‘Battery storage flexibility is a key building block of a decarbonised power sector.’

This statement is not a myth. In fact it is almost a truism.

Intermittent renewables will dominate electricity supply in a decarbonised world. Wind and solar output require a low carbon source of flexible backup. Rapidly declining battery costs will facilitate broad deployment. Sound familiar?

While there is a broad consensus around the vision for batteries, the practical details of the business model and investment case for individual battery projects is less clear. In today’s article we challenge three ‘myths’ currently circulating in relation to battery investment.

‘Myth’ 1: Batteries shift load to smooth renewable output

While in theory batteries can be paired with renewables to smooth intermittent output, this does not represent a viable business model to support battery investment. There are three main reasons for this:

- Duration: Investment is currently focused on 0.5-2.0 hour lithium-ion batteries, which are seeing the steepest & fastest cell cost declines. The short duration of these batteries significantly limits the volumes of energy that can be moved between time periods.

- Degradation: A focus on shifting load requires deep cycling. This shortens the life of lithium-ion batteries and accelerates the costs of cell replacement, undermining project economics.

- Returns: Cycling batteries to shift load is not commercially optimal. The returns from load shifting (e.g. full cycle to capture cheapest offpeak hour vs highest price peak hour) are well below those required to support investment.

Maximising battery returns involves the complex optimisation of battery optionality against multiple markets including wholesale (e.g. day-ahead and within-day prices), balancing markets and network services.

The logic above does not preclude successful co-location of batteries with solar or wind projects. But the benefits of doing this are focused on cost reductions (e.g. shared infrastructure & connection) and portfolio risk diversification, not on load shifting.

Battery flexibility will also play a key role in dampening price fluctuations which are driven by intermittent renewable output. But with shorter duration batteries this is via multiple shallow cycles to respond to short term price volatility rather than deep cycling in order to shift load.

A viable investment case for longer duration, deeper cycling storage solutions (e.g. flow batteries) looks to be at least five years away.

‘Myth’ 2: Battery investment is being underpinned by network services

The UK and Germany are leading European investment in batteries. Early projects in both markets have been supported by network services contracts (e.g. the UK EFR contracts tendered in 2016 for very rapid frequency response services). But battery investment cases being developed today have turned to focus on merchant returns.

Revenue opportunities from network services remain. This includes both grid services for transmission connected projects (e.g. frequency response, reactive power) as well as local/site revenues for embedded batteries. But the value of these services has been declining and contract horizons shortening as competition to provide flexibility increases. For example, prices for frequency response services in both the UK and Germany have fallen significantly over the last three years.

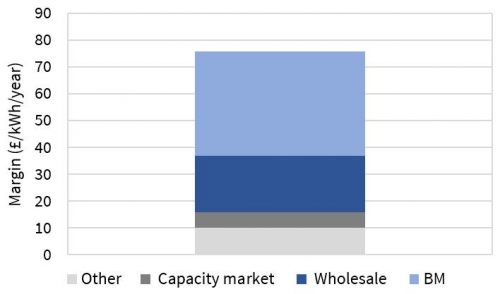

As a result, battery investment cases are being built on a ‘margin stacking’ model. This includes a base of more stable returns e.g. capacity payments, ancillary services & local site revenue. But merchant returns from wholesale and balancing markets are key to bridge the gap required to sign off a bankable project. An example of a margin stacking model in a UK battery project is shown in Chart 1.