“The BESS revenue stack is shifting from ancillaries to arbitrage”

Despite being one of Europe’s smaller power markets, Irelands Single Electricity Market (SEM) has attracted significant investor interest in battery storage. In today’s article we dig into how strong demand growth and regulatory reforms are underpinning BESS scaling. We also set out some of the risks and challenges investors face.

Strong demand growth driving flex requirement

Ireland’s power market has experienced an unusually turbulent few years, shaped by a combination of the wider European energy crisis and dynamics specific to the island itself.

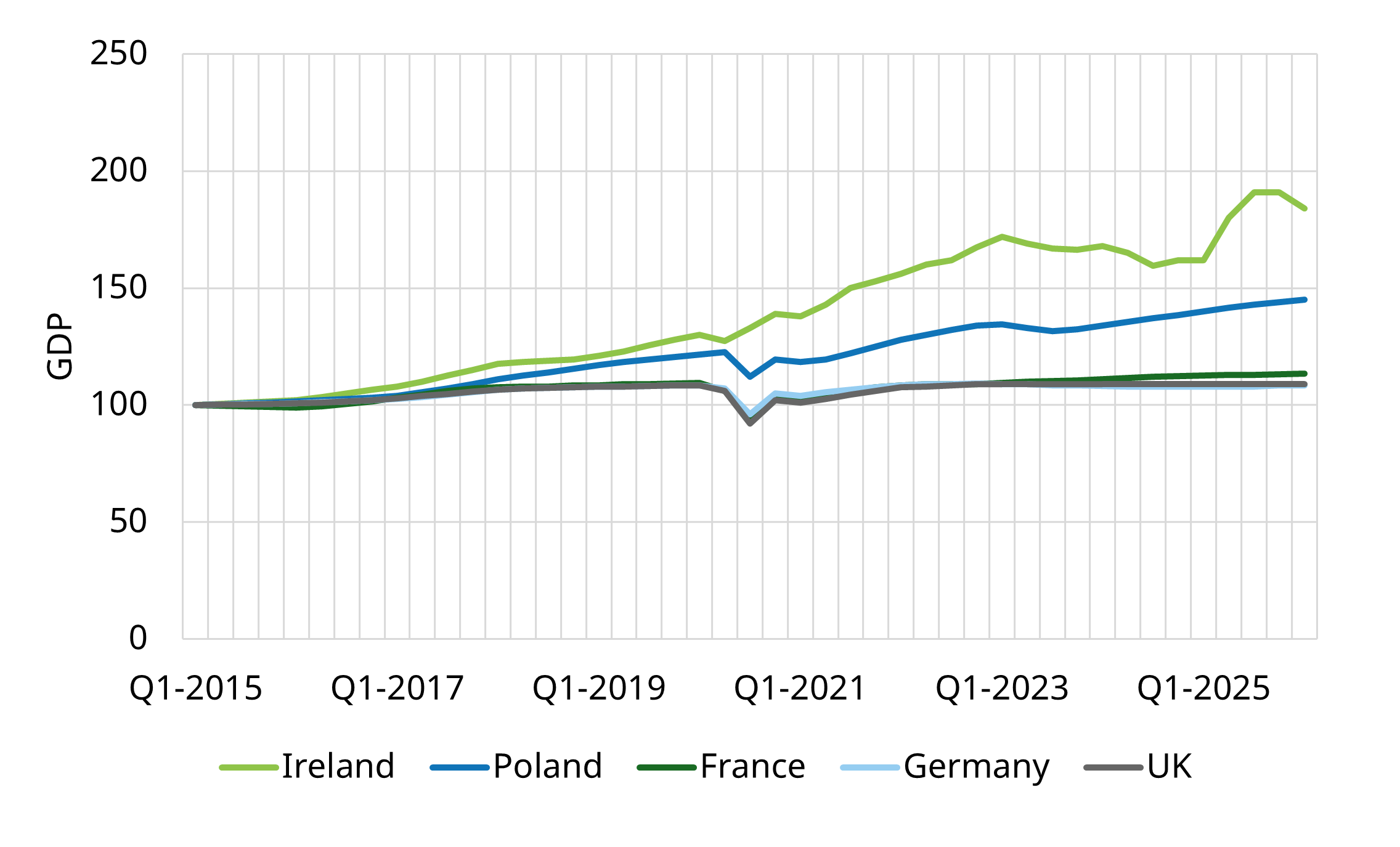

Unlike most of its European neighbours, Ireland has delivered exceptional economic growth in recent years as shown in Chart 1. This has been underpinned by global corporations establishing their European operations there, attracted by the country’s low corporation tax regime.

Google, Meta and a wave of AI hyperscalers have made Ireland, and Dublin in particular, a focal point for data centre investment, to the point where the sector now accounts for around 22% of total national power demand. For context, that figure stands at roughly 5% in the US and 4% in the UK.

The consequence has been a rapid acceleration in electricity demand at a time when supply-side infrastructure was struggling to keep pace. Ireland faces particular challenges in deploying new generation capacity, with planning constraints acting as a persistent and difficult barrier.

Market & policy response to demand growth

The combination of surging demand and constrained build-out pushed system adequacy to critical levels, with Loss of Load Expectation (LOLE) breaching 50 hours in certain years and forcing the state to procure emergency generation to maintain security of supply.

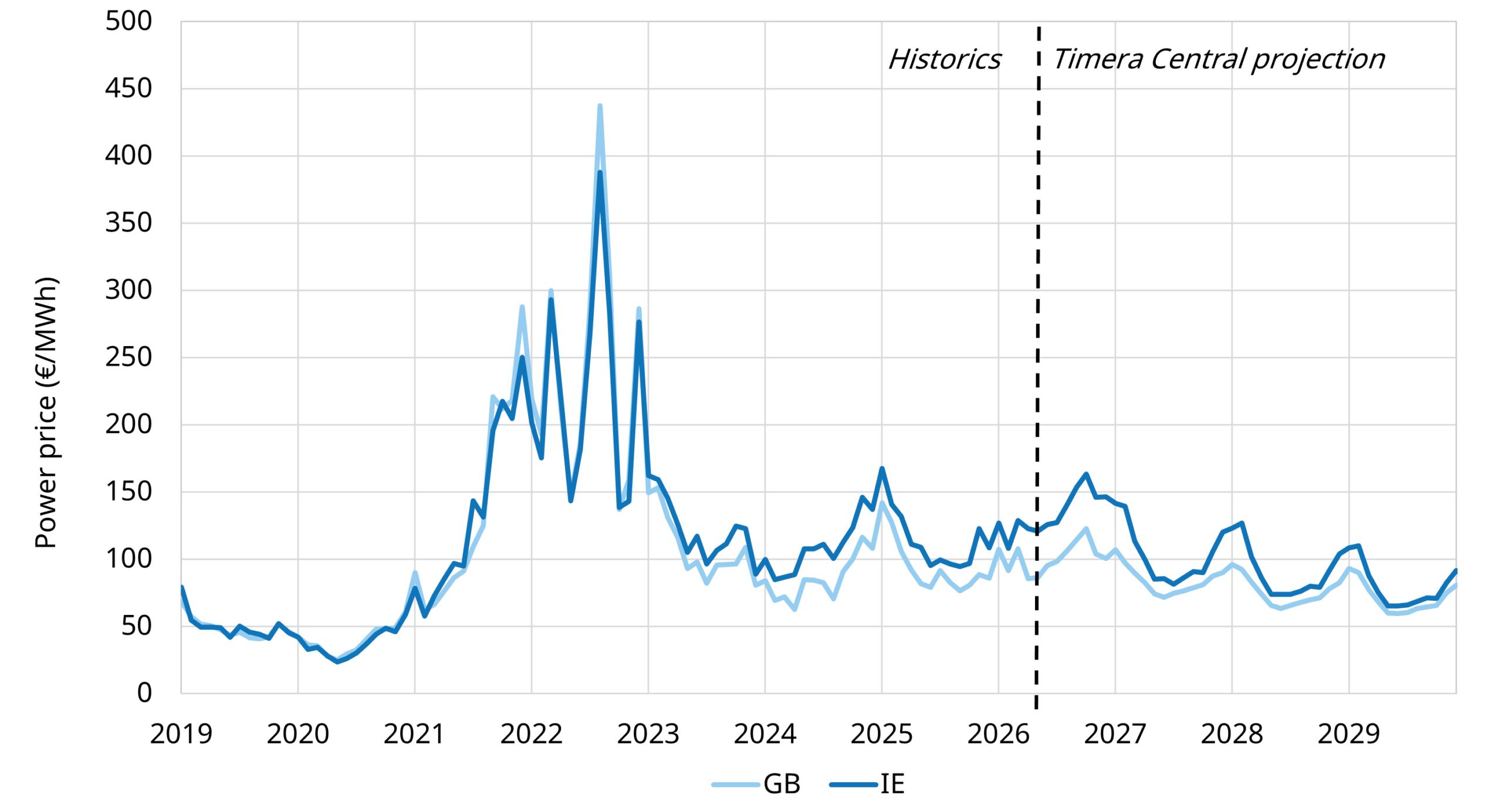

Wholesale power prices reflected the same underlying tightness. Having historically traded in close alignment with Great Britain, Irish prices progressively decoupled and sustained a significant premium over extended periods, due to system stress, as shown in Chart 2.

Chart 2: GB vs IE Day-Ahead power prices

Source: Timera, EPEX, SEMOpx

The policy response has been broad-based. A moratorium on new data centre connections in the Dublin region provided some near-term relief on the demand side, while the Planning and Development Act 2024 introduced meaningful reforms to address what had become one of the most persistent concerns for investors in the market.

On the supply side, a combination of capacity market reforms, new renewable support schemes and expanding interconnection capacity are beginning to rebalance the equation. While structural tightness persists through the transition, the elevated price volatility this creates continues to present attractive opportunities for flexible asset investors able to capture value at the front end of the curve.

Against this backdrop, there is a strong investment opportunity for flexible assets in the Irish market. In this article we focus on the BESS investment case, setting out the key revenue drivers, market design considerations and outlook for returns. In future articles will examine the RES investment case and the impact of interconnectors on the market.

What drove initial BESS build wave?

Two revenue streams underpinned the early wave of Irish BESS investment:

- DS3 Ancillary Services: The DS3 regulated tariff framework offered static payments for a range of system services, with multipliers of up to 4.7x during periods of high non-synchronous renewable penetration. Crucially, there was no forward commitment requirement, giving operators flexibility to switch in and out of services as conditions changed.

- Capacity Market (CM): Strong clearing prices for new-build BESS, reaching up to £150/kW/yr, combined with favourable de-rating factors, allowed assets to secure attractive 10-year contracted revenues. This provided a reliable contracted floor that supported debt financing.

These dynamics drove deployment of predominantly shorter-duration assets (0.5 to 1 hour), well-suited to the frequency response and DS3 services on offer.

5 challenges facing BESS investors

Despite the favourable revenue environment, several structural constraints limited the full potential of Irish BESS:

1. Wholesale market access was restricted until November 2025, when regulatory changes finally permitted BESS to submit negative Final Physical Notifications (FPNs) and receive negative dispatch instructions. Prior to this, participation in wholesale arbitrage was challenging.

2. Intraday liquidity beyond the IDA1 auction has been limited, constraining the ability of operators to re-optimise positions closer to real time or capture additional value via churn like in more liquid markets like DE.

3. Ancillary revenues are facing a structural shift. The DS3 budget of €235 million was exceeded for multiple years, driven primarily by spending on frequency response services, triggering a reform process (Future Arrangement for System Services, FASS). This has introduced uncertainty around future ancillary service revenues as procurement will shift to competitive day ahead auctions.

4. Planning remains a key development risk, with some projects facing prolonged delays or outright refusal, adding uncertainty to project timelines and costs.

5. Co-location remained challenging with e.g. MEC sharing historically not allowed and regulatory uncertainty around treatment of hybrid assets.

Market reform and BESS investment case impact

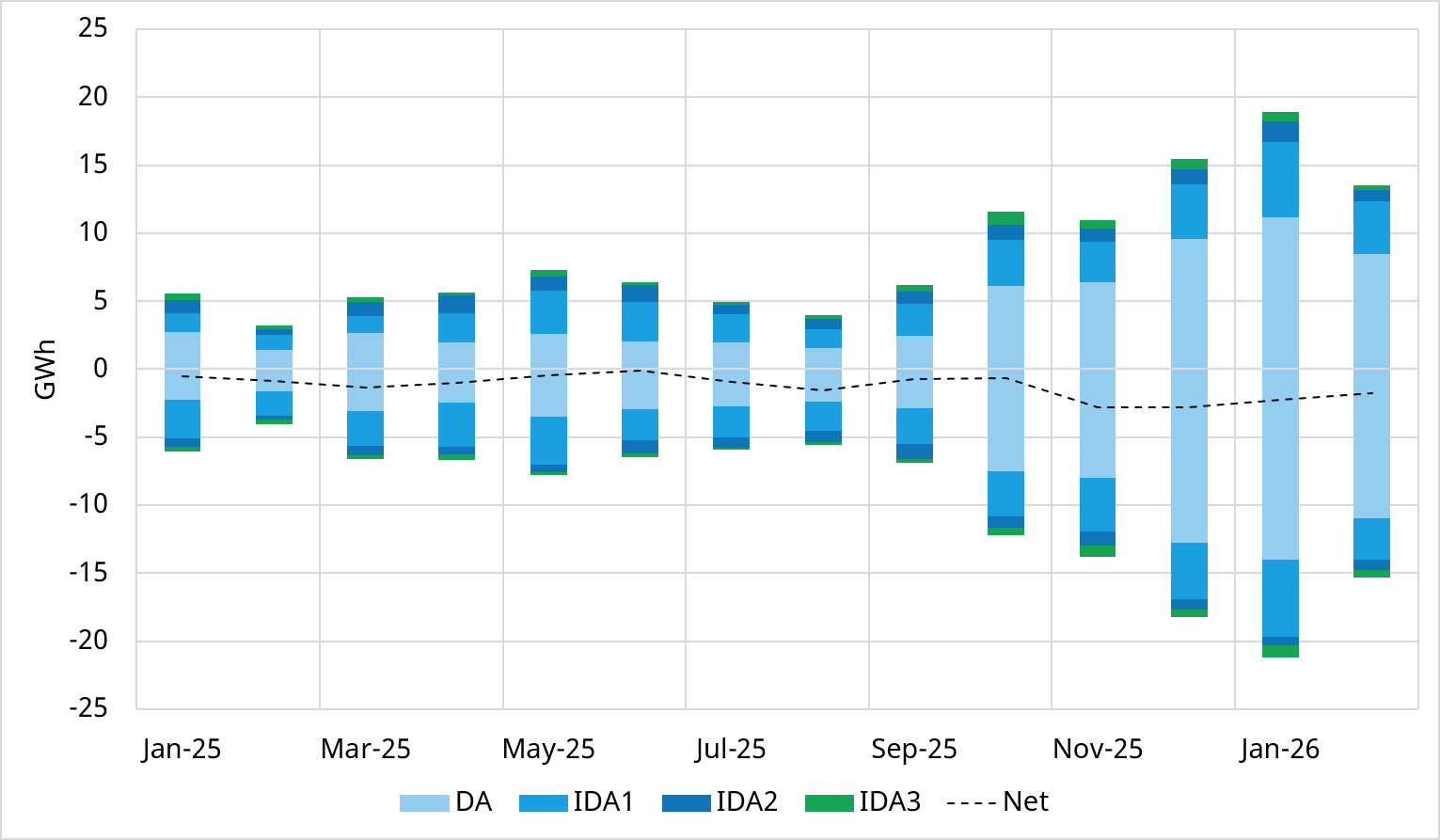

The most significant recent development for Irish BESS is the rollout of Scheduling and Dispatch 2 (SD2), which has opened wholesale market participation to storage assets via negative FPNs and dispatch instructions. The impact has been immediate as shown in Chart 3: traded volumes for Irish BESS increased approximately fourfold following implementation.

IDA means Intraday auctions, there a multiple across the day in the SEM some of which are coupled with the GB power market. IDA1 occurs first and IDA3 last.

Further reforms under the Enhanced Storage programme will bring BESS into the scheduling and economic dispatch algorithms, improving the commercial case for wholesale arbitrage and allowing assets to be dispatched more efficiently within the system.

On ancillary services, the direction of travel mirrors what has been observed in other markets with a shift from long term contracted revenues to more efficient and competitive auctions.

DS3 is transitioning towards competitive day-ahead auctions under the Future Arrangement of System Services (FASS). As has been the case in Great Britain, competitive procurement tends to compress ancillary service revenues over time as the market matures and new capacity enters.

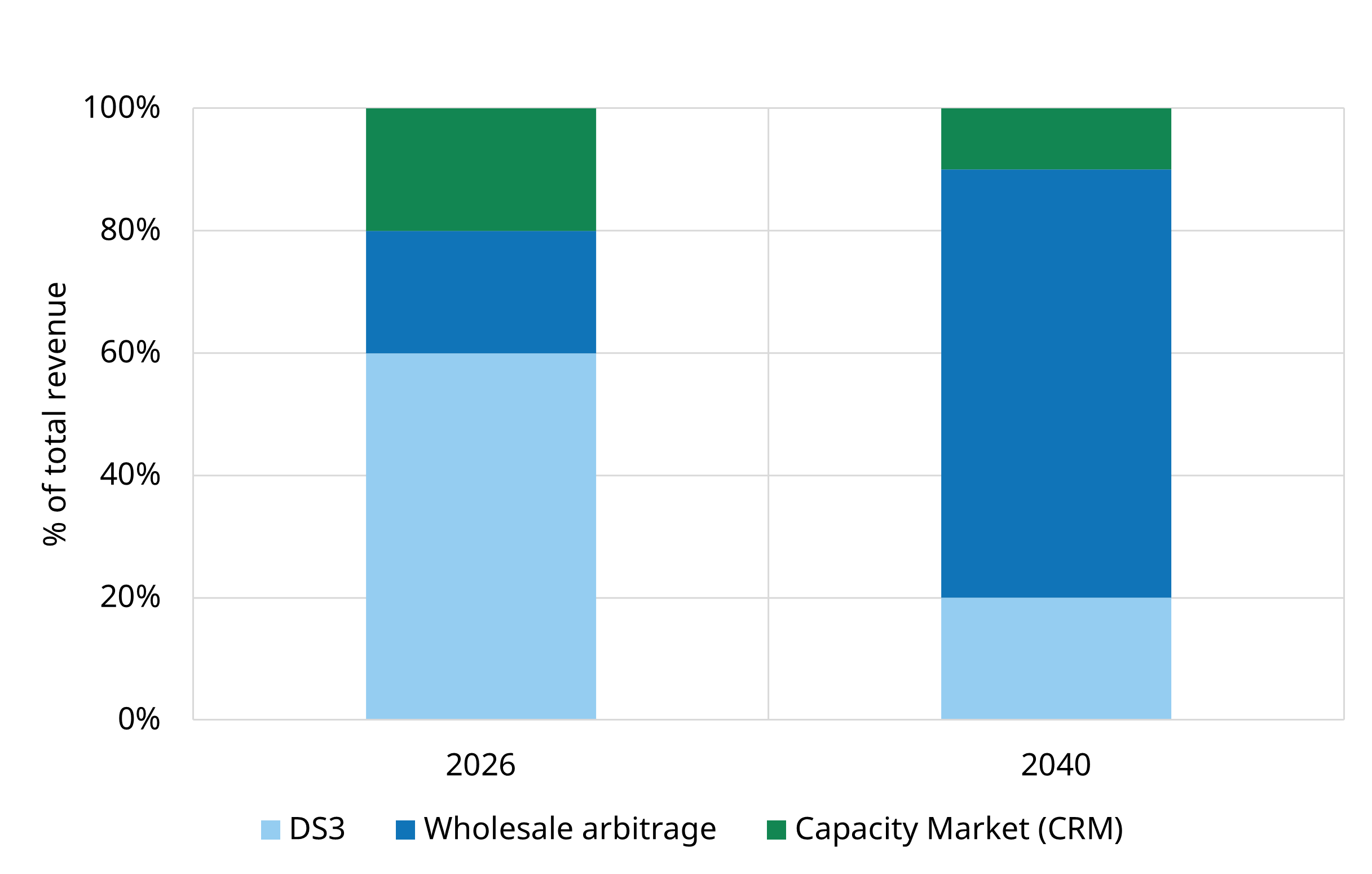

The implication for Irish BESS is that revenue will increasingly migrate towards wholesale arbitrage as shown in Chart 4. This is a shift that offers upside but also introduces greater cash flow variability and demands more sophisticated trading, revenue forecasting and route-to-market arrangements.

Chart 4: Illustration of BESS revenue stack 2026 vs 2040

Source: Timera stochastic BESS asset valuation model

This evolution is important for investors and lenders to price correctly. In a market where the offtake regime is less mature than GB, securing long-term revenue contracts or robust merchant arrangements will be a key differentiator for project bankability.

For battery storage investors, the ongoing shift from an ancillary tariff-driven revenue environment towards one increasingly underpinned by arbitrage introduces greater uncertainty into the business case.

Stochastic modelling of BESS revenue stack distributions enables investors and lenders to understand:

- Risks – that often sit in the left hand tails of the revenue distribution

- Value capture – strongly influenced by the right hand tail of the revenue distribution

Quantification of these distributions underpins development of a robust BESS investment case.

There are also a number of other factors investors need to weigh up, such as the planned shift in network charges from demand-based DTUoS to generation-based GTUoS, the need for greater clarity around co-location regulation, and rising curtailment risk as RES capacity grows. We will explore some of these in future articles, but if you are actively looking at investment opportunities in Ireland, please get in touch with our team to discuss in more detail.

How Timera can help

Timera is active across the Irish market, having provided valuation and commercial due diligence support for acquisitions including Greenlink and Energia as well as multiple BESS projects. We bring deep commercial and analytical expertise across flexible assets in Ireland, from revenue modelling and market access strategy through to transaction support and ongoing asset management advisory.

Get in touch with Arshpreet Dhatt (Principal) arshpreet.dhatt@timera-energy.com to discuss how we can support you.