Last weekend saw a prevalence of negative power prices across Europe driven by high levels of wind and solar output along with subdued demand. This led to many countries having issues with managing downward margins.

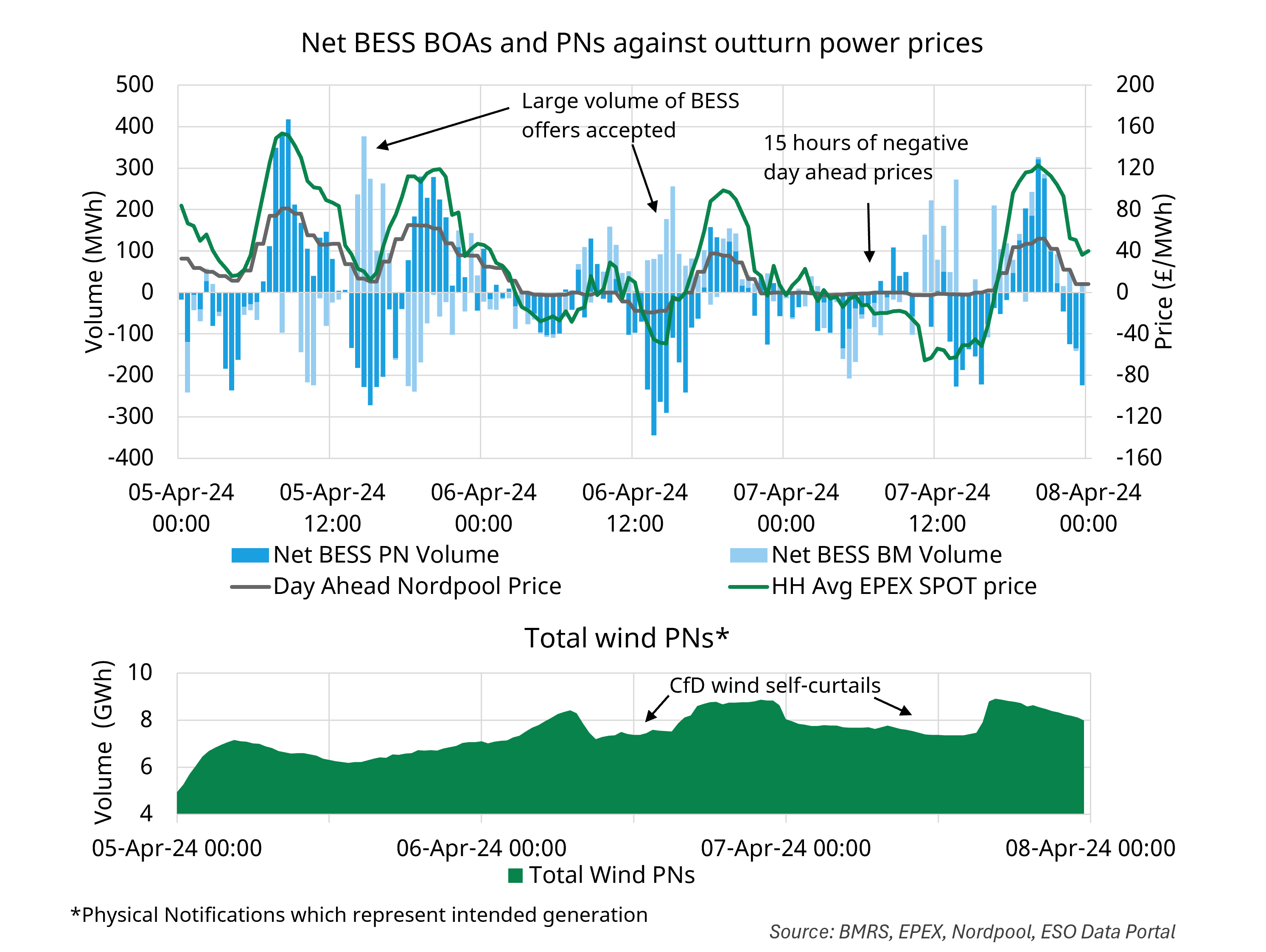

In GB a combination of high wind output due to Storm Kathleen along with mild temperatures led to many hours of negative prices, including 15 hours of consecutive negative prices on Sunday April 7th (as shown in the chart).

Most CfD backed units lose their subsidy after 6 hours of consecutive negative pricing with some losing subsidy during any periods of negative pricing, hence many CfD wind units self-curtailed during this period. Early CfD and ROC backed wind continues receiving subsidy payments during periods of negative price and hence continued generating and exacerbating negative pricing.

The weekend was particular beneficial for BESS which could use periods of negative pricing to be paid to charge, but were subsequently accepted for large volumes of energy tagged offers by ESO (see chart) and hence paid again to prevent them from doing so.

Market conditions such as this will become more prevalent as RES build out in GB continues providing further opportunities for high revenues for BESS. It also presents a case for zonal pricing to prevent large volumes of balancing actions such as those seen over the weekend.