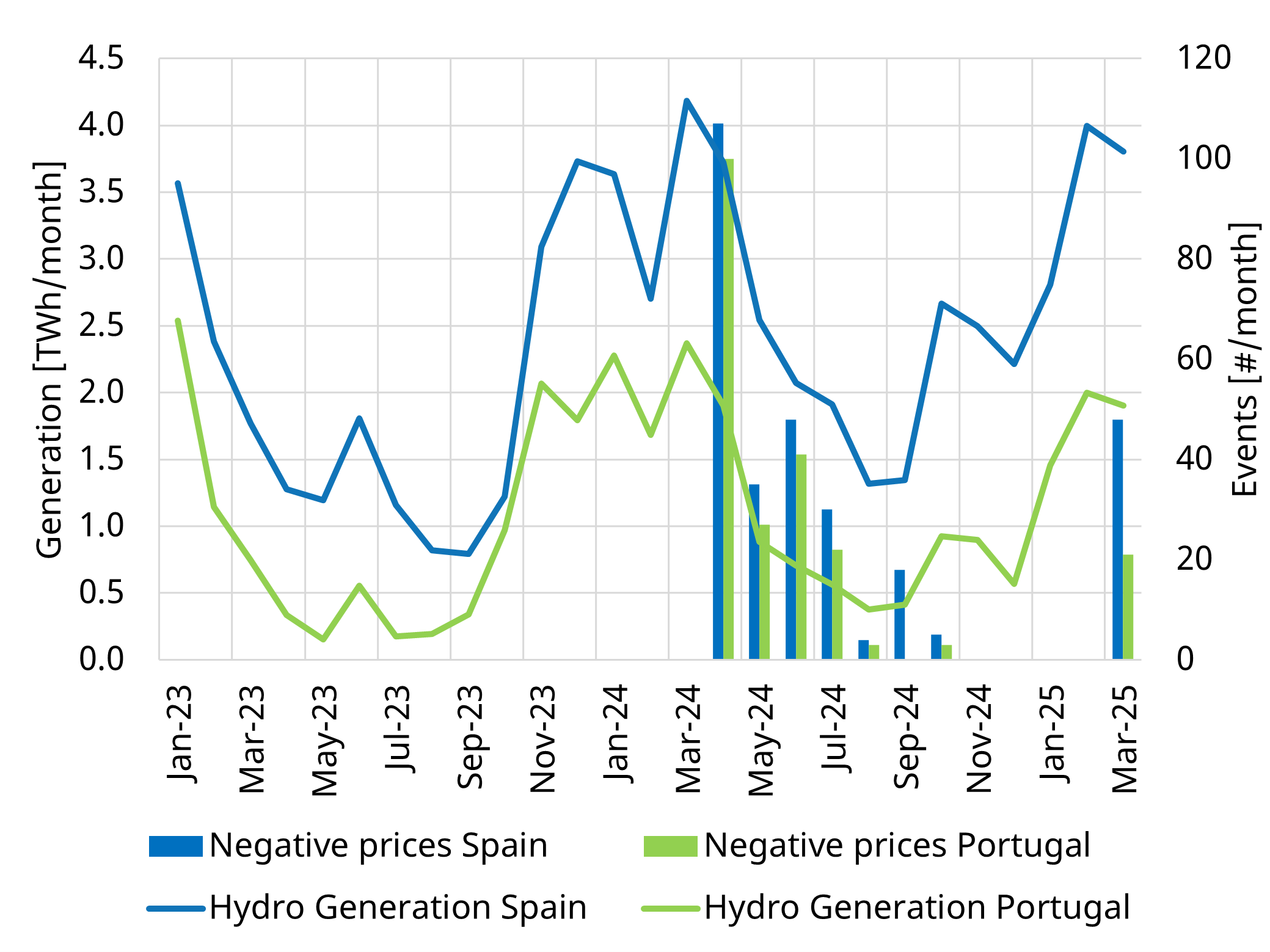

Negative prices are no longer a rarity in Iberia. Since their first appearance in April 2024, Spain and Portugal have seen sustained negative Day-Ahead prices events until October 2024. After a seasonal pause over Winter, negative price events have re-emerged in March 2025.

One key driver behind this structural shift is hydro. Exceptional rainfall in early 2025 pushed Spanish hydro reservoirs back toward record Spring 2024 levels, exceeding 14 TWh of stored energy more than France, Italy, Switzerland, and Greece combined. With reservoirs close to capacity, hydro generators are being forced into the Day Ahead market with low bids to avoid spillover. In doing so, they’re prioritising dispatch over price responsiveness, regardless of seasonal market opportunities.

Hydro, traditionally a flexible and price-sensitive asset class, is now contributing more predictably to oversupply, particularly during midday hours, where it converges with rising solar output. March 2025 marked the first time that average negative prices fell below -1 €/MWh, driven by the low prices reached during the final weekend of the month.

With solar ramping up and hydro storage capacity constraints, price compression in the central hours is set to persist. This creates increasingly attractive arbitrage opportunities for storage assets, with average 1-hour spreads reaching their historical maximum in Iberia exceeding 150 €/MWh in March 2025.

Climate change and seasonal weather patterns are playing a growing role in shaping marginal prices across Europe. This is creating both seasonal opportunities and risks for flexible assets dynamics that can only be accurately captured through stochastic modelling.