Since the heightened panic across the Eurozone last summer, central banks have flooded credit markets with cheap money. This has temporarily calmed credit market fears and FX volatility has fallen in sympathy. But in the absence of any real structural steps to address the problems of the Eurozone and its undercapitalised banking system, the crisis is far from over. The fragile state of Europe is evident from the recent problems caused by Cyprus which, given its size, should not be a source of late night emergency bailout sessions.

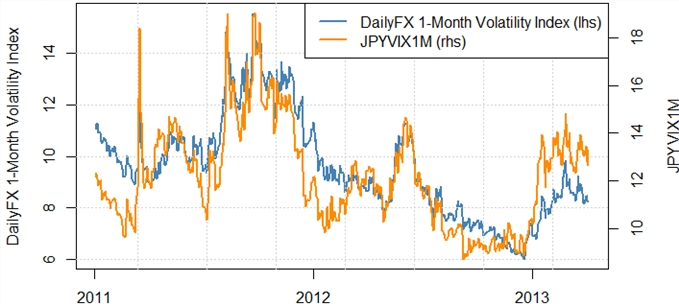

FX risk management can often be the Achilles heel of an otherwise sound energy portfolio risk management framework. Chart 1 shows FX volatility on the rise again in 2013. A key factor behind this rise has been the vast (USD187 billion a month) new quantitative easing programme recently instated by Japan, to try and reflate its way out of a state of stagnant bankruptcy. In a world of ever more daring and unorthodox monetary policy, it is a good time to revisit the impact of FX risk on energy portfolios.

The problem that is forward FX

Energy contracts that specify payment for delivery of a commodity (e.g. gas) at a specified date in the future are core to the commercial business of most European energy companies. If that delivery is in a foreign currency (e.g. EUR) then there is a direct forward FX exposure associated with the future cash payment. In addition this cashflow needs to be discounted for risk measurement calculations to account for the time value of money. Indirect or implied forward FX exposure can also result from complex contract price indexation. For example, where the formula includes FX conversions or includes prices where the currency unit of a formula component is different from the underlying market (e.g. averaging EUR/MT Gas Oil quote when the underlying market is quoted in USD/MT).

The treatment of forward FX and IR exposures can often be hidden ‘under the bonnet’ of most trading and risk management system solutions. But a number of energy companies are facing inconsistencies in the way they treat FX and IR exposures across their portfolio. The impact of these inconsistencies has become more pronounced over the last 3 years as a result of funding stress in financial markets from the European debt crisis. These inconsistencies can undermine mark to market and risk measurement calculations and compromise the principle that all portfolio exposures are consistently priced against the most liquid market source.

A clash between two approaches

There are two approaches commonly used to tackle the FX and IR exposures associated with forward energy positions:

- using LIBOR (the London Interbank Offered Rate) interest rate quotes to discount exposures which are then valued against a spot FX rate

- using forward FX market quotes and deriving an implied interest rate curve to discount exposures.

Both are theoretically valid but there are some clear pitfalls to watch out for. For legacy reasons, usually driven by systems implementation, many energy companies rely on the LIBOR discounting spot FX approach. LIBOR curves are accessible and commonly used across other areas of energy companies (e.g. by treasury, accounting and settlements functions).

The shortfall of this approach is that it results in a representation of forward FX exposures as (i) a large spot FX exposure (ii) a relatively small exposure to the interest rate differential between the two currencies involved. Given that the forward FX exposure is typically hedged with traded FX forward contracts, there is a mismatch between the risk management exposure representation and the way the exposure is managed in practice.

The knock on implications of this is that it compromises the ability of traders and risk managers to understand the impact of movements in forward FX rates on portfolio value (eg through VaR simulations or stress tests). The use of quoted forward FX prices for exposure mark to market and risk measurement provides a more accurate representation, but it can result in some difficult inconsistencies in the use of interest rates for discounting.

The two approaches are no longer interchangeable

Up until the onset of the financial crisis, the answer derived by approaches 1. and 2. above was essentially identical. Arbitrage ensured that there was no profit available from borrowing at home to lend abroad (or vice versa) if FX risk was fully hedged. This condition, commonly known as covered interest parity arbitrage, has broken down a number of times since the onset of the financial crisis.

Funding stress and counterparty credit risk issues have led to a divergence between LIBOR and interest rates implied from forward FX curve since the onset of the financial crisis. Both are valid market sources of interest rates, but for reasons explained below, there can be inconsistencies between the two of them. The reason for this involves a diversion into credit markets and is best illustrated by an example below. If you are not so interested in the cause, but more the effect, you can skip to the section below.

An Italian bank of dubious credit quality has structural USD liabilities associated with its commercial lending business and needs to fund these via short term borrowing of USD. Under normal credit market conditions it would borrow the USD in the interbank market at a rate referenced to LIBOR. But under the conditions of credit market stress that have prevailed since the onset of the financial crisis in late 2008, the bank is constrained in its ability to borrow USD in the interbank market. This can be both due to concerns of the Italian bank’s credit risk but also to a broader shortage of USD funding in times of more acute market stress. But the bank has an alternative option to obtain USD funding. Instead of borrowing in the interbank market (at LIBOR), the bank can buy USD for delivery in the FX forward market. In doing this the bank is effectively taking out a collateralised loan (EUR for USD). The impact of banks funding through FX forwards in this manner has caused a divergence between LIBOR rates and the interest rates implied from FX forward prices. In theory this difference is arbitragable. In practice credit risk and funding have constrained that arbitrage during periods of market stress.

How does this effect energy exposures?

It is common practice in energy companies to create synthetic forward FX curves using spot FX rates and published LIBOR curves. The divergence described above means that this approach is no longer a reliable way to generate a forward FX curve for MtM and risk measurement purposes. But scrapping the use of LIBOR altogether to focus on traded forward FX prices can create other problems. It is likely that some business functions within an energy company will need to use LIBOR rates (e.g. for contract settlement and treasury). So the challenge is finding a solution which recognises the divergence between LIBOR and forward FX rates but can handle the inconsistencies in the discounting of cashflows that may arise.