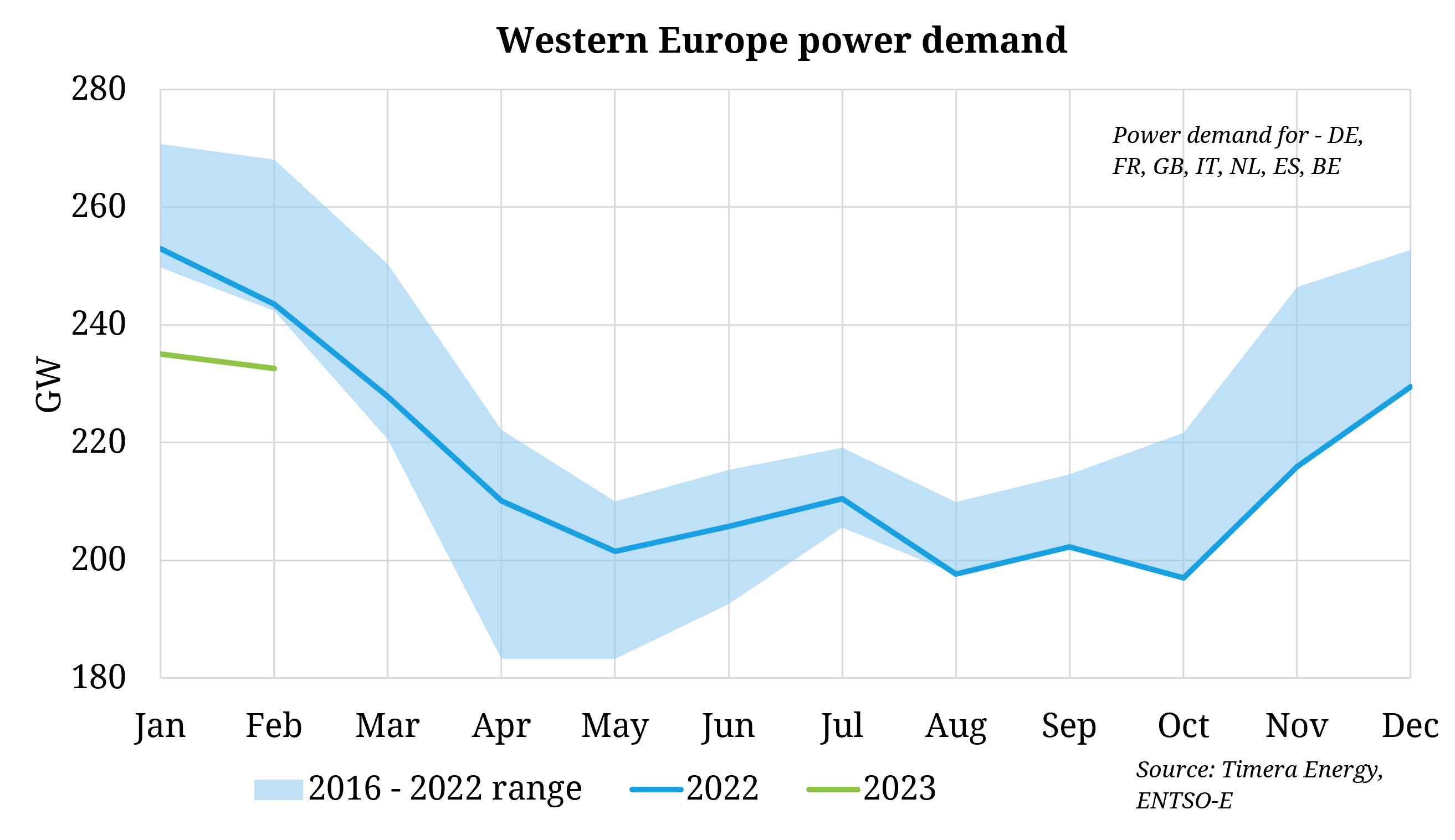

The parallel gas and power market crises in 2022 saw prices soar in a bid to reduce demand to balance the European markets. EU energy reduction policy echoed this, targeting a 10% reduction in power demand (including 5% reduction across peak periods) up until end of March 2023. A mild winter supported these efforts, with Western European demand at 5-year lows from August to December 2022, and an overall 5% drop in H2-2022 from H2-2021 levels (even against covid/lockdown suppressed demand).

Despite a decline in baseload power prices of ~50% from December 2022 to January 2023 (alongside a decline in TTF of similar magnitudes), power demand continued to drop by 7% year-on-year in January. The gap narrowed slightly in February but remains (down 4.5% y-o-y). Looking to ensure the trend continues, the EU is targeting energy demand reductions of at least 32.5% by 2030 on current levels.

The key question for policy makers in the short term and the economy in the long term remains; whether the demand declines have been temporary adjustments supported by warm weather, or a structural shift and offshoring of demand.