“The TTF premium is back”

European gas hub prices have strengthened materially in recent weeks vs Asian markers. This reflects low storage levels in Europe driving stronger demand for LNG cargoes.

Within Europe, offshore LNG to onshore gas hub price spreads have also blown out. DES NWE prices have opened up a significant discount to TTF, improving the moneyness of regas capacity slots for players already holding regas capacity.

Let’s dig into what is going on.

Low storage inventories supporting TTF

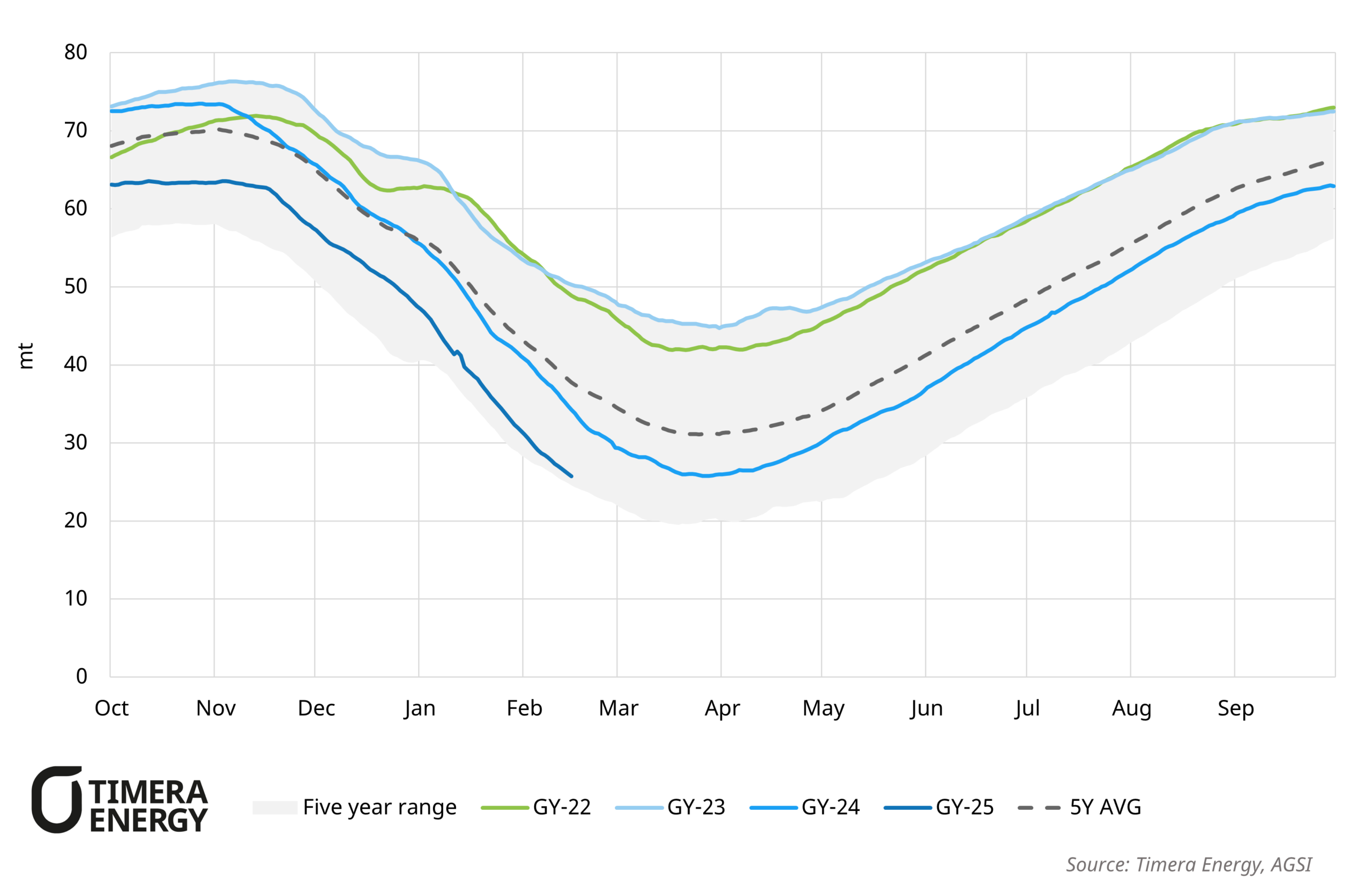

TTF prices are being supported by below-average storage levels as shown in Chart 1, with a price premium to JKM required to attract adequate LNG cargo flow to meet European demand.

Aggregate European inventories are currently at ~25 mt, towards the bottom of the 5 year range. This has increased market sensitivity to late-winter supply risk and the upcoming refill season.

Chart 1: Aggregate European storage inventories

Source: Timera Energy, GIE

Onshore price premium boosting regas margins

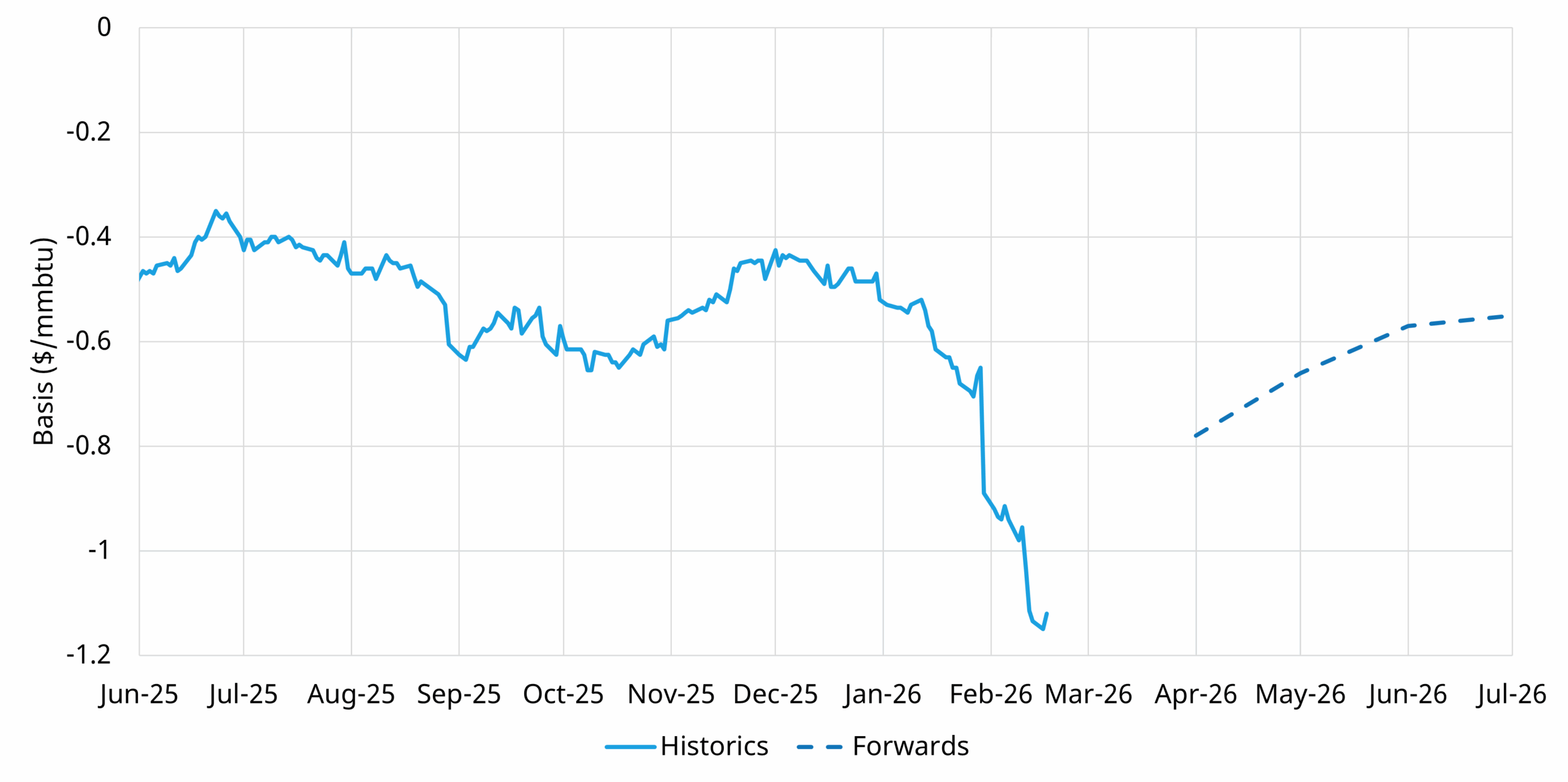

Chart 2 highlights the resulting shift in offshore-onshore price spreads. The front month DES NWE–TTF basis has widened to around 1.00 $/mmbtu, a level at which most Northwest European regas terminals cover variable costs and return to positive merchant margins on imported LNG.

This widening offshore–onshore spread increasingly reflects tighter utilisation and growing competition for regasification capacity within Europe as LNG inflows rise and capacity constraints emerge.

Chart 2: Front month DES NWE – TTF price spread

Source: Timera Energy, Spark

This marks an important shift in market dynamics. Merchant regas capacity typically sits at or out of the money, with holders relying on incremental portfolio optionality to justify long-term bookings. The recent move into the money, however, highlights the potential for higher extrinsic value to accrue during periodic episodes of strong utilisation and elevated spreads.

UK divergence limits margin uplift

The spread-driven uplift has not been uniform across Europe. In the UK, NBP has weakened relative to TTF, reflecting stronger LNG cargo demand on the continent. This has meant weaker UK regas margins, with the UK’s higher relative terminal cost base contributing.

The result is growing intra-European divergence in regas value, which is influencing marginal cargo routing decisions within the Atlantic basin.

5 commercial implications

Let’s finish with 5 commercial takeaways:

- Late-winter risk premium: cooler weather & low storage inventories are supporting TTF risk premium and volatility.

- Regas in the money: most continental European regas terminals are ‘at’ or ‘in the money’, as offshore – onshore spreads support import margins for holders of primary capacity.

- Regas flex value up: The value of optionality (flex value) associated with terminal access and short-term capacity has risen, particularly for LNG portfolio players.

- UK regas value softer: the discount of NBP to TTF reflects a weaker price signal for cargo flow to the UK, resulting in less attractive regas margins.

- Distributional impact: widening DES–TTF spreads improve economics for regas capacity holders, while players without secured capacity face higher secondary access costs and tougher economics.

Looking ahead, the persistence of European regas margin strength will depend on whether the TTF risk premium holds through the refill season and whether Asian demand tightens regional LNG pricing.

We continue to support LNG portfolio players with European market access strategy and negotiation support, covering market outlooks, regulatory risks, standalone value and value of integration into wider portfolios. Feel free to reach out to our LNG & Gas Director David Duncan for more information (david.duncan@timera-energy.com).