Prices in the latest T-4 capacity auction smashed UK records clearing at 30.6 £/kW (~€37/kW). This follows last year’s auction clearing price of 18 £/kW.

“There is a requirement for at least 30-40 £bn of flexible asset investment by 2035”

The latest auction is for delivery of capacity in 2025-26. By this point the UK coal fleet will be retired. The nuclear fleet is also closing more quickly than anticipated given safety issues with ageing plants. Sizewell B is the only nuclear plant with a T-4 capacity agreement in 2025-26.

By the second half of this decade the UK is set to lose 9GW of coal and nuclear capacity. In addition there is likely to be more than 7GW of ageing CCGTs that retire by around 2030. Renewable build is accelerating but on a derated capacity basis this is significantly outweighed by closures of coal, nuclear & gas plants.

The result? After a period of lower price outcomes, the UK capacity market is again providing a clear price signal for investment in flexible capacity.

In today’s article we look at the UK’s latest auction and what it reveals about how the capacity deficit is being addressed.

Batteries the clear winners

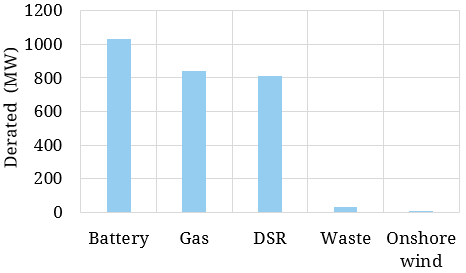

Almost 5GW of official ‘new-build’ capacity & almost 1GW of DSR was procured in the T-4 auction, split across interconnectors, gas peakers, storage, wind and waste. Only 1.9GW of that total represents genuine new-build with the interconnector capacity listed as ‘new’ due to a quirk in the capacity market rules. In addition there was 0.8GW of Unproven Demand Side Response (DSR) capacity that received one year contracts.

A breakdown of the 2.7GW of genuinely new capacity is shown in Chart 1.

Source: Timera Energy, EMR Delivery Body

The clear winners in the latest auction are batteries with 3.3 GW of new capacity successful (around 1GW derated). This volume represents around double the currently installed battery capacity in the UK. It is also more than 3 times the battery capacity successful in the last T-4 auction.

It is one thing to secure a capacity agreement but quite another to secure the cells and balance of system equipment required to build it. Battery projects are currently strongly impacted by global supply chain issues.

There is a shortage of input materials for manufacturers (driving up costs) and major delivery delays to buyers. There is also intense demand for cells from a rapidly growing EV industry. So while large UK battery project pipelines are quoted on a regular basis, there are very real constraints around turning concept into reality.

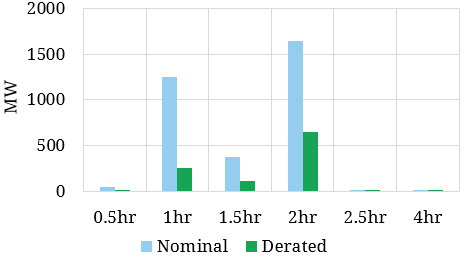

The 3.3GW of successful battery capacity represents around 5GWh of storage volume. Chart 2 shows the clear trend towards longer duration batteries, with 2 hour batteries now dominating new capacity. There were even a couple of projects of greater than 2 hour duration (one of 4 hours). However the impact of supply chain issues on cell costs may slow the extension of duration over the next couple of years.

Chart 2: Successful battery capacity by duration

Source: Timera Energy, EMR Delivery Body

DSR was also successful as a category, dominated by a range of small-scale Enel X and Flexitricity (Quinbrook) projects. There is not clear published information on what this DSR capacity is comprised of, but behind the meter batteries play a role, effectively expanding the battery volumes set to come online (vs those summarised in Chart 2).

Distribution connected gas engines continue to receive 15 year capacity agreements. There was also a successful OCGT project at Immingham. The limited duration of batteries leaves a key gap for provision of longer duration flexibility (e.g. from 2 hours to 2 weeks). As flexible coal & gas plants close, gas engines & OCGTs are stepping in to provide that longer duration flexibility to support the system through periods of low wind & solar output.

New CCGTs the clear losers

A range of new build CCGT projects have historically provided strong resistance to higher auction clearing prices. But despite the capacity price climbing over 30 £/kW, there was not a single successful CCGT project in the latest auction, despite over 5GW competing.

This reflects the growing decarbonisation risk for a large CCGT asset which has an economic life well into the 2040s. In the absence of a credible plan to decarbonise the emissions footprint of CCGTs, it appears they have effectively been removed as a competitive source of new capacity. The future of new CCGT projects looks to depend on an economic CCUS solution via the industrial clusters receiving fast track support from the government.

In terms of existing capacity exiting the auction, SSE’s ageing 670MW Medway CCGT failed to clear, highlighting the possibility of additional CCGT retirement across the next 5 years. Of the UK nuclear fleet, only Sizewell B pre-qualified despite EDF extending the life of Heysham 2 and Torness to 2028. This raises the risk of a further significant reduction in nuclear capacity against base-line projections.

Conclusions on flexible asset investment

There are 3 parallel forces at work driving up the returns on flexible assets:

- Rising capacity prices for 15 year contracts to support new build (as set out above)

- Rapidly increasing energy & Balancing Mechanism margins as market volatility has risen between 2020 & 2022

- The introduction of new revenue streams e.g. the Dynamic Containment frequency response service targeted at batteries.

Despite the rapid rise in flexible asset returns across the last 2 years, the UK still faces a substantial challenge to deliver adequate volumes of flexible capacity.

In a Briefing Pack we release this week, we set out the scale of the flexibility investment challenge required to decarbonise the UK’s power sector. This details:

- The scale of coal, nuclear & gas plant capacity closures (at least 30GW by 2035)

- The fact that closures are outpacing renewable capacity growth, despite accelerating wind & solar build

- The impact of power demand growth from decarbonisation of other sectors (transport, heat & industry)

- The structural market & policy drivers supporting flex asset returns

- The requirement for at least 30-40 £bn of flexible asset investment by 2035.

You can download this pack by clicking here.