“A near term shock with a longer term footprint”

Gas and oil prices fell sharply last week following the Middle East ceasefire announcement. However, the truce remains fragile with no clear path to a diplomatic solution, and uncertainty over the scale and timing of recovery in Hormuz cargo flows continues to drive significant market volatility.

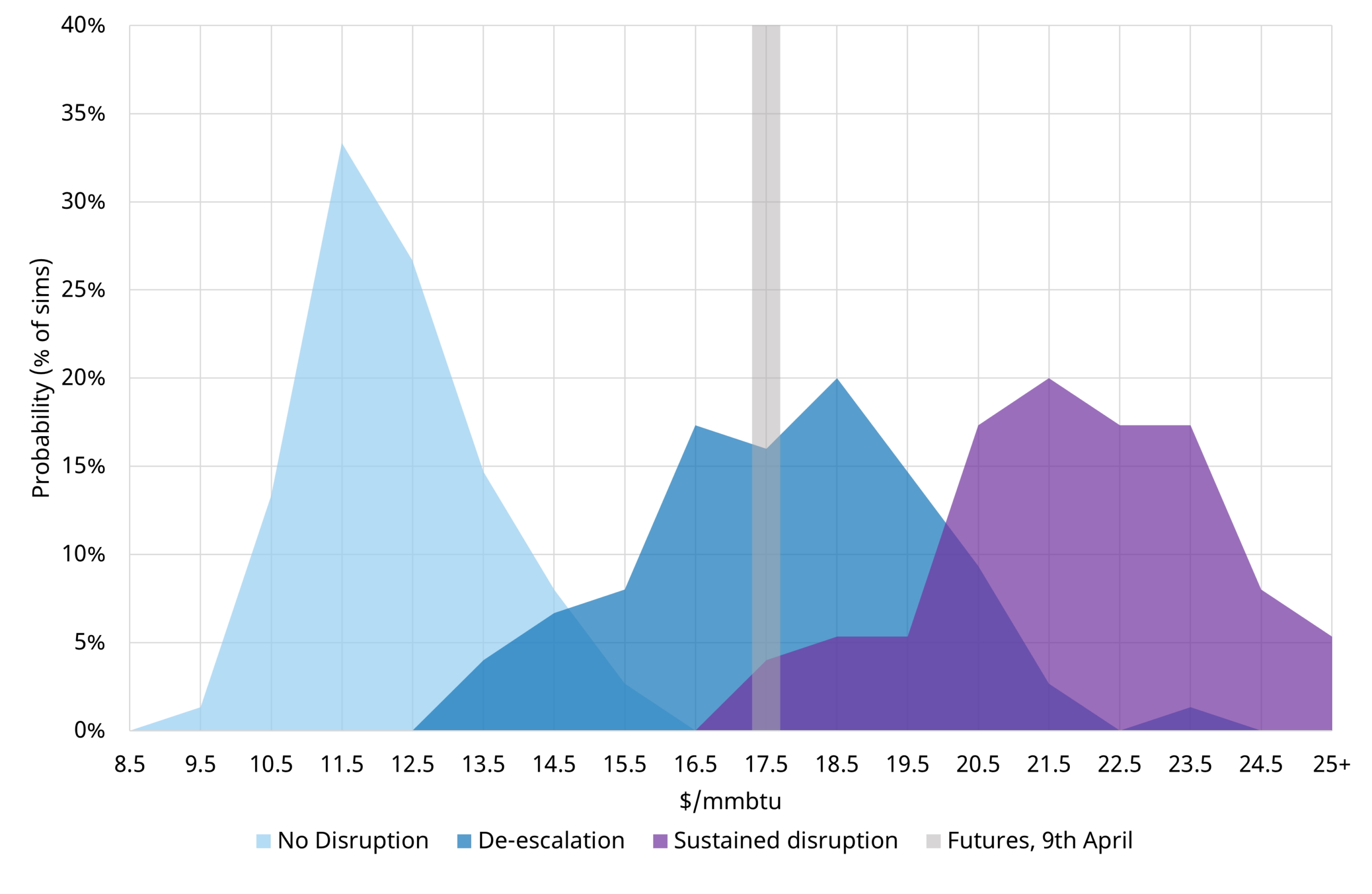

We recently modelled and published two potential LNG market scenarios in response to the supply shock (i) ‘De-escalation’ and (ii) Sustained Disruption.

The Summer 2026 JKM price distributions from this analysis are shown in Chart 1. The market price reaction so far over summer looks broadly consistent with our De-escalation scenario, which assumes a gradual resumption of Qatari LNG production beginning in May, followed by a ramp-up through June and July.

Chart 1: Summer 2026 scenario based JKM price distributions

Source: Timera Global Gas Model

Regardless of whether the ceasefire proves durable, the crisis is likely to have longer-term structural implications for both the supply and demand sides of the global LNG market.

Supply side: damage so far relatively contained

The central supply-side question is how the enduring impacts of the conflict interact with the large wave of new LNG capacity coming online – more than 200 mtpa by 2030 (an almost 50% increase vs 2025).

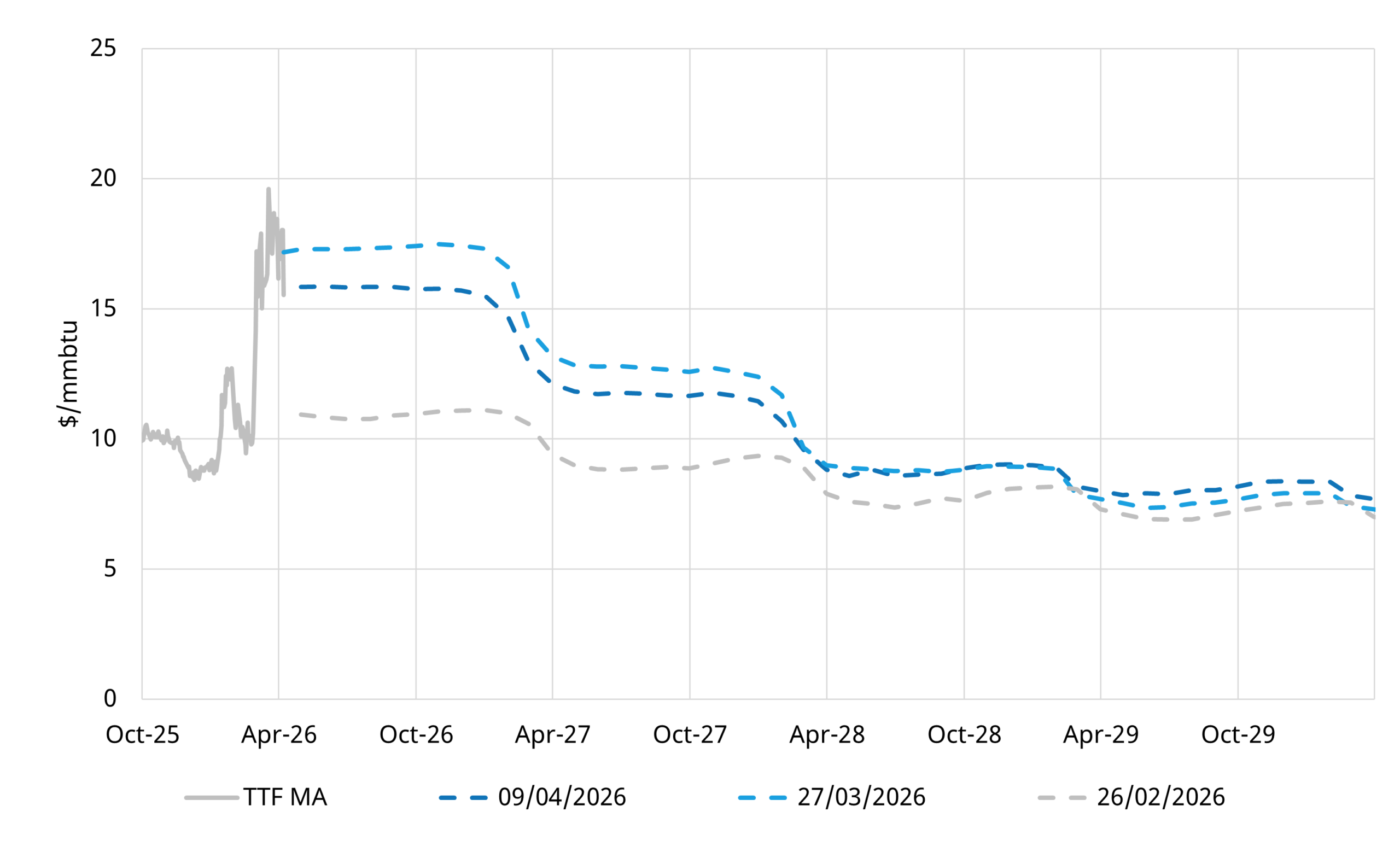

Chart 2 shows how the summer 2028 onwards portion of gas forward curves has remained relatively anchored despite the conflict. Price increases have been concentrated in the front end of the curve, resulting in a pronounced steepening of curve backwardation. This reflects a market view that the supply overhang will ultimately reassert itself in the medium term, with the impact of this crisis temporary, not structural.

The most concrete enduring supply impacts to date relate to Qatari production. This is both via damage to Ras Laffan South trains 4 and 6 and delays to new trains coming online. We estimate this will remove ~15-20 mtpa from the market through at least early 2029 (relative to our pre crisis outlook).

Our modelling indicates that this disruption does have some impact on prices out to 2029, though the effect is progressively dampened by the scale of new supply coming online. In short: the damage is material, but not sufficient to fundamentally alter the medium-term supply picture.

The supply outlook in 2030 remains broadly unchanged, although beyond this point the crisis could lead to investment patterns shifting as the market moves into a more uncertain pre-FID project horizon.

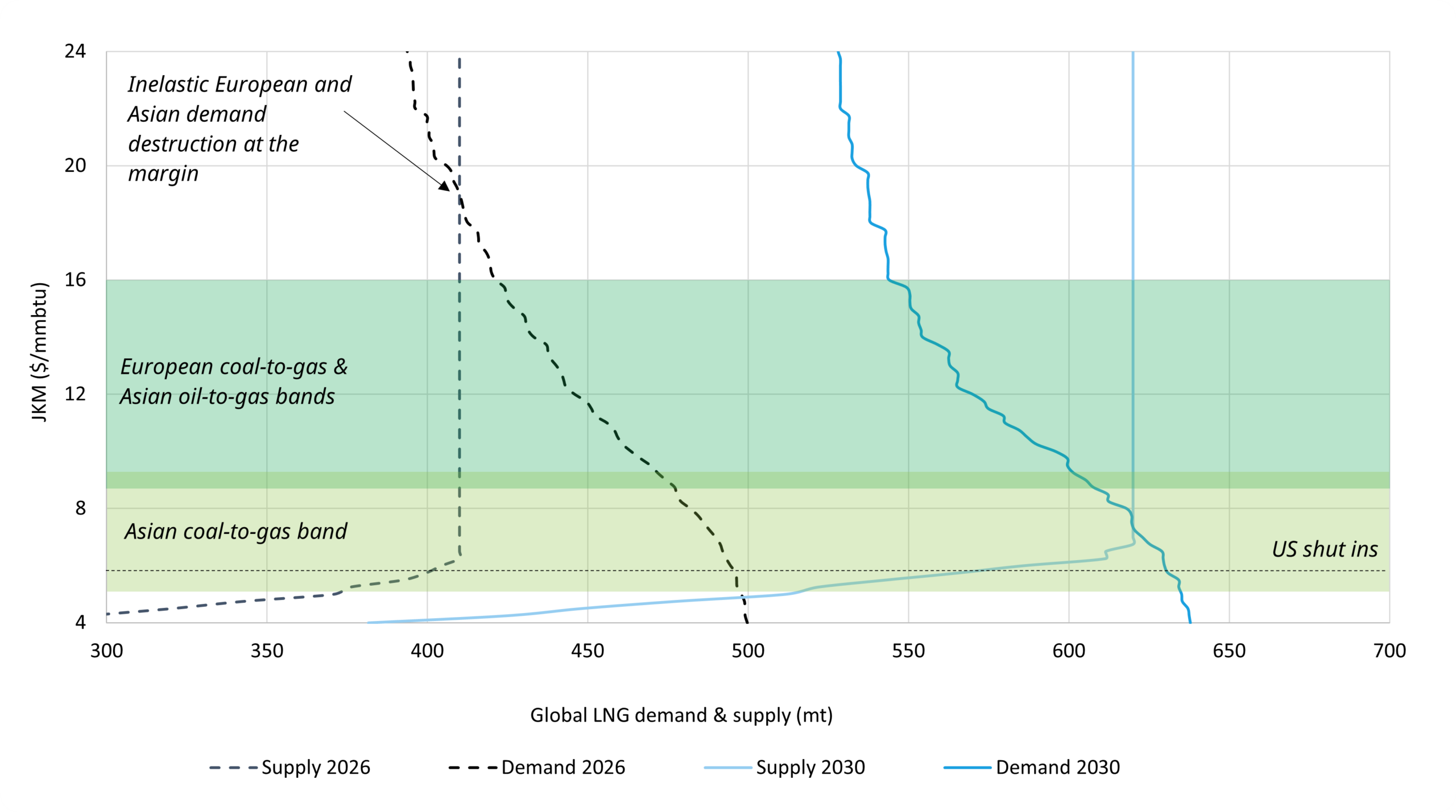

We illustrate LNG market supply & demand curve outputs from our global gas market model in Chart 3. The chart higihlights the scale of the impact of new supply coming online by 2030 (represented by a significant rightward shift in the supply curve). This increase materially outweights current Qatari supply disruptions and exerts downward pressure on global LNG prices, as the market must clear through demand creation at lower price levels.

Chart 3: LNG market supply & demand curves 2026 vs 2030 (illustrative scenario)

Source: Timera Global Gas Model; the shaded bands are schematic representations of our modelled switching prices

Demand side: nuanced and harder to read

The enduring demand impacts of the crisis are more complex. Supply disruption and sustained price volatility are likely to be net negative for LNG demand growth at a critical point in the market’s development as summarised in Table 1.

Five commercial implications for LNG players

We are seeing five clear themes emerging across our LNG client base in response to the crisis:

- Location-differentiated supply. Marginal buyers are placing a growing premium on security of supply by source and on portfolio diversification. This is broadly positive for producers in Africa and South America, and a headwind for Middle Eastern suppliers.

- Tighter end-user demands. Buyers are focusing harder on contractual supply risk mitigants – more volume flexibility, shorter price review terms, and stronger force majeure protections.

- Bankability pressures. Concessions to end users on flexibility and pricing terms reduce the bankability of supply deals. For projects dependent on long-term offtake to secure financing, this creates tangible challenges.

- Indexation caution. The shock has heightened wariness around both JKM and TTF indexation, given the volatility these benchmarks have exhibited. Brent indexation offers no easy refuge either. The result is growing interest in hybrid pricing structures that blend benchmarks or introduce floors and caps.

- Commercial agility. The broader backdrop, a wall of new supply coming online through the late 2020s, continues to weigh on contracting. The shock may provide incremental support for deal-making, but the buyers and sellers that capture value will be those with the commercial sophistication to structure genuinely flexible, risk-appropriate deals.

We will be having a more detailed discussion on the supply shock, LNG market state of play and commercial implications in our webinar tomorrow (Tue 14th) – see details below.

Join our upcoming webinar “From crisis to supply wave: navigating global gas uncertainty”

Time: 0900 BST (1000 CET, 1600 SGT)

Date: Tues, 14th, April, 2026

Pre-registration is required. Please visit this link: https://attendee.gotowebinar.com/register/3412496419270133853?source=blog

Coverage:

– Middle East supply disruption: a framework for assessing impacts on global balances, pricing, and market uncertainty

– The next LNG wave: how new supply impacts a repriced global gas market

– Portfolio implications: key themes for asset value and portfolio strategy

Timera Energy advises LNG producers, buyers, traders and investors on portfolio valuation, commercial strategy and market risk. Feel free to reach out to our LNG & Gas Director, David Duncan (david.stokes@timera-energy.com) for more details.