“Offtake structure has become a key value driver”

Battery route-to-market structures are becoming an increasingly important value driver for BESS investors. In today’s article we focus on GB as Europe’s most mature BESS offtake market – but many of the conclusions apply across other European markets.

As ancillary service revenues have fallen and merchant optimisation has become more competitive, offtake negotiations are shifting from simple optimiser selection to more sophisticated offtake structuring.

We look at the key offtake structures being used by investors and set out 5 key focus areas for an effective route-to-market strategy.

The 4 core BESS offtake structures

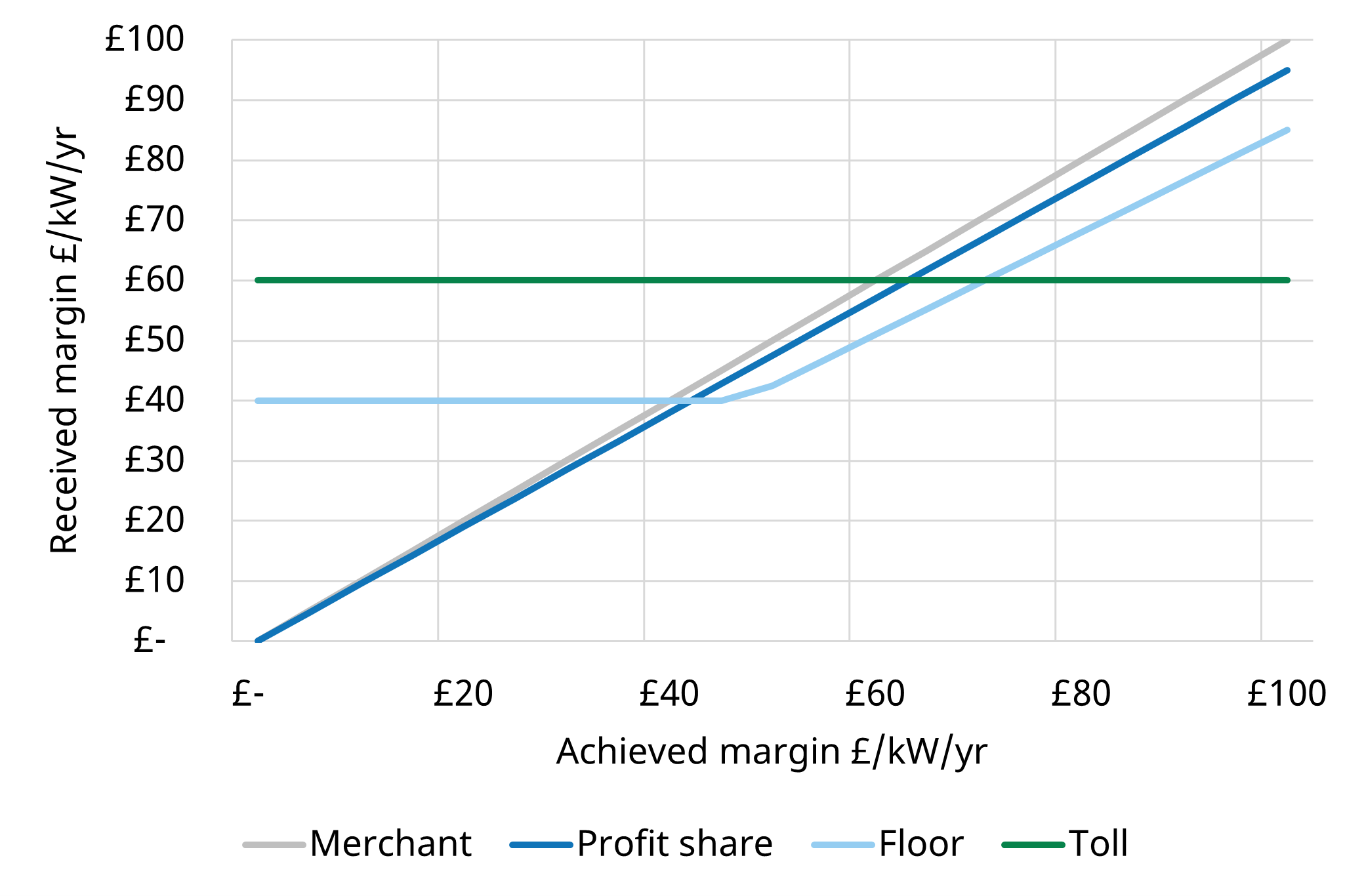

There are four main commercial structures currently shaping the GB battery offtake market, summarised in Table 1.

Table 1: Core BESS offtake structure options

The payoff profiles are illustrated in Chart 1.

Three important factors drive offtake structure selection:

- Debt financing – Revenue protection provided by tolls and floors enable project financing, that can significantly enhance equity IRRs. Bankability of the offtake provider is important (noting that the entity underwriting the toll/floor can be third party).

- Equity downside protection – Floors also provide equity investors with protection from weaker market conditions – paid for by giving away upside (e.g. higher margin share %) or additional annual fees.

- Upside access – Viable returns on equity rely on a structure that enables enough retained upside. Profit share structure (often tiered) is important, but investors are increasingly exploring other hedging instruments such as day-ahead swaps.

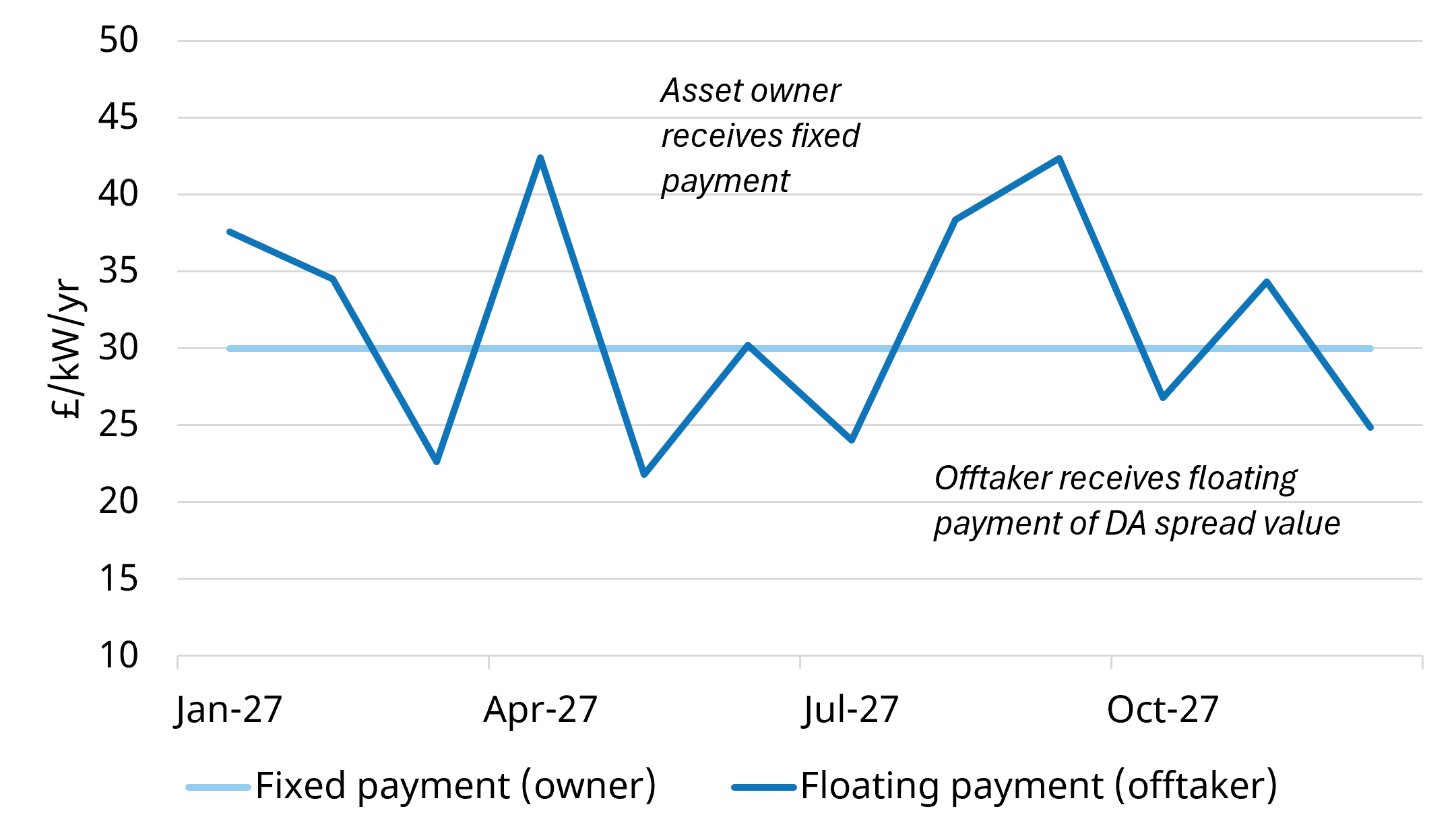

Day-ahead swaps and index-linked approaches are emerging in the GB market

Day-ahead (DA) swaps

A DA swap is a financial instrument layered on top of an underlying route to market structure. The asset owner receives a fixed payment and in return pays the offtaker a floating amount, indexed to a defined DA spread

As shown in Chart 2, the asset owner receives a fixed payment and pays the offtaker a floating amount linked to the capturable day-ahead spread (e.g. spread between two highest vs two lowest priced hours). This effectively acts as a hedge on the day-ahead spread exposure of the battery.

These structures are financial rather than physical. They can sit above different underlying optimisation arrangements, but they introduce basis risk. The floating leg may be calculated using an agreed methodology for day-ahead value, while realised asset performance will depend on degradation, availability, cycling strategy, round-trip efficiency and operational constraints.

Index-linked structures are also emerging in GB, with the Modo battery performance index one example of a settlement reference. These products may support benchmarking, but have clear limitations: they do not provide downside protection and effectively cap value performance at fleet-average outcomes.

Five key takeaways for effective offtake structuring

1. Start with the investment case, not the headline price.

The optimal structure depends on leverage, target return, risk appetite and portfolio dynamics. A toll, floor or profit share can each be right depending on whether the asset is being financed for stable yield, merchant upside or a blended risk-return profile.

2. Value downside protection explicitly.

Floors and tolls reduce revenue volatility, but protection is paid for through lower upside or higher optimiser economics. Investors should explicitly quantify BESS value sacrificed for downside protection using stochastic analysis.

3. Assess optimiser capability as part of the economics.

For any structure with residual merchant exposure, optimiser quality materially affects realised margin. Investors should assess track record, forecasting capability, market access, automation, optimisation frequency, reporting transparency and treatment of third-party versus owned assets.

4. Managing basis risk via swaps and index products

Financial overlays can offer useful alternatives, but do not necessarily improve risk adjusted returns. Value needs to be carefully modelled to account for hedge volumes, degradation assumptions, cycling constraints and outages. Otherwise, a structure designed to reduce risk can create a new mismatch between financial settlement and physical asset performance.

5. Consider multi-offtaker strategies across a portfolio.

RTM decisions do not need to be uniform. Splitting assets, or capacity within assets, across multiple optimisers can reduce concentration risk, create live benchmarking and allow investors to combine structures. This is particularly valuable where investors want both downside protection and merchant upside.

As BESS markets mature, offtake strategy is becoming an increasingly important driver of asset value. Focusing on the 5 areas above helps ensure offtake structure is a source of competitive advantage.

Timera supports BESS investors across Europe with offtake strategy, structuring and commercial analysis. For more details, contact Lucienne Hill Smith (Senior Analyst) lucienne.hill.smith@timera-energy.com.