“Italy has now entered a new intense auction phase for BESS”

Terna’s latest forward storage procurement plan, recently endorsed by ARERA, sets total utility-scale storage needs at 42 GWh by 2030 across Southern Italy and the islands.

That figure has been revised downward consistently: from 71 GWh in 2022, to 50 GWh in 2024, and now to 42 GWh, with roughly 10 GWh already contracted in the September 2025 MACSE auction.

The next MACSE round is targeting 2029 COD and is expected in Q4 2026. It therefore carries a maximum quota of 16 GWh – although this may be reduced by the Southern BESS capacity eventually awarded in next Capacity Market 2028 auction, expected by July 2026.

The MACSE and Capacity Market (CM) mechanisms are now running in parallel to procure BESS, with some key regulatory parameters still under consultation. In this article we look at both opportunities and challenges facing Italian BESS investors.

MACSE 2029: high competition baked in from the outset

The four bidding zones from the latest auction have been confirmed. North and Centre-North remain excluded from MACSE tenders: for investors there, the Capacity Market is the regulated route to contracted revenue streams.

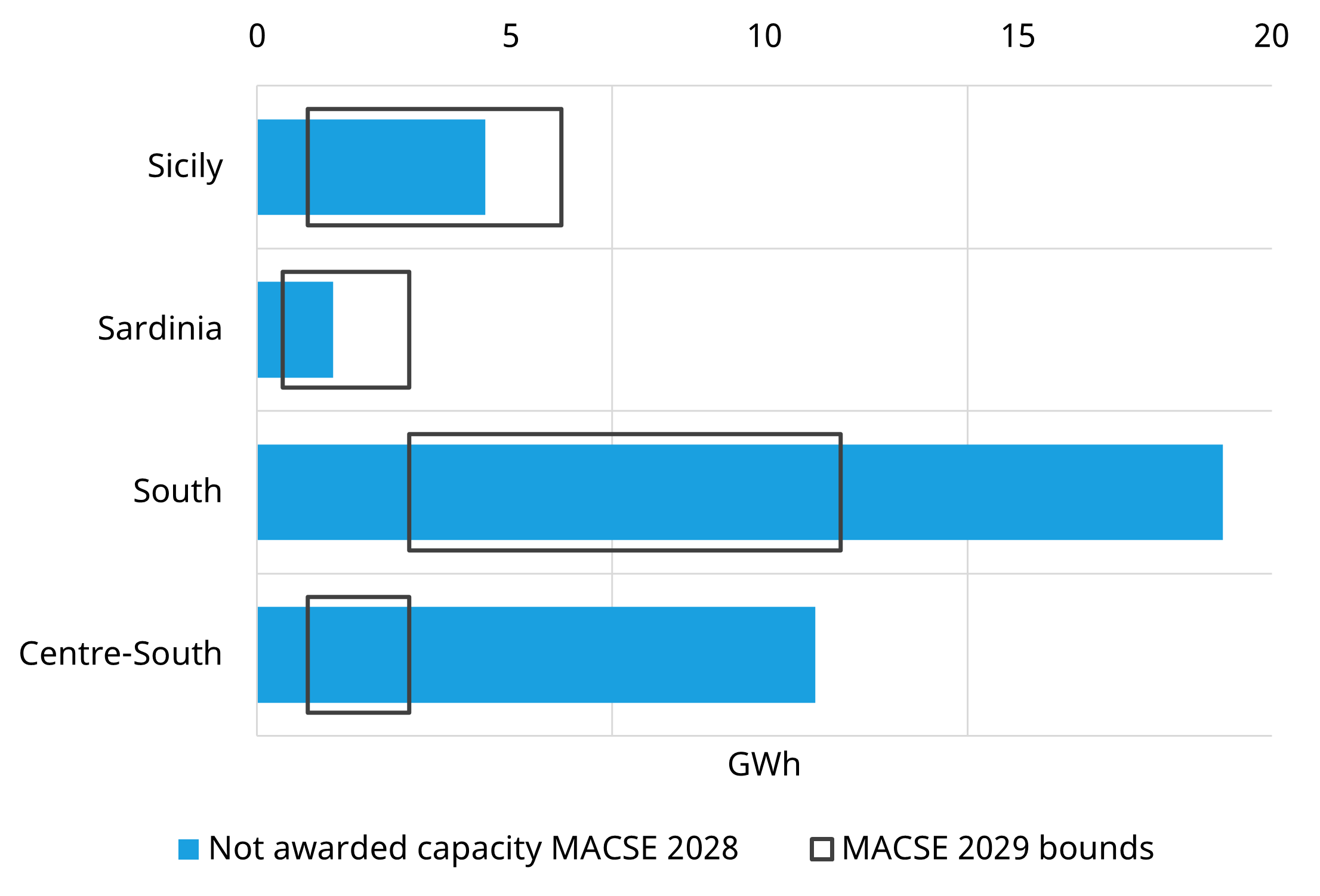

Chart 1 compares Terna’s upper and lower bound zonal quotas for the next MACSE auction with non-awarded capacity from the 2025 round. Non-awarded capacity alone already more than doubles the 16 GWh maximum quota. In the South & Calabria zone, where the maximum upper bound will be 11.5 GWh, competition is set to be intense. This figure does not yet capture new projects authorised ahead of the auction registration deadline, so it likely understates the supply overhang.

Chart 1: Zonal MACSE quotas vs. non-awarded capacity from 2025 auction

Source: Timera Energy, Terna, ARERA

The final MACSE quota will be reduced by capacity awarded through the CM 2028 auction in MACSE-eligible zones: this constitutes a direct mechanical linkage between the two mechanisms.

For Southern projects, this creates a strategic fork. MACSE offers a dedicated storage contract, but at the cost of high competition and binary auction risk. The Capacity Market can be stacked with a tolling agreement, offering a more flexible commercial structure with lower auction risk exposure — though navigating it brings its own complexities, as discussed below.

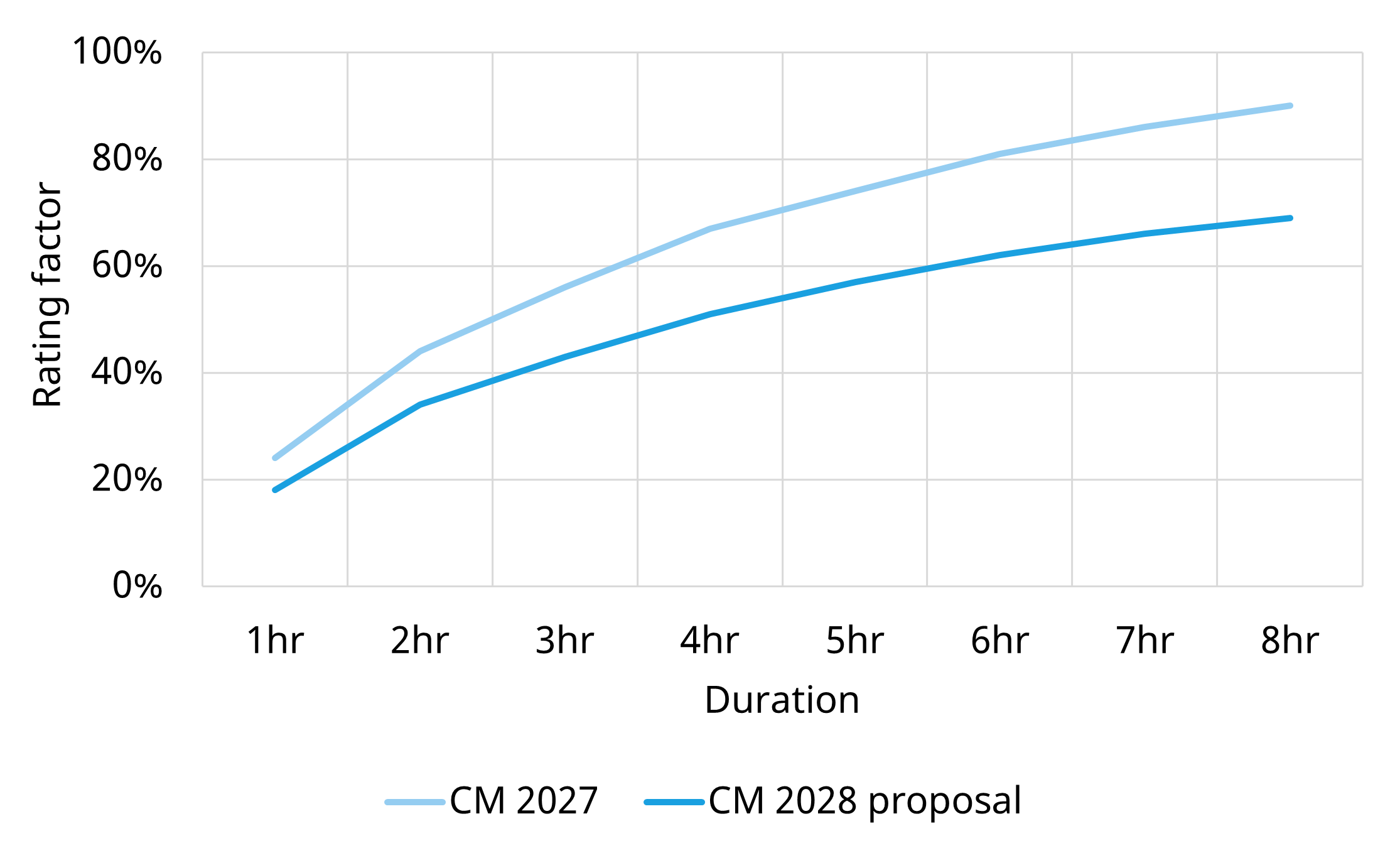

CM derating is a two-tier problem for new BESS

Terna’s February 2026 consultation proposes a significant downward revision to derating factors for the CM 2028 auction as discussed in our previous article. As BESS penetration increases, the incremental adequacy contribution of new storage declines. The proposed revision would reduce effective derating factors for new BESS by approximately 24%, directly compressing capacity revenues at any given clearing price (as shown in Chart 2).

Crucially, the consultation proposes to preserve higher derating factors for the ~10 GWh already contracted via MACSE 2028 – creating an asymmetric treatment between existing and new capacity within the same auction. If confirmed, this would add a material headwind for Southern projects considering the CM route and could channel more competition back into MACSE.

On the other hand, solar will be considered with lower derating factors too, reducing RES pressure on the CM.

CM 2028: what the missing parameters mean

The CM 2028 auction has completed consultation, but zonal demand curves and interconnector capacity assumptions remain unpublished – the two inputs that will ultimately define market space and competitive dynamics by zone.

The data centre pipeline is heavily concentrated in the North. If this demand uplift is reflected in the North’s demand curve, it could substantially increase headroom for Northern capacity while offering a limited relief to Southern participants dependent on final interconnector constraints. Until these parameters are confirmed, quantifying CM participation value across zones remains subject to material uncertainty.

CM will happen ahead of MACSE, therefore CM participation can anyway represent a risk hedging opportunity for Southern BESS projects from the high competition risk that MACSE will inevitably carry.

5 key BESS investor takeaways

Let’s finish with some key takeaways for investors:

- Terna’s de-escalating storage targets mean the next 2 MACSE auctions will be smaller than previous 2024 expectations, with structural competition locked in from the outset.

- Non-awarded MACSE 2028 pipeline already far exceeds MACSE 2029 maximum quota before new authorisations are counted.

- The proposed derating revision – if confirmed – penalises new BESS relative to already-contracted MACSE volumes, adding a headwind for Southern BESS participation to CM.

- This derating approach may impact market space in the North too based on the interconnector constraints defined in the auction.

- The data centre-driven demand uplift is asymmetrically concentrated in the North, which could contain CM opportunities for Southern projects.

Auction risk remains the central commercial variable for investors for both CM and MACSE paths.

How Timera can help

We recently published our Q1 2026 quarterly update of the Italian BESS Subscription Service, covering revenue stacking projections for all Italian bidding zones and grid nodes across all contract configurations – Merchant, MACSE and Capacity Market – together with market scenario analysis and baseload and RES-captured price projections. It is designed to underpin bankable investment cases for BESS and renewable projects across Italy.

For more information, contact Alessio Cunico (Associate Director) alessio.cunico@timera-energy.com or Steven Coppack (Power Director) steven.coppack@timera-energy.com.