Multiple Western Europe regas capacity auctions are running concurrently through 2026, offering an opening for portfolio players to secure long-term terminal access into this key liquid market.

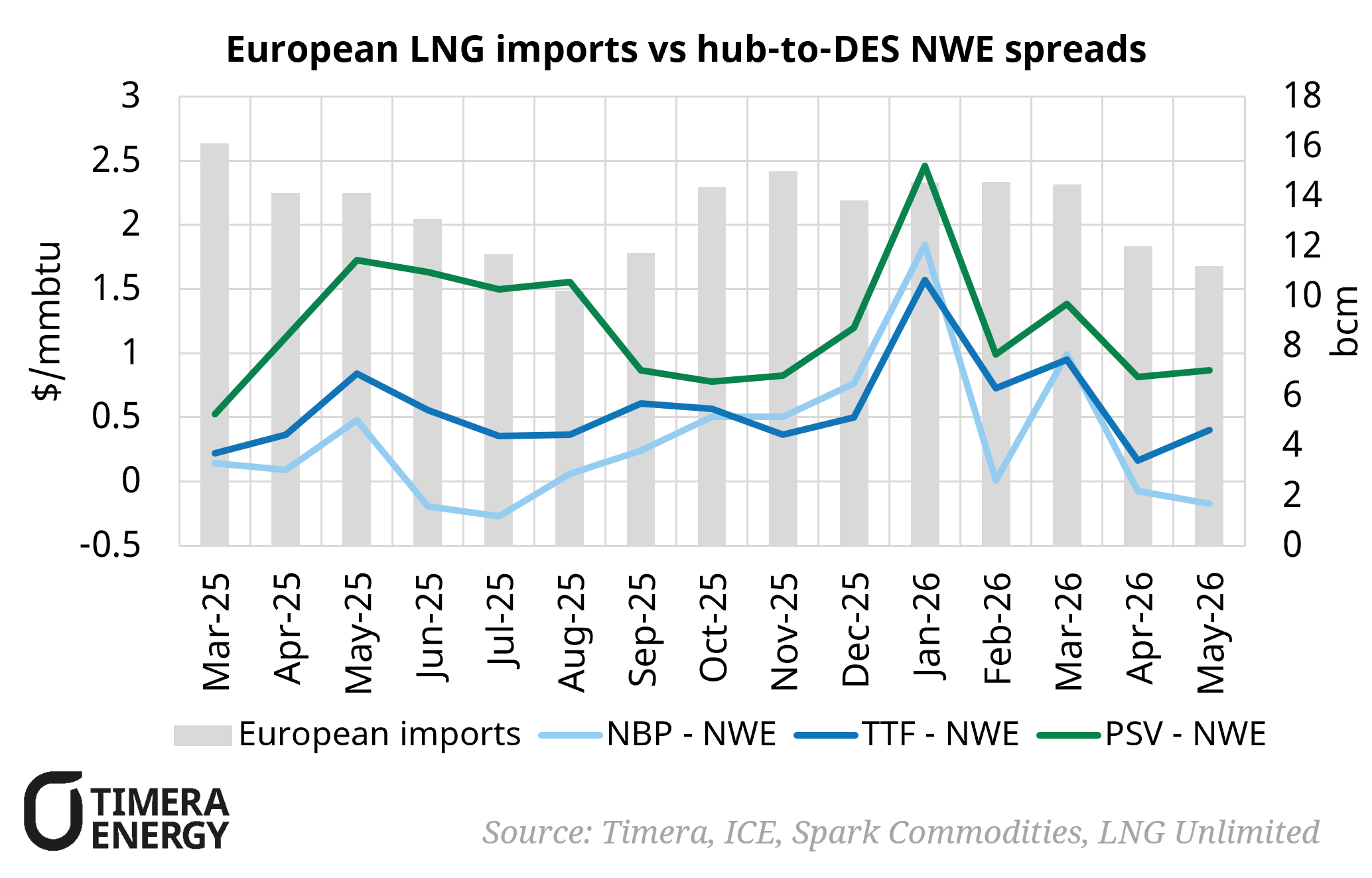

The chart below shows the recent evolution of the primary price signal driving regas value: onshore hub to DES NW Europe LNG spreads. The spread has eased back from its January peak as the closure of the Strait of Hormuz has led to European LNG imports pulling back from late 2025 highs.

But with a 200+ mtpa LNG supply wave building into the back half of the decade, the structural case for adding primary European regas positions into portfolios remains a key area of interest, particularly for those building Atlantic LNG supply positions into the coming wave.

Four processes are worth tracking, spanning binding auctions, expression of interests (EOIs) and new build open seasons:

- Dragon LNG (UK): a binding auction for ~9 bcm/yr of firm capacity from August 2029, with bids due 13 July. Tranches range from ~1.2 bcm/yr up to 100% of the terminal, with NBP access on a 10-year minimum term.

- Grain LNG (UK): an Expression of Interest for ~3 mtpa from October 2029 as contracts roll off, open until 15 July. This is information gathering only; any formal allocation will be confirmed separately.

- Zeeland Energy Terminal (NL): the VTTI / Höegh Evi FSRU (~7.5 bcm/yr from late 2029). EOI phase closed in March, with the commercial process expected to conclude by end 2026 ahead of FID in Q3 2027.

- Adriatic LNG (Italy): having offered capacity to 2050 in its autumn 2025 open season, a fresh round is awaited.

Getting the commercial and valuation framing with regards to European regas opportunities matters. As set out in this previous article, Timera has developed a robust approach to support market participants across European market access strategy, regas auction negotiation and capacity valuation. Reach out to David Duncan at david.duncan@timera-energy.com to discuss further.