“The system needs gas… but investors need returns”

For more than two decades, CCGTs have provided the flexible backbone of the GB power market. They have provided flexible generation output to fill gaps around renewables, supported security of supply, and dominated marginal power price setting. But similar market forces that pushed coal out of the system are now challenging the economics of gas-fired generation.

The gas era is ending faster than markets expected

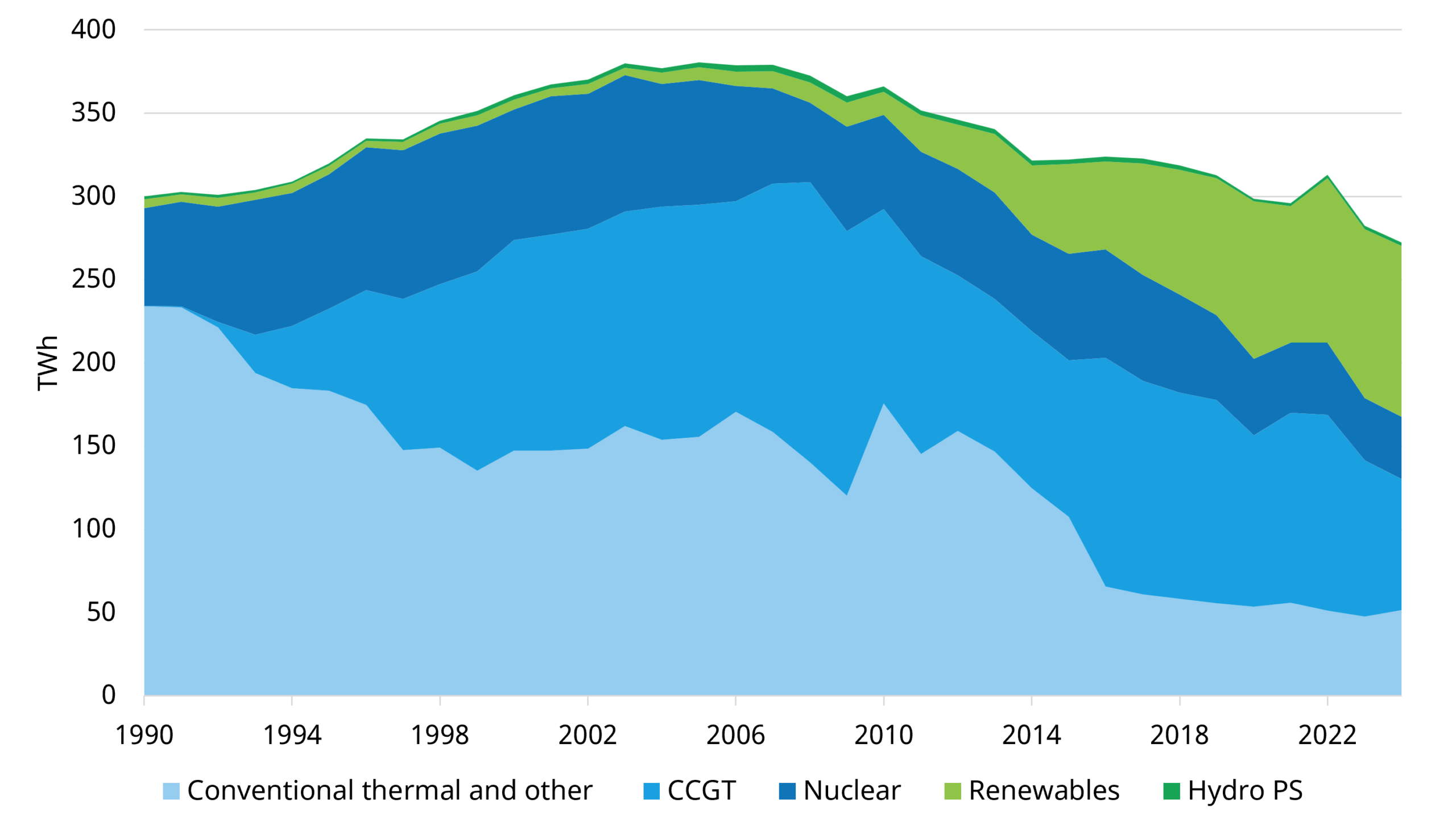

The historic GB supply mix shows a clear story. Thermal generation has been in structural decline for more than a decade, while renewables have taken a steadily larger share of supply.

Gas remains the last dispatchable backstop in the system. That makes it critical during periods of low wind, low solar, high demand or system stress.

BESS and LDES are not direct replacements for gas flexibility. Storage enables the movement of energy across relatively short time periods. But it is a net consumer of energy – in other words it cannot add incremental energy to the system to deal with prolonged periods of low wind & solar output.

As RES penetration increase, the role of gas is moving away from regular mid-merit generation and toward infrequent, high-value periods of system tightness. That shift changes the revenue stack. Gas asset value capture is becoming more focused on extrinsic energy margin from price volatility and capacity payments.

Renewables are pushing gas off the margin

Gas is still the marginal price-setter for a significant share of GB settlement periods. But Chart 2 shows how our stochastic market modelling points to a steady decline in the number of hours set by gas as renewable output grows.

As renewables expand, gas assets are pushed further up the merit order. They clear less often and load factors fall. Revenues become more concentrated in tighter market periods, particularly stress events.

That is the central problem for the sector. A plant may remain valuable to the system because it is available when needed, but it may not earn enough from normal market operation to justify ongoing investment.

This is particularly challenging for gas assets that are structurally out-of-the-money on an intrinsic basis. If core energy margin is weak, owners need enough extrinsic value & capacity payments to cover fixed & variable costs, maintenance capex and risk.

An ageing fleet with no replacement in sight

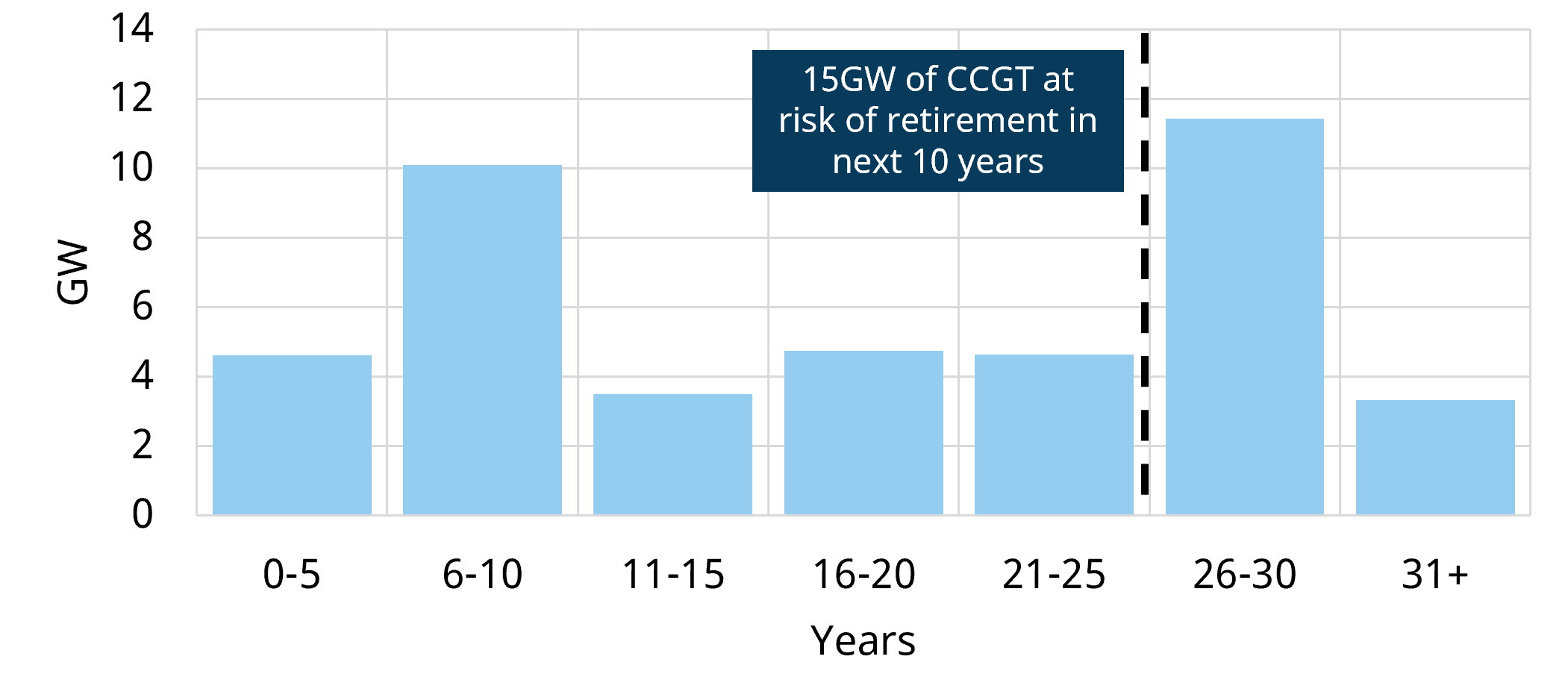

The GB CCGT fleet was largely built in two waves: the 1990s “dash for gas” and a second build-out in the mid-2000s. Much of the fleet is now 20 to 30 years old, with a material volume moving into the age range where major refurbishment capex is required to keep assets running.

Age brings rising Operation & Maintenance (O&M costs), declining reliability and tougher life-extension choices. Retirements are already accelerating, and Chart 3 highlights our analysis of around 15 GW of CCGT capacity at risk of retirement over the next 10 years.

In a normal investment cycle, ageing capacity would be replaced by new build. But that is not happening.

Despite Capacity Market clearing prices reaching record highs – £65/kW in the T-4 2024 auction – investors are not prepared to commit to large capex new plants with asset lives extending beyond 2050. No new gas cleared in the most recent T-4 2029/30 DY auction, and with the price clearing at £27/kW, the economics for multi-year refurbishment commitments didn’t stack up for most participants. Around 14GW of gas plants entered under refurbishment agreements, initially prequalifying for both 3-year and 15-year contracts, however only ~1.5GW gas plants took a 3-year agreement and ~11GW opted for 1-year contracts. The low clearing price left participants instead opting to extend plant life into the early 2030s ahead of eventual retirement, rather than committing capital to significant refurbs.

Gas recip engines have the advantage of lower capex, lower start costs and greater flexibility. But gas engine build volumes in capacity market are also declining given low load factors and increasing policy risks.

The uncomfortable firm capacity gap

This creates a growing challenge for GB security of supply.

Retirements, limited new build and rising demand point to a looming firm capacity gap. Demand growth from EVs, heat pumps and data centres will increase the need for reliable supply during periods when renewable output is weak.

Interconnectors and batteries will help. They are essential sources of flexibility. But they are not substitutes for dispatchable thermal generation during multi-day low-wind, low-solar events.

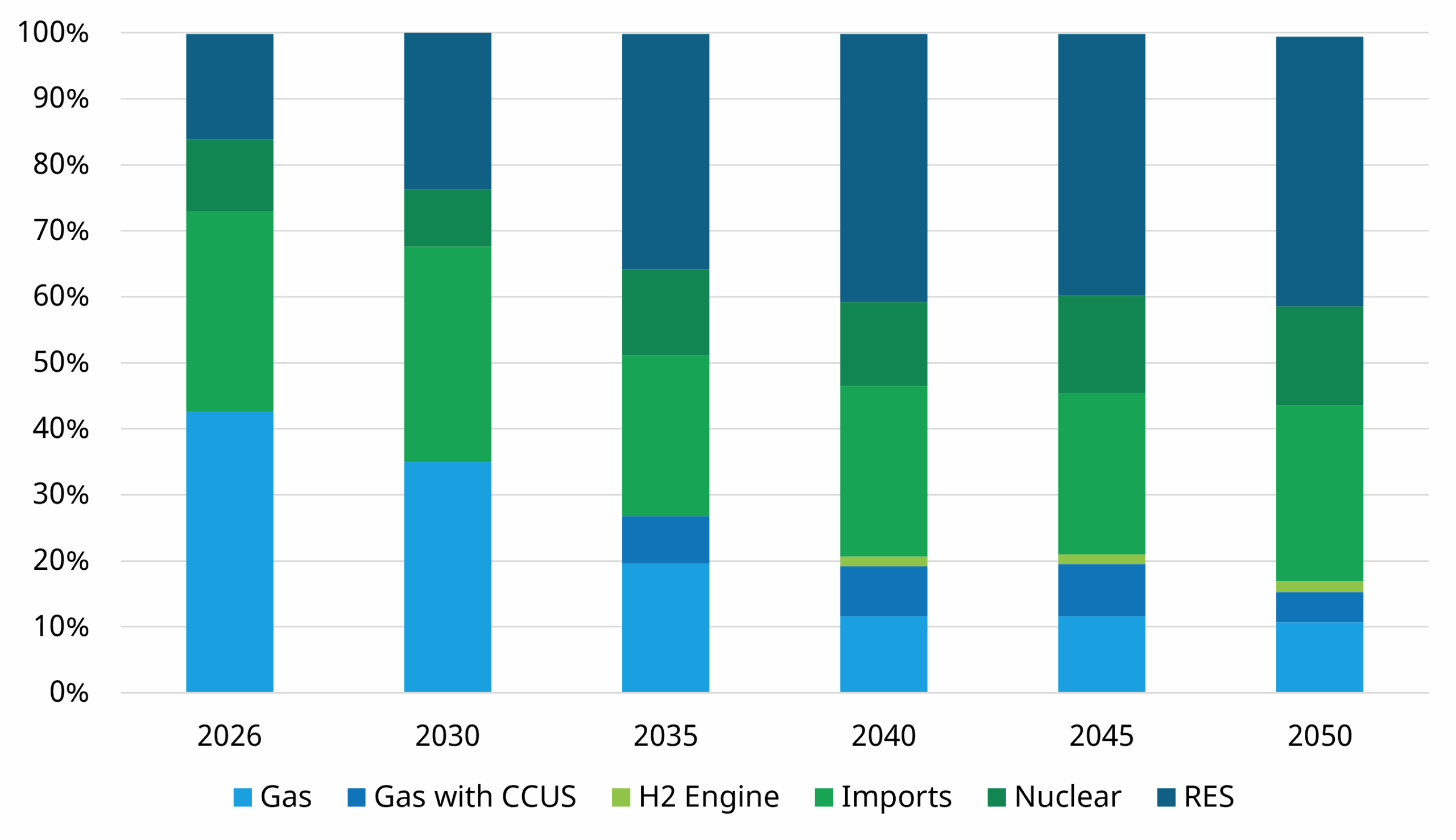

That leaves three options for maintaining GB security of supply:

- Rely on the delivery of new firm low-carbon capacity at scale – but this is a high risk strategy given challenges in scaling LDES, CCS-enabled gas and hydrogen-fired generation

- Extend the lives of existing CCGTs, but this becomes more expensive and uncertain as the fleet ages

- Or try and incentivise more gas-fired recip engine capacity to provide low load factor system back up

GB is not alone. The same dynamic is emerging across Northwest European power markets: ageing thermal backstop capacity, rising renewables, growing electrified demand and weak investment signals for new unabated gas.

Gas will not disappear from GB power markets in the near term. But its economics are becoming challenging. The market is moving toward a “last gas standing” problem: the system still needs gas capacity, but the investment case for keeping it available is becoming harder to sustain.

Challenges may fuel transaction activity

As gas assets value transitions towards extrinsic margin and end of life economics, risk / return profile shifts as does the ‘natural owner’ of these assets.

This is likely to drive M&A activity with a shift in ownership from IPPs and utilities to private equity funds and trading focused companies with higher risk tolerance.

There is often high value optionality around asset flex enhancements, life extensions and site value as well as cost efficiencies that are better monetised via private equity than a utility.

A good example of this was Riverstone buying Engie’s coal assets in Germany & the Netherlands in one of the more profitable power portfolio acquisitions of recent history.

The market may be challenging for gas, but that does not mean existing flexible assets have no value. But it does mean that the value is changing hands.