“Is monetisation strategy following value?”

The 2025/26 European gas storage year, which closed at the end of March, underscored a familiar paradox: despite the indispensable role storage plays in flexibility and security of supply, it remains a structurally difficult market for both operators and capacity buyers.

The 2025–26 gas year was a stress test for the European storage value model. The results point to a structural shift in how storage assets earn their margin.

A turbulent season

European gas storage went into the 2025–26 injection season with inventories below the five-year average. Prices were elevated, and several governments – e.g. Italy and Germany – put subsidy mechanisms in place to incentivise injections.

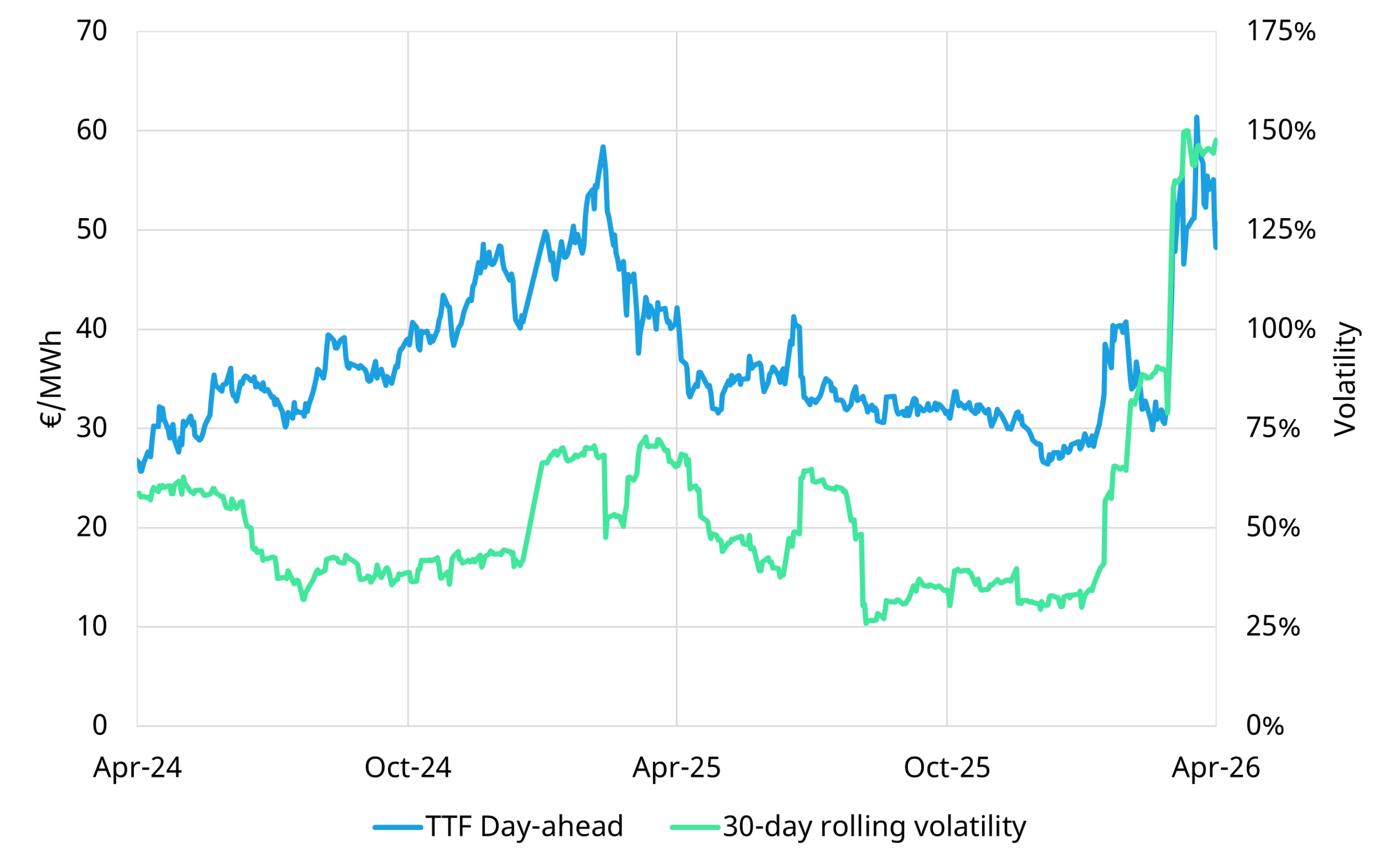

The gas market however delivered some surprises as shown in Chart 1.

Chart 1: TTF front-month prices and 30-day rolling volatility

Source: Timera Energy, ICE

The 2025-26 storage year got off to a difficult start in Q4 2024 for storage operators. A sharp rally in TTF prices drove strong backwardation in the forward curve. By October 2024, summer-winter spreads had moved out of the money and remained there through to April 2025, creating a challenging backdrop for storage operators selling capacity via auctions.

With backwardation implying zero intrinsic value for the coming storage season, capacity prices for 2025-26 cleared at very low levels: operators were selling capacity into a tough market with buyers heavily discounting extrinsic value and some auctions failing to clear.

As the 2025 storage season got underway in April, seasonal spreads normalised. A sustained wave of LNG arrivals into Europe kept prices on a slow downward drift throughout the injection period, with volatility remaining largely compressed vs 2024 levels.

Price volatility was subdued for much of the year, limiting options for profitable re-optimisation of storage positions. It was only in the winter and into early 2026 that a larger opportunity emerged: a cold snap across Europe in February tightened balances, before the Middle East shock hit in March.

The Iran conflict and the resulting closure of the Strait of Hormuz sent global gas prices and volatility as shown in Chart 1. For many storage optimisers, a significant portion of season’s value was concentrated in those final winter months. However being close to the end of the storage year limited opportunities to extract value from crisis induced price volatility.

European injection demand was met by pulling in a record volume of LNG. Price volatility – not seasonal shape – became the dominant feature of the TTF curve. The flatness of seasonal spreads across 2025 alongside sharper volatility events has acted to shift the majority of value from intrinsic to extrinsic. The former is hedgeable on a forward basis, the latter is focused on re-optimisation of prompt positions to extract price volatility.

What the backtest shows

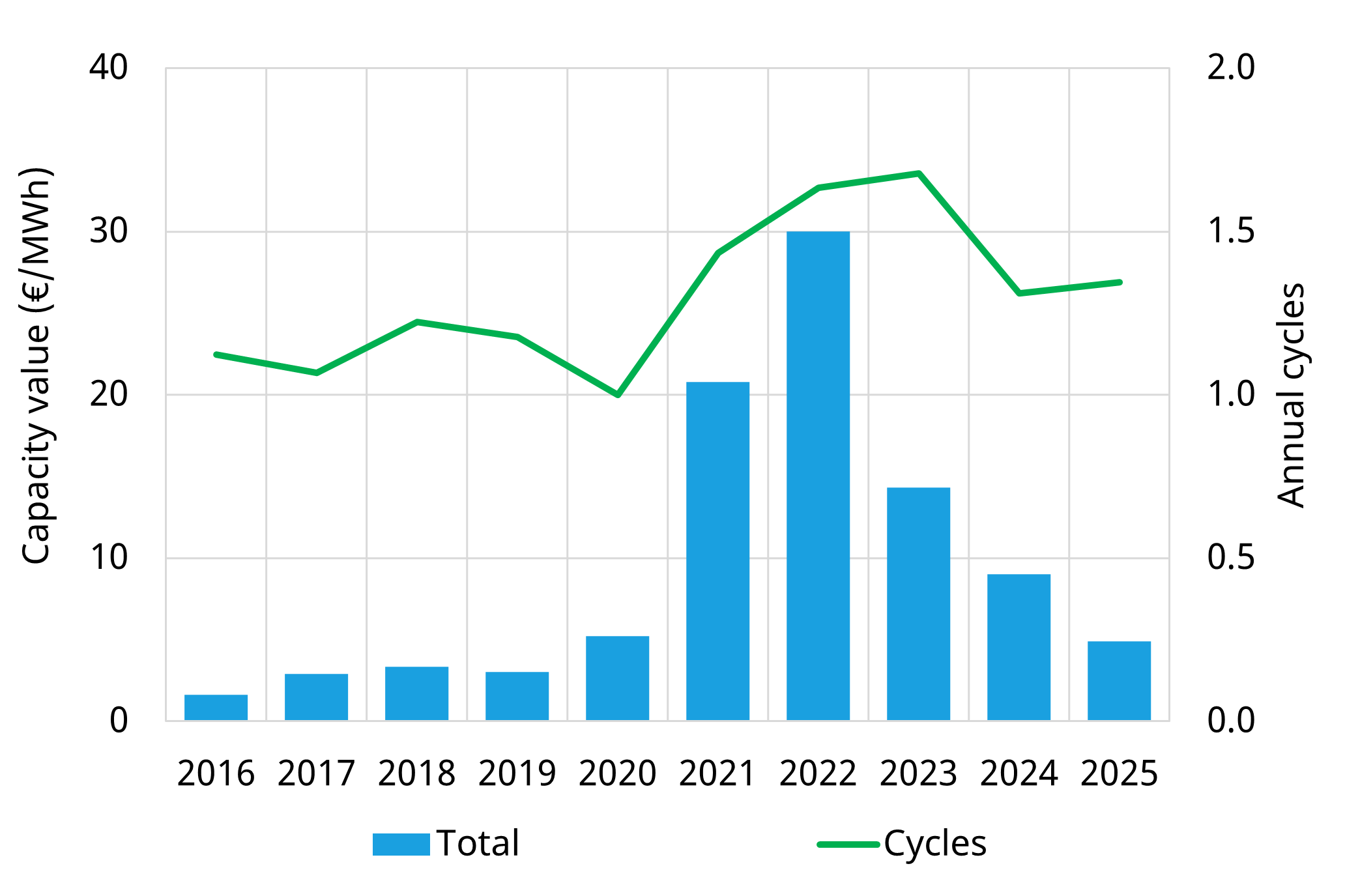

To illustrate the dynamics of storage value capture across the 2025-26 storage year, we ran a rolling intrinsic optimisation against Apr-25 to Mar-26 forward curves, using a standard 90/90 day cycle seasonal facility with TTF hub access, shown in Chart 2.

Chart 2: Backtested revenue capture across the gas storage year, April - March

Source: Timera Energy gas storage valuation model, ICE

Our backtested estimate of achievable margin across the 2026 was €4.90/MWh, which is a 45% reduction from the previous year. There was zero intrinsic value (measured at the start of January ahead of the storage year beginning in April 2025), so 100% of this value is from re-optimisation of the storage through-out the year in response to price volatility.

We do not expect a structural recovery in storage margins across the next few years, as large volumes of LNG supply growth are likely to weigh on volatility. Growing LNG supply is also eroding intrinsic value for storage facilities by providing additional seasonal flexibility to Europe, and reducing the demand for gas storage contracts.

There are, however, factors which are driving greater volatility in European onshore gas prices. Growing intermittency in the power sector from the buildout of renewables, with the backdrop of overall increasing electrification will act to increase variability for gas-fired-power demand, on time frames which only short-term flexible gas supply such as storage can meet.

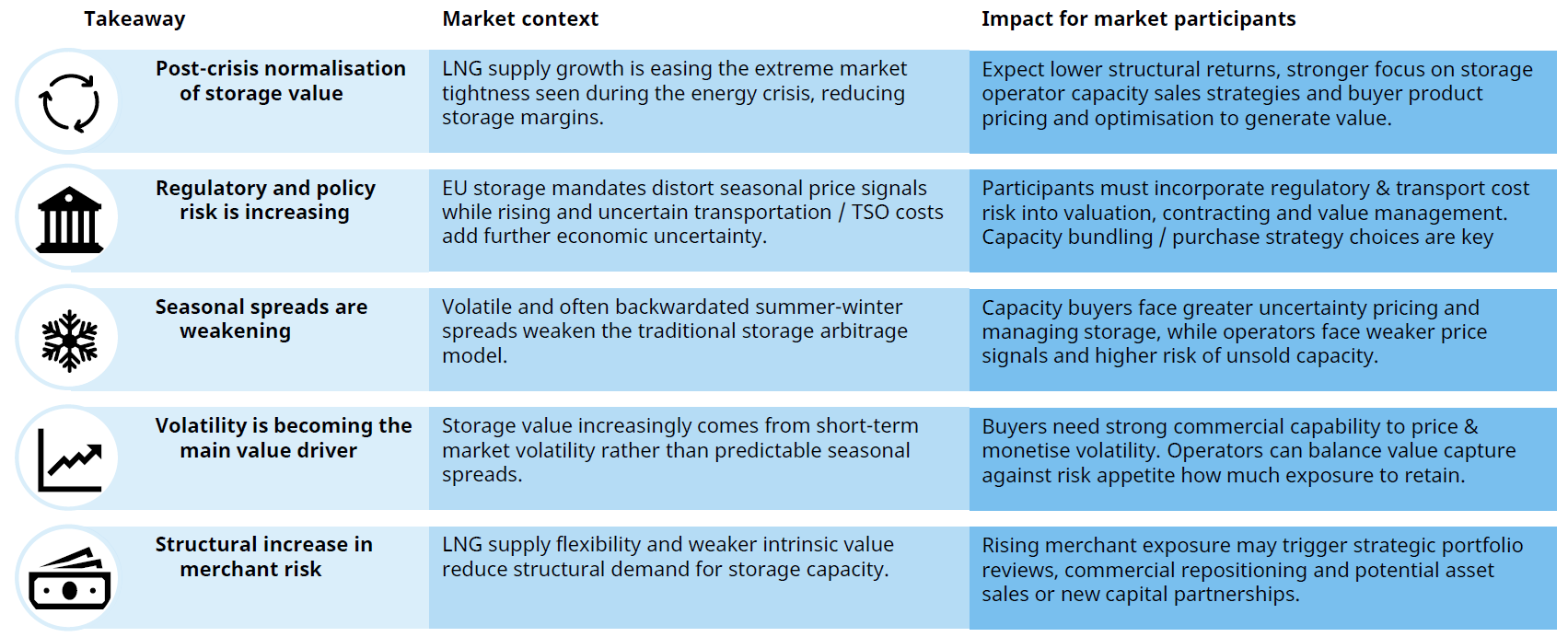

5 key takeaways for storage owners and investors

Storage remains critical midstream flex infrastructure for European security of supply. But valuation and monetisation strategies need to reflect the structural shift in value from capturing seasonal spreads to harvesting price volatility. In Table 1 we summarise 5 key takeaways for owners & investors against the current market backdrop:

Three practical implications stand out across the table:

- Valuation methodologies need to capture extrinsic value properly. Simple spread based intrinsic valuation increasingly understates a facility’s economic value and risks anchoring transactions and investment decisions on the wrong number.

- Operational capability becomes a sharper differentiator. Cycling speed, multi-cycle optionality and hub connectivity directly determine how much extrinsic value an asset can actually monetise.

- Commercial strategy needs to reflect the new value mix. Capacity sales strategy, contracting structures and hedging approaches need to reflect the shift in underlying asset value from intrinsic to extrinsic.

Get these right and significant value opportunities remain across the European gas storage asset base.

Timera Energy advises gas storage investors, operators, and traders on asset valuation, commercial strategy and market risk. If you have any questions regarding our gas storage outlook, or would like more information, feel free to reach out to Arthur Finch (Analyst, Gas & Power) at arthur.finch@timera-energy.com.