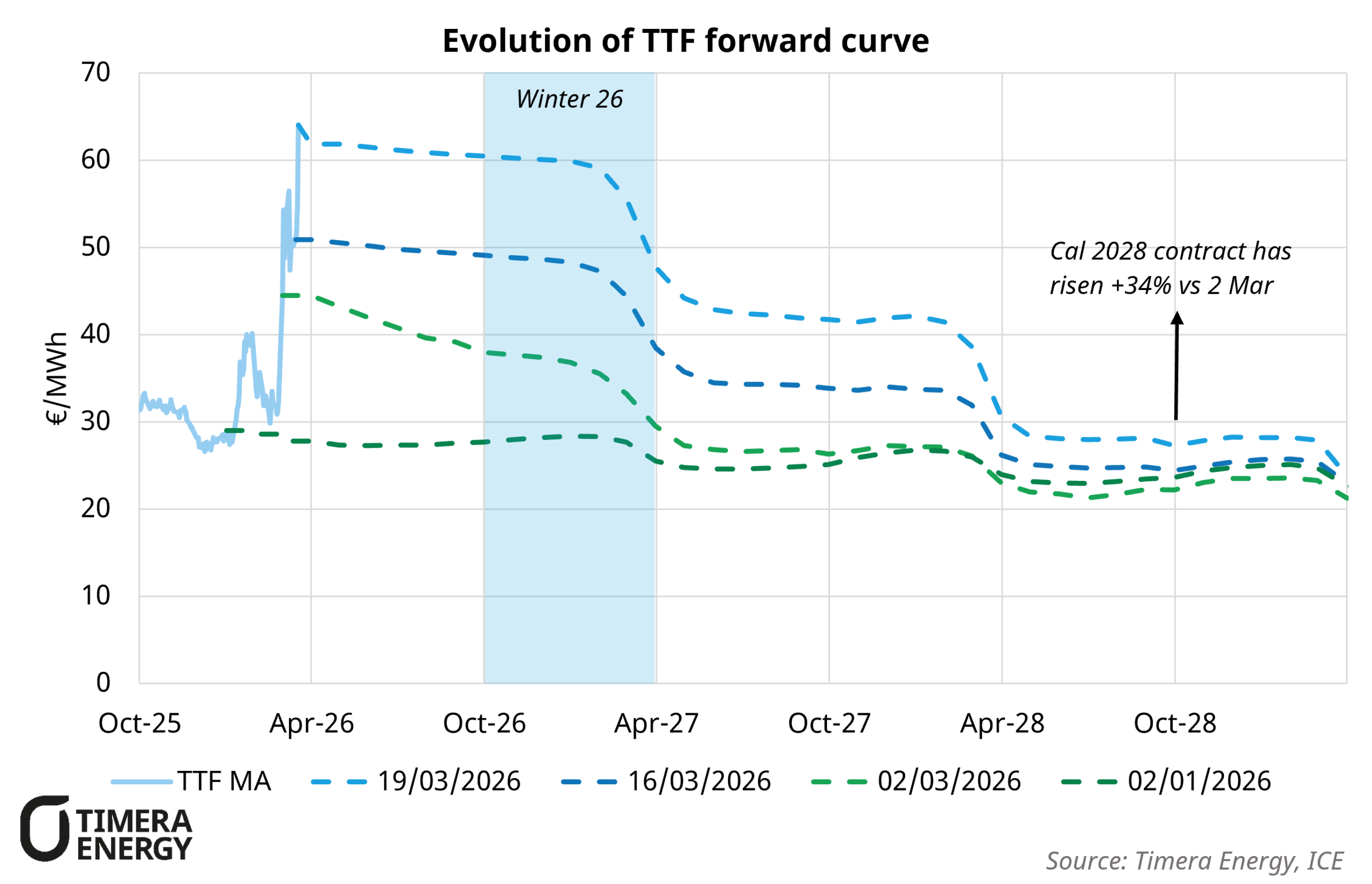

The April 2026 TTF contract opened 27% higher on 19 March, touching an intraday high of €74/MWh, before settling at €61.85/MWh, €7.2/MWh above the prior close as traders re-assessed impact of strikes on the Ras Laffan LNG export facility. Critically, the winter 2026 contract rose by around €8.2/MWh, outpacing the prompt move. This is a clear sign that the market is now pricing sustained disruption rather than a short-term shock.

This marks a clear shift from the initial reaction on 2 March, when the front month rose €12.5/MWh but winter 2026 increased by only €5/MWh. The fundamental driver of Thursday’s repricing is the scale of Qatari disruption, with strikes on trains 4 and 6 at Ras Laffan. Saad Al-Kaabi (QatarEnergy CEO) stated that these strikes have taken approximately 12.8 mtpa of LNG capacity offline for three to five years.

QatarEnergy has indicated it may declare force majeure on long-term contracts with buyers in Italy, Belgium, South Korea and China, the primary destinations for affected volumes. With Asia bearing the largest share of lost supply, European buyers will need to price up to attract marginal cargoes from alternative sources to backfill the gap, reinforcing the structural bid now visible across the 2026 and 2027 contracts.

If you would like to discuss the implications of these supply disruptions for your portfolio or trading strategy, please contact David Duncan (david.duncan@timera-energy.com)