The recent escalations in the tensions involving the Middle East have raised the risk of disruption to LNG flows through the Strait of Hormuz, one of the most critical energy transit routes globally. As highlighted in our earlier post, a closure of the Strait represents a global gas supply shock given the importance of the Qatari LNG exports moving through. The disruption has pushed gas prices higher as markets price in the loss of supply and heightened uncertainty around how long the disruption might persist. April NBP forwards have nearly doubled from ~£25/MWh on 24 February to ~£48/MWh on 3 March.

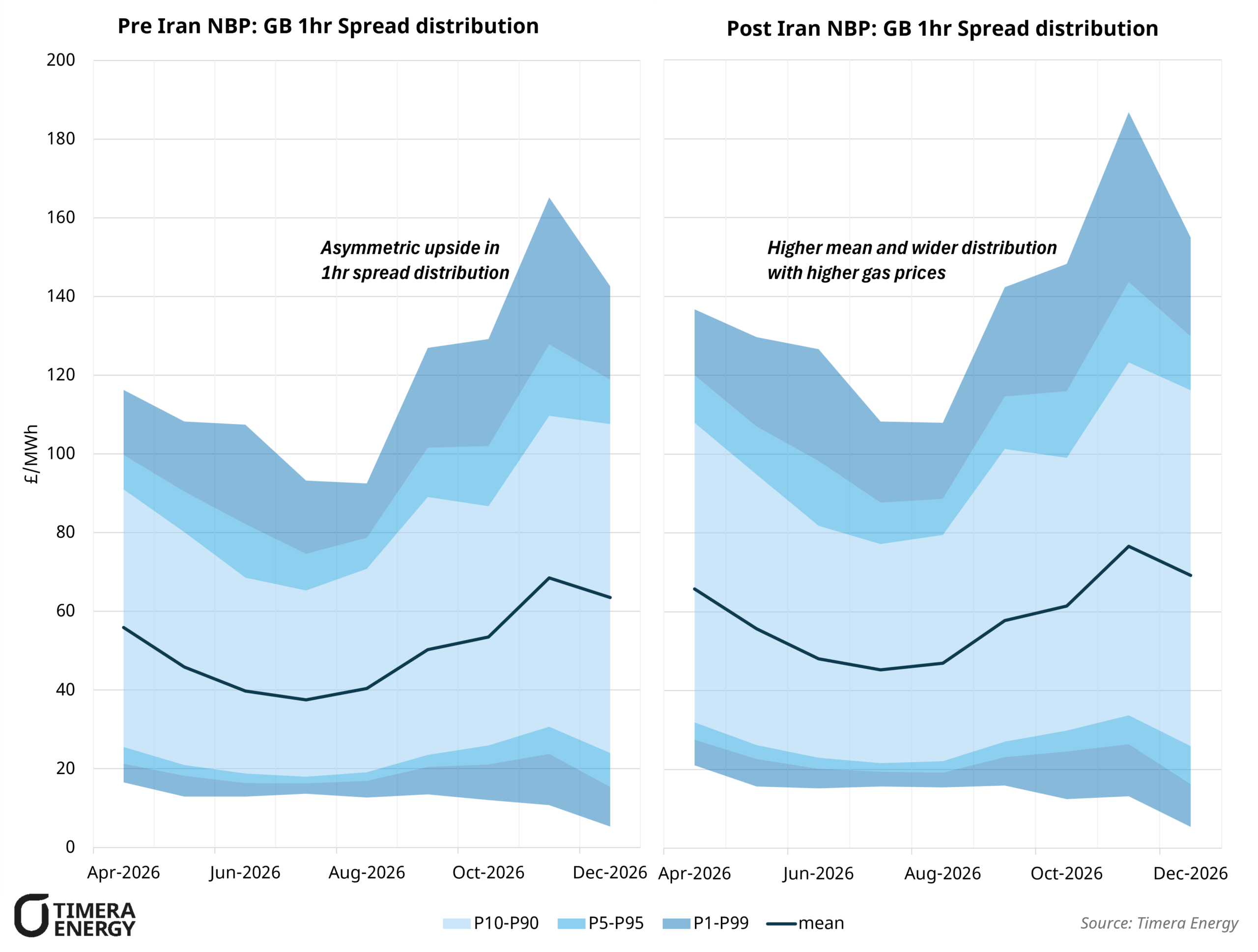

Gas fired generation remains the dominant marginal price setter in GB, meaning any sustained move in the gas forward curve passes directly into the power spread outlook and by extension into the value case for flexible assets like BESS. The charts above shows modelled 1 hour power price spreads in GB under two NBP forward curves: one week before the Iran conflict escalated, and one week after. The mean spread outlook is ~16% higher under the post conflict scenario a direct pass through of higher gas prices into average power spreads and BESS revenues.

The more interesting shift, however, is in the distribution around that mean. Both scenarios exhibit positively skewed spread distributions, reflecting a structural reality of power markets: there is a limit on how low spreads can go, but no equivalent constraint on the upside. The floor is anchored by days where similarly efficient gas plant sets the margin throughout, or where strong wind suppresses prices across the whole day neither of which changes materially between the two scenarios. Under the higher gas price scenario, it is the upside tail that expands with days of greater volatility and larger price spikes, strengthening the asymmetric value case for flexible assets.

The extent to which GB BESS assets realise the uplift demonstrated above in practice will depend on whether elevated gas prices materialise at the spot level or if it is partially locked in via forward hedge products such as day ahead swaps. For GB BESS operators, the improved spread outlook would offer some relief after a damper revenue environment this winter compared to winter 24/25 (see our previous post).

Stochastic modelling of various market scenarios is increasingly critical for capturing both value and risk in flexible asset investments, particularly in the context of rapidly evolving power markets and geopolitical landscape. If you’d like to discuss how our modelling approach can support you with bankable analysis in GB and European power markets, feel free to reach out to Arshpreet Dhatt (Senior Analyst) arshpreet.dhatt@timera-energy.com.