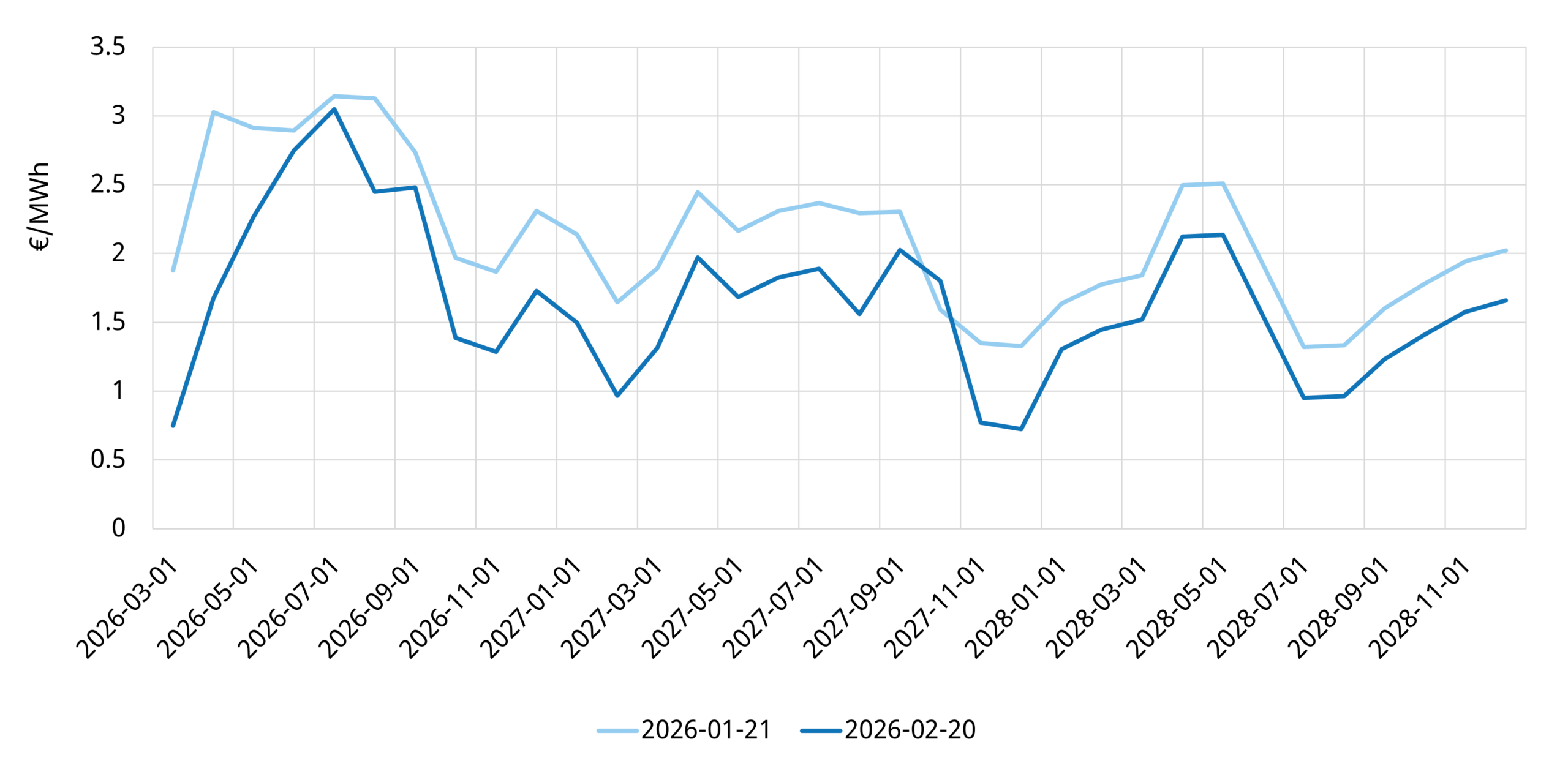

2) Gas market reform: PSV–TTF liquidity service set to reduce power prices

DL Bollette introduces a liquidity service designed to strengthen Italian gas hub (PSV) liquidity and reduce the structural PSV–TTF premium. We covered the mechanics of this scheme and its limits in a recent snapshot article on the PSV–TTF spread.

This gas price intervention translates directly into lower power prices, given gas plants dominate marginal price setting in Italy. Narrowing the PSV–TTF spread compresses the wholesale price premium in Italy vs North-West Europe.

Chart 1 shows how this spread fell across the last month, even before decree approval because of market expectations and policy leaks. However, the forwards still imply a structural PSV premium against TTF for the next few years.

Chart 1: PSV-TTF forward price spread decline

Source: ICE, Timera Energy

Investor takeaways:

- The PSV – TTF spread impact of this mechanism is mitigated by the fact that only a relatively small budget has been allocated to this mechanism (€200 millions)

- Spread compression is likely to be focused in periods of tight gas market conditions

- This measure could likely reduce extrinsic value upside for flexible power assets, rather than structurally reduce intrinsic value.

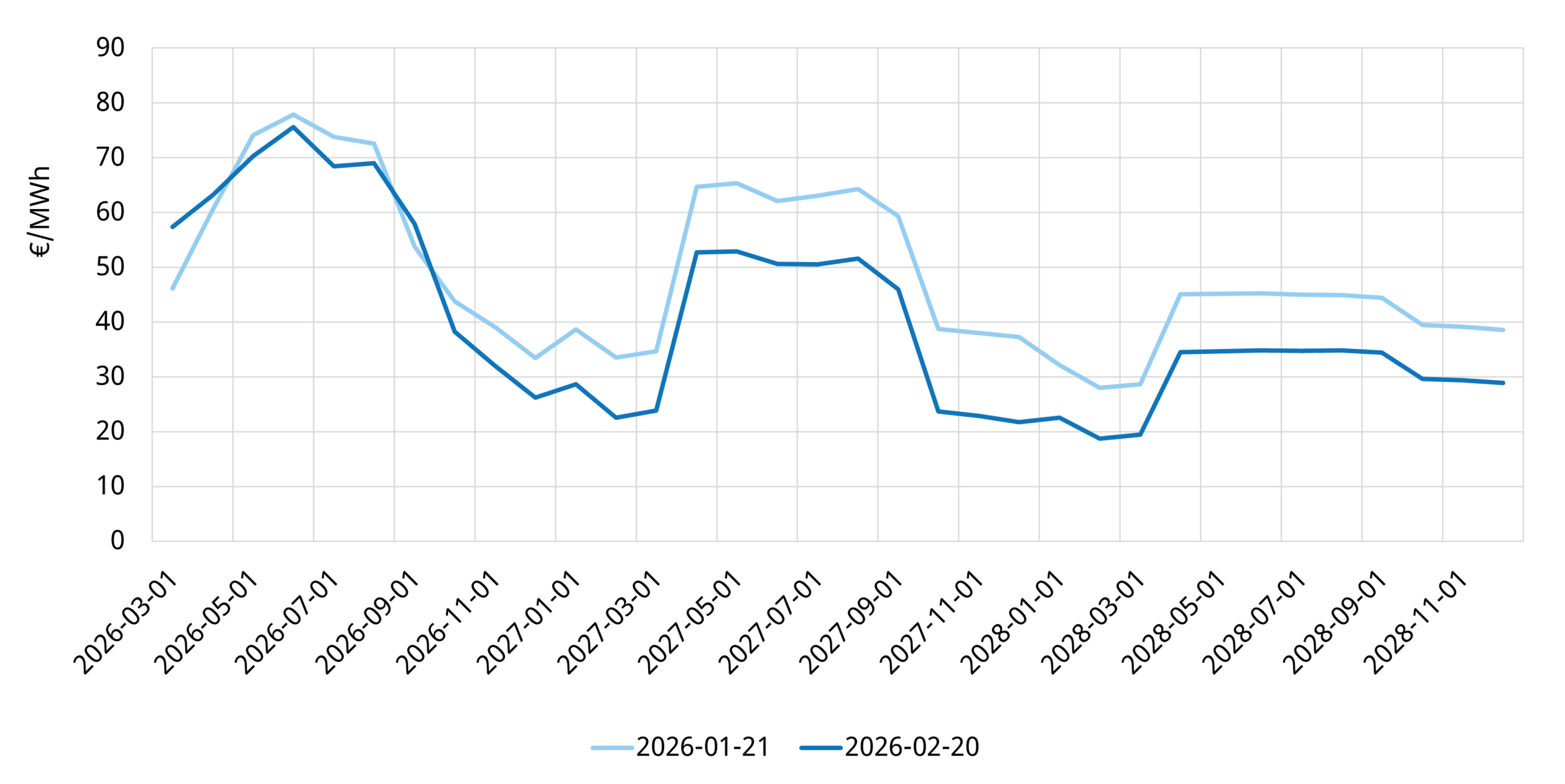

3) Power price interventions: thermal costs + “competitive checks”

DL Bollette also acknowledges that Italy’s power price premium vs other European countries is not driven by PSV premium alone. The decree includes interventions designed to fix other issues.

3.1 Thermal cost relief from 2027: gas transport items + ETS-linked component

From 1 January 2027, ARERA will define how gas transport tariff components are refunded to thermal generators. An ETS-linked compensation mechanism will also be introduced, subject to cost pass-through obligations and ARERA monitoring.

The ETS component is explicitly conditional on EU State aid approval, making the European Commission’s decision key for investor value impact. Design constraints will need to avoid distortions to cross-border flows and market coupling, potentially limiting scope or requiring safeguards.

Chart 2 shows how 2027-2028 forward Italian power prices were significantly repriced by the market across the last few weeks, although a structural spread vs neighbouring countries remains.

Chart 2: Italian-French forward power price spreads (baseload)

Source: ICE, Timera Energy

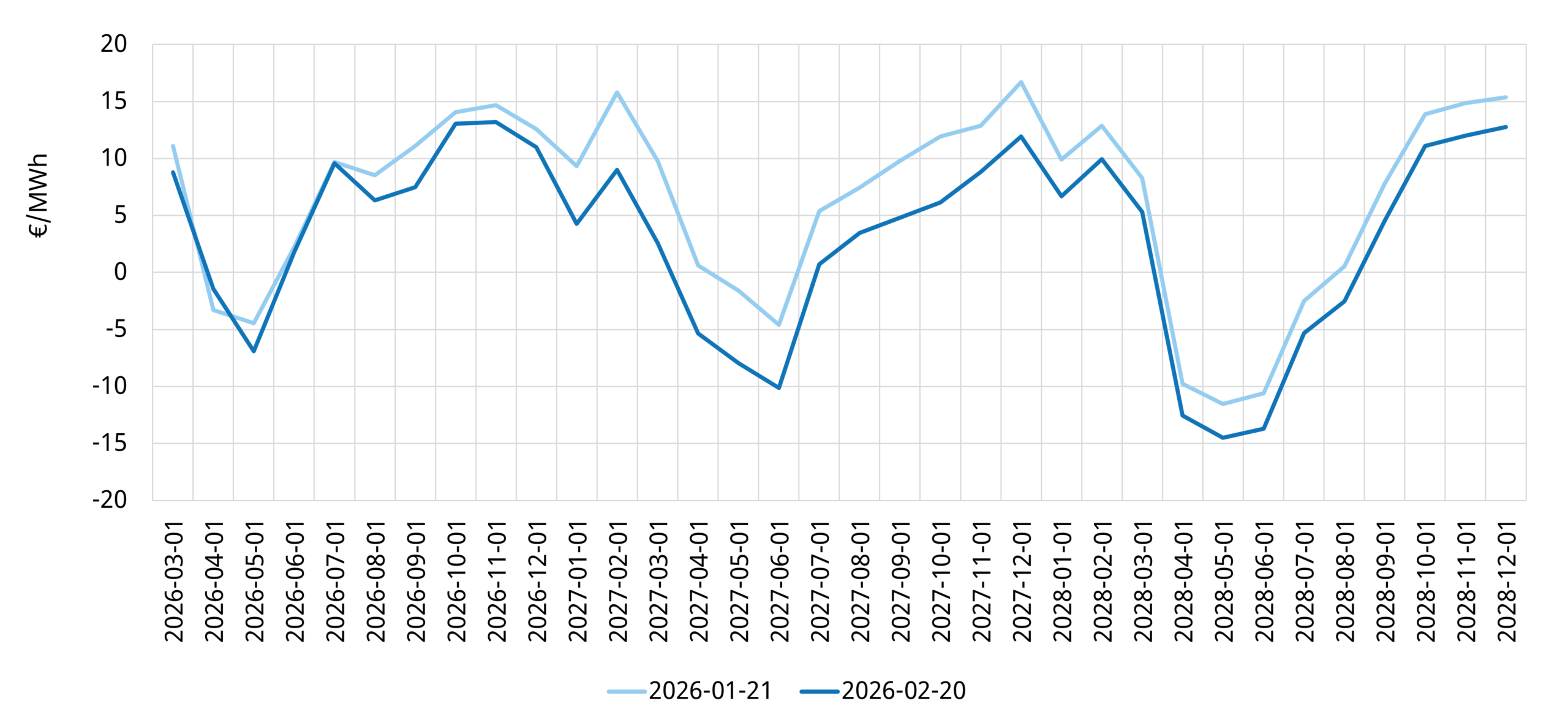

3.2 Competitive checks: policy recognition of mark-up premia

The decree strengthens the “competition integrity” dimension, mandating ARERA to assess capacity withholding behaviour and ensure bidding aligns with REMIT principles.

ARERA’s Summer 2025 investigation linked Italy’s persistent premium to structurally higher marginal mark-ups, following the post-2022 regime shift as set out in our prior article on Italian power price divergence.

Chart 3 shows the impact of forward clean spark spreads (CCGT generation intrinsic margin metric) declining from Jan 2027.

Chart 3: Italian Clean Spark Spread future curves

Source: ICE, Timera Energy

Investor takeaways:

- This is likely to have some impact of reducing intrinsic and extrinsic value of flexible power assets (e.g. BESS, LDES, hydro)

- The impact in the short term could be stronger for RES value rather than for BESS, given reduction in power prices vs intraday & MSD price volatility

- The overall impact will be highly dependent on final mechanism implementation (e.g. how much and for how long EUA will be reimbursed).

4) Grid connection reform – important value impact on development pipelines

DL Bollette confirms the shift from connection as a reservation right to a merit-based allocation for RES and BESS.

Projects failing to secure Terna approval are expected to have STMG proposals cancelled within six months. Terna will publish quarterly updates on additional capacity available by network area. ARERA will revise connection rules, including overbooking, decadence mechanisms and stronger linkage between reservation duration and permitting maturity.

Investor takeaways:

- Careful assessment of project connection features is now even more important during due diligence

- STMG “optionality” loses value without permitting maturity

- Pipelines stratify into: (i) permitted, (ii) validated by Terna but not permitted, (iii) pure reservation

- Projects aligned with credible substation reinforcement gain structural advantage; saturated areas become structurally disadvantaged, shifting M&A premia

This aligns with broader European reforms addressing legacy grid processes under energy transition pressures.

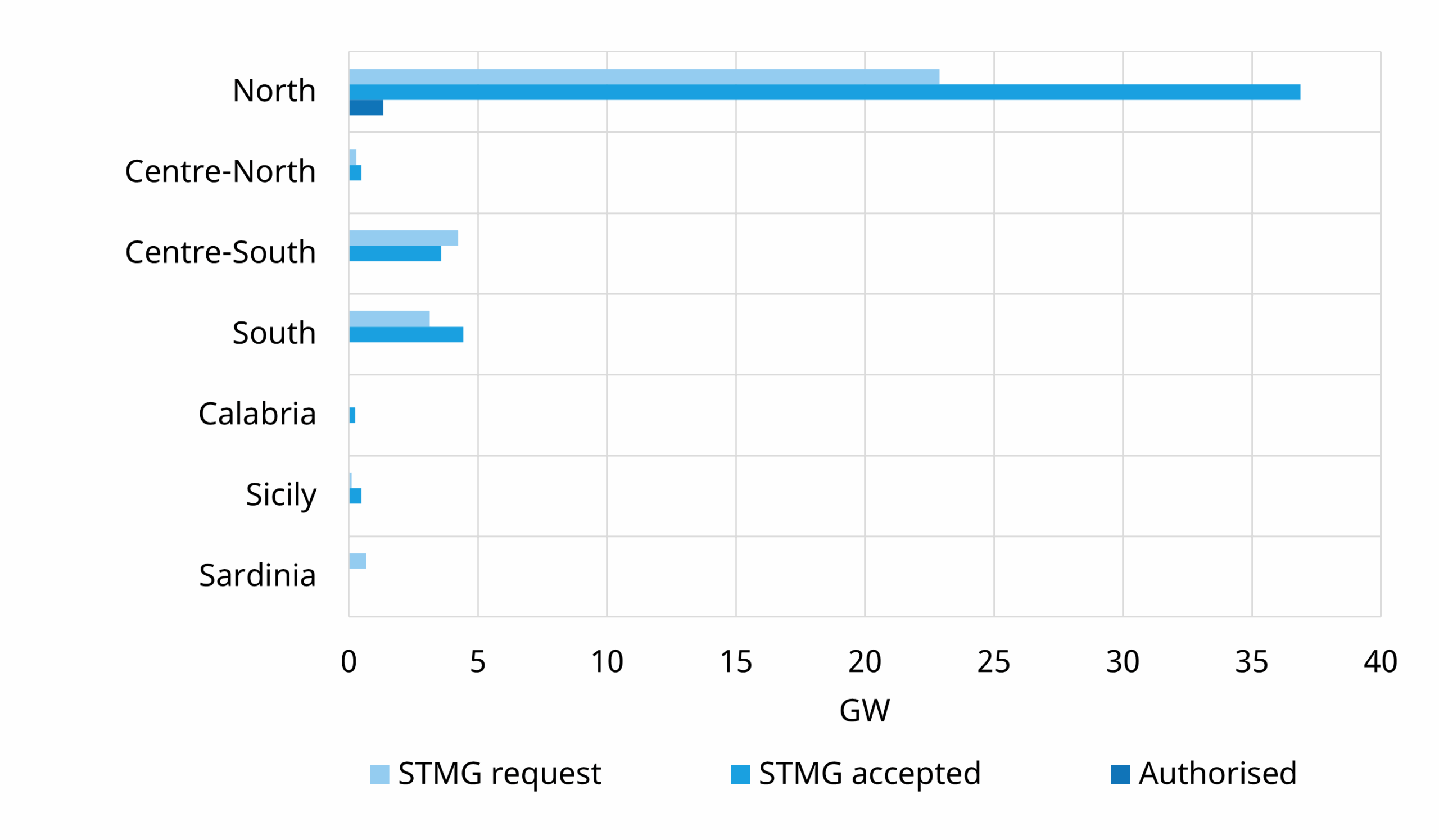

5) Data centre connection queue reform – upside value driver

The decree aims to streamline data centre authorisation and integrate connection works into a unified process. Faster permitting could increase the probability of COD for viable projects. The current 78 GW connection queue (Chart 4) represents material demand-side optionality.

Chart 4: Connection request queue for Data Centres in Italy (as of Jan 2026)

Source: Terna, Timera Energy

The queue is concentrated in the North, potentially amplifying existing North–South demand asymmetry. This could:

- Shift zonal demand forecasts and impact wholesale prices and PPAs

- Tighten Capacity Market demand curves and support clearing premia

- Increase implied value for flexible and adequate capacity (LDES and conventional)

Investor takeaways:

- Data centre demand represents material upside for power asset values

- Enabling AI-driven demand growth is particularly relevant in a market with a historically stagnant load

6) Capacity Market consultation and next MACSE auctions

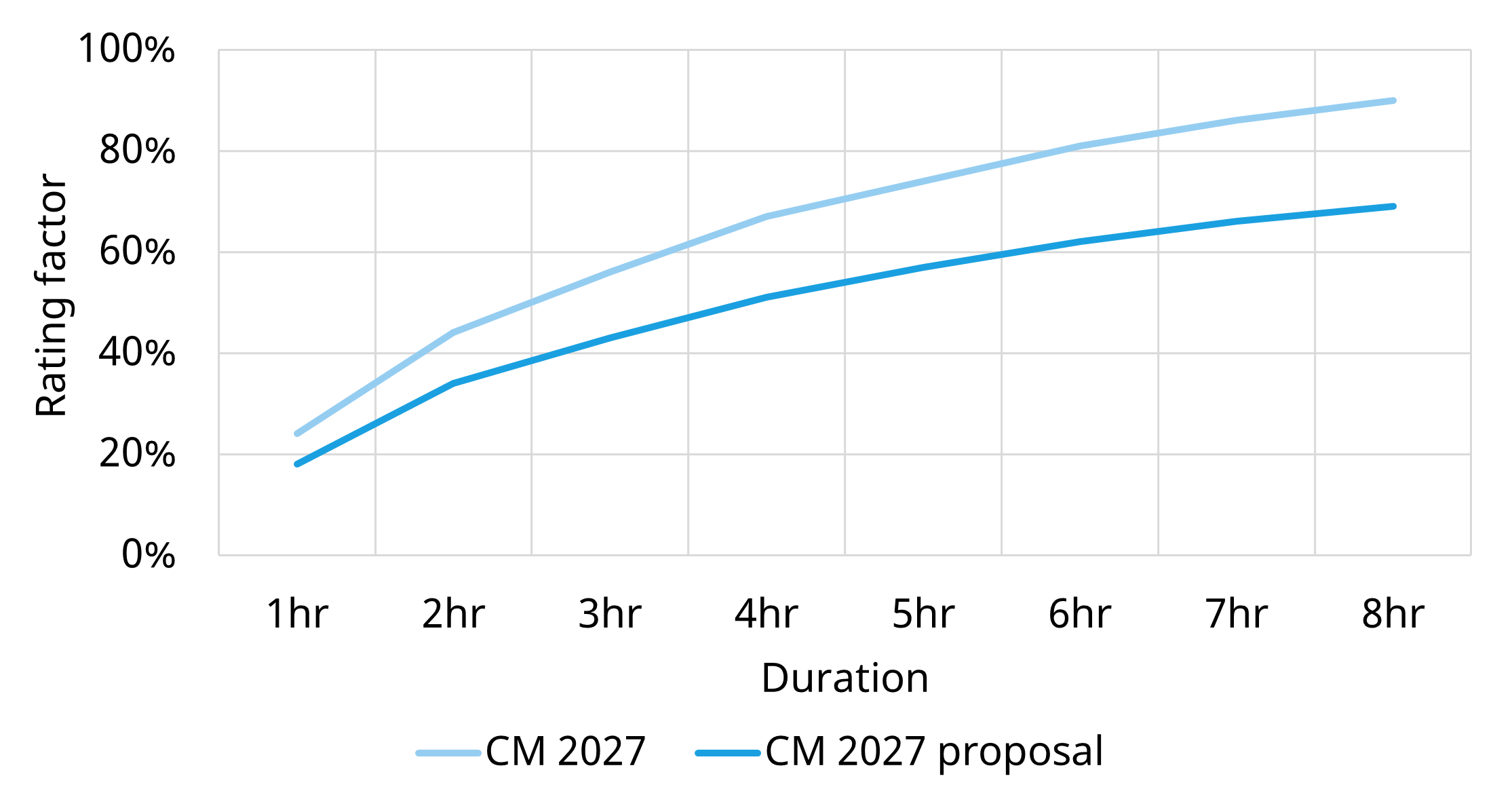

Terna has launched a Capacity Market consultation (submissions due 9 Mar), including revised derating for the 2028 auction (Chart 5).

Chart 5: Original vs proposed Capacity Market derating factors

Source: Terna

Revised derating affects participants in two ways:

- Lower derating for BESS and RES reduces recognised CM premium per MW.

- Changes to adequacy contribution may increase auction space for new capacity (CDP), potentially supporting higher clearing prices but still depending on final constraints, data centre treatment and incumbents’ strategy.

Timing is also relevant. Consultation changes may delay the next CM auction, with knock-on effects for MACSE (targeting 2029–2030). MACSE auctions occur 270 days after consultation publication, pushing the next expected round toward end of 2026.

Investor takeaways:

- Derating reform presents both risk and opportunity, to be factored into asset investment cases

- CM auction analysis must incorporate both volume and price effects in valuation

7) Tolling market dynamics and merchant value

Italy’s BESS tolling market is evolving rapidly, with four major contracts signed recently and strong interest from CM-awarded capacity seeking revenue stability.

Two structural drivers:

- Low MACSE clearing prices increasingly anchor fixed-price discussions, exerting downward pressure on offtake pricing

- From 2028, time-shifting products may compete with tolling structures, likely already reflected in negotiations

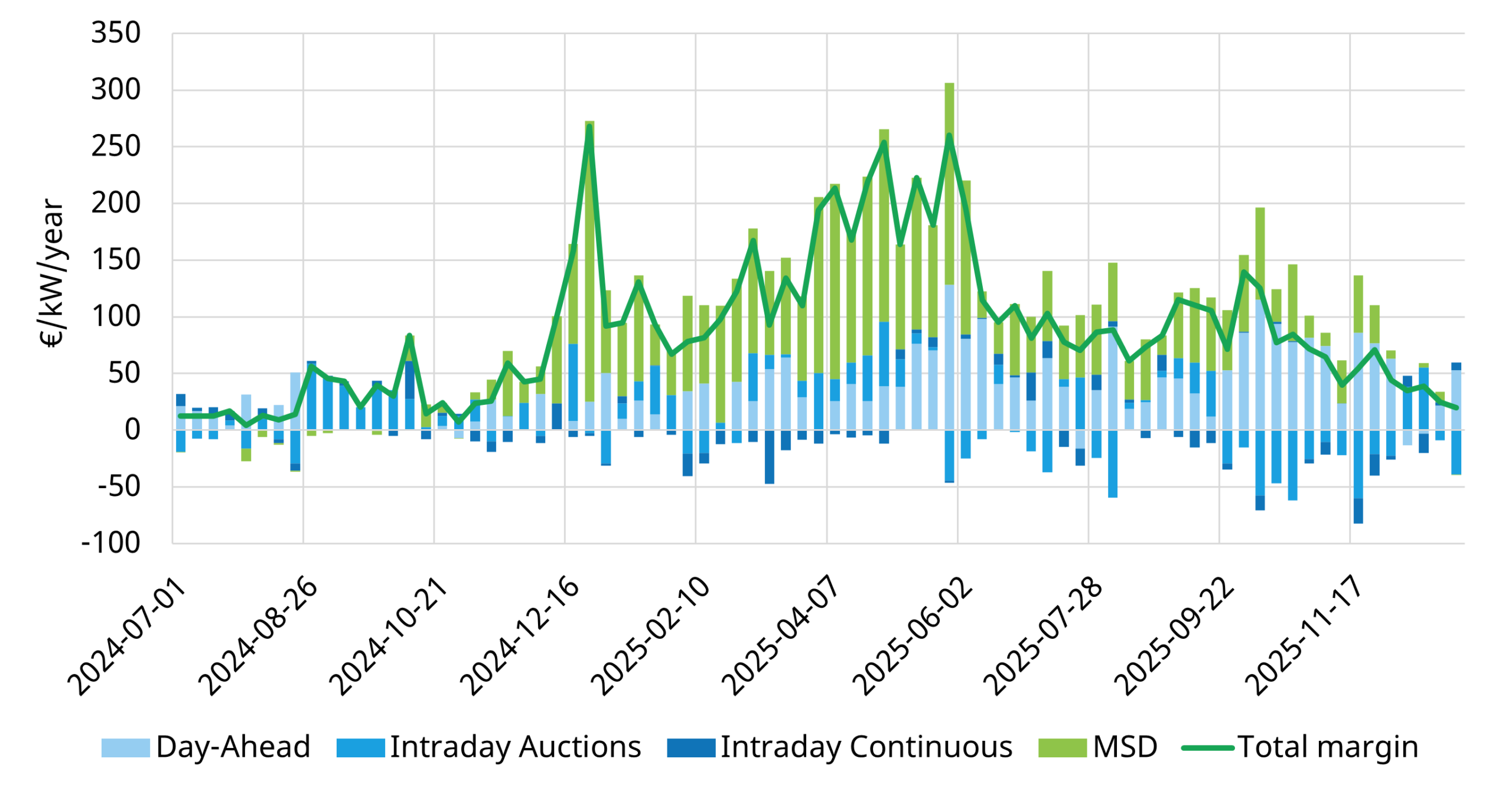

Merchant benchmarking remains critical. Current Italian merchant value is lower than in some European markets. Chart 6 shows annualised margins for the best-performing 4-hour asset in the North, though structural changes (FER-X, FER-Z, BESS deployment, demand evolution, FCR integration, flow-based coupling) limit historical extrapolation.

Chart 6: Historical 4 hr BESS margins in North zone

Source: GME, Timera Energy; note chart shows weekly annualised margins for the best 4hr BESS asset performers participating in the North bidding zone

Investor takeaways:

- BESS merchant value levels in the Italian market remain structurally lower than in other European markets, however this may potentially shift across the next few years

- Approximately 90% of existing BESS capacity is optimised by Enel under portfolio logic, reducing the representativeness of current individual asset performance

- MACSE still represents a unique route-to-market opportunity for BESS assets in South of Italy, but Capacity Market, tolling contracts and merchant exposure are crucial alternative routes that can offer risk adjusted upside.

8) FER-Z: a new opportunity for BESS

The FER-Z CfD mechanism for RES is under consultation. It may revive the case for co-located RES+BESS, despite MACSE’s stricter co-location constraints.

FER-Z moves toward remunerating shaped or baseload-like output profiles, increasing the strategic role of storage:

- Co-located BESS can economically shape CfD output.

- Alternatively, southern RES portfolios may combine time-shifting products with MACSE-backed capacity.

Investor takeaways:

- FER-Z may provide an additional route-to-market for BESS, though design remains under consultation and not yet fully defined

- It is a more complex CfD scheme than FER-X, but one that may open new co-located and flex asset portfolio opportunities

Closing investor implications

The breadth and pace of reform reinforces one conclusion: the impact of policy risk must be effectively embedded and quantified in asset investment valuation analysis.

Beside MACSE and CM, Italian BESS investment has now a potential third regulated route to market option to consider: FER-Z. The relative attractiveness of these solutions for investors is materially impacted by the policy reforms we set out above.

Feel free to reach out to Alessio Cunico (Associate Director) alessio.cunico@timera-energy.com for further information on our services in the Italian market.