The focus on GB power capacity into Winter 23/24 intensified this week. Across the space of a few days:

- DESNZ requested NGESO start negotiating the possibility of extending the Winter Contingency coal contracts (currently in place with Drax, EDF’s West Burton and Uniper’s Ratcliffe)

- Within a day, EDF and Drax simultaneously announced they have ruled out extending the coal units into Winter 23, citing logistical, workforce, maintenance and compliance reasons.

Coal is currently due to be phased out of GB by the end of 2024, while other sections of conventional generation are aging – Heysham 2 retirement is now slated for 2028, but Hartlepool and Heysham 1 flagged as extended by two years to 2026. These are being replaced by batteries (~5GW nominal in the latest T-4 CM) and renewables (e.g. ambitious ~50GW offshore wind target from ~14GW current by 2030).

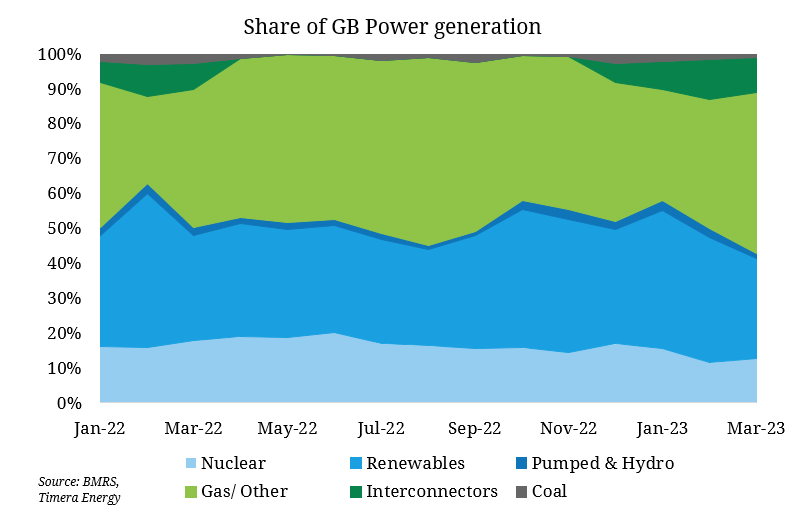

However these are not a quick fix for the challenges to be faced this winter, if GB looks to avoid demand destruction (hence high prices) on the margin. Coal has contributed 1.6% of GB power generation, even across the unusually mild Winter 22/23 so far, highlighting the upcoming challenge.