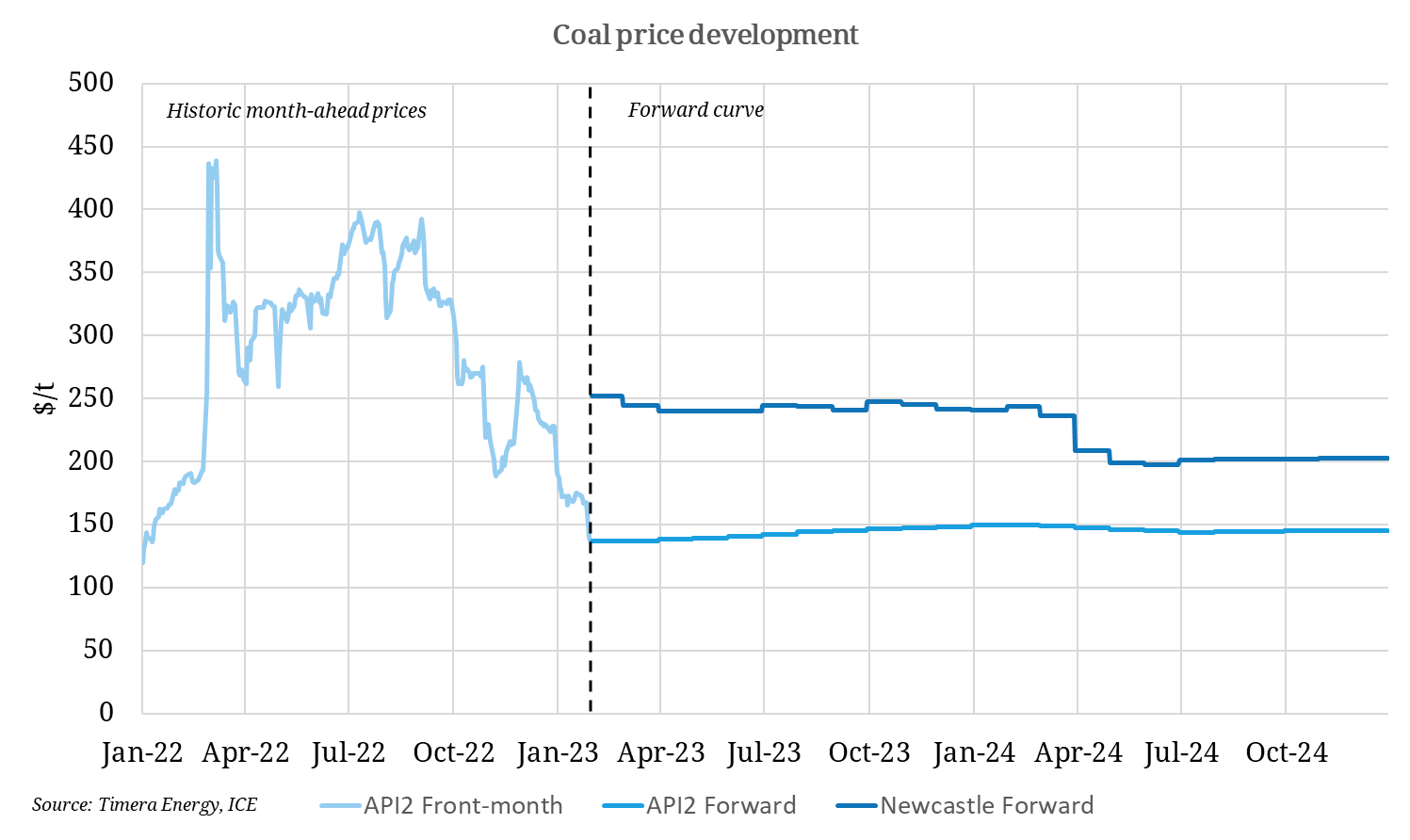

European coal futures (API2) have declined sharply over the past few months, with the Mar-23 contract dropping by 50% since late November to $137/t. The European coal market has followed the drop in European gas & power prices, as concerns over fuel shortages eased on mild winter temperatures and weakened industrial demand, feeding into reduced coal demand in the Continent. Gas prices have dropped sharply to start nearing levels required to begin pushing coal out of the generation mix. In addition, ARA coal inventories are at around four-month highs of over 6 million tonnes in January, approximately a third higher than last January, reducing buying activity as buyers risk leaving material idle at ports.

The Asian coal market has diverged massively compared to Europe, exemplified by the record-high price spread between them. Newcastle prices have tripled their premium over API2 prices from ca. $40/t before Russia’s invasion of Ukraine to $120/t on the Mar-23 futures contract. Historically, Newcastle coal prices have averaged a premium of just under $6/t over API2 in the past 10 years. A more bullish sentiment in Asian coal markets has been driven by a tight Pacific Basin market and expectations of higher demand, as the world’s largest coal importer China reboots its economy this year following COVID lockdowns throughout 2022. Last year saw Australian coal exports dogged by weather-related production issues and ongoing labour shortages. China has recently lifted its unofficial ban on Australian coal imports imposed two-and-a-half years ago, supporting a ramp up in steelmaking activity which has been buoyed by major stimulus measures from Beijing.