Germany is one of Europe’s most active power markets for BESS investment. Over 3 GW of grid-scale storage is expected to be operational by the end of 2026. Our analysis sees capacity growing past 12 GW by 2030, despite major connection access challenges currently facing developers.

BESS growth is being driven by strong structural fundamentals: rapid wind and solar penetration, retiring thermal plants and demand growth are widening day-ahead price spreads and pushing intraday volatility higher.

German BESS returns are currently strong, but the regulatory structure underpinning them is now facing some major reforms. Grid fees, connection terms and redispatch obligations are all being targeted.

These reforms are presenting a key challenge for our German BESS investor client base – how to price the impact of regulatory reform into live investment cases, and how to distinguish projects that can absorb the changes from those that won’t.

Grid fee reform is the biggest single risk – impact depends on configuration

The headline reform is the network regulator, BNetzA’s, overhaul of the grid fee regime that currently applies to battery storage. Today’s baseline is a 20-year full exemption for assets commissioned before August 2029 – an exemption that every German BESS investment case has taken as given.

BNetzA’s AgNeS process proposes to replace this from 2029 with a three-part fee structure:

1. A capacity charge (Leistungspreis, €/kW), payable on booked grid capacity regardless of dispatch.

2. A variable working charge (Arbeitspreis, €/kWh) potentially on either total or net grid energy consumption

3. A dynamic working charge or payment (dynamischer Arbeitspreis, €/kWh) that varies by location and time, and can turn negative where storage provides grid relief.

The biggest source of investor and financing uncertainty today is retroactivity. BNetzA has signalled it may end grid fee exemptions early – potentially including assets already built or under construction – which would directly impact economics of existing projects.

Final parameters may not be fixed until late 2028, past FID for many 2028–29 COD projects. Lenders are reluctant to lend against risks they cannot yet quantify. The scale of the value impact varies significantly by project configuration: duration, cycling pattern and location are all value drivers.

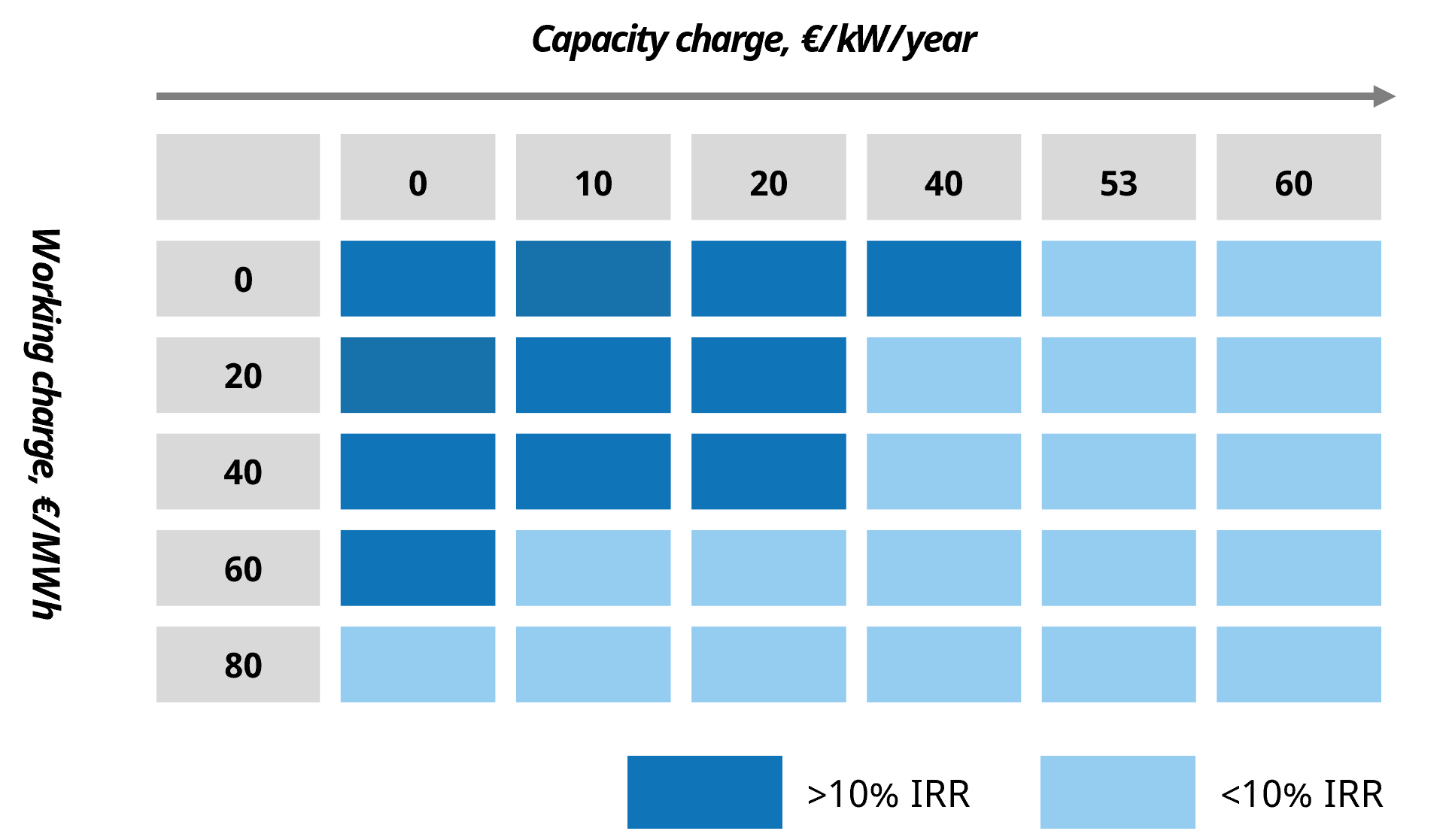

Chart 1 shows a heat map of post-grid-fee IRR across fixed capacity and variable working charge (Leistungspreis × Arbeitspreis) combinations, for 4hr BESS assets. Dark blue cells show where projects clear a 10% unlevered IRR hurdle; light blue cells show where they don’t.

Chart 1: Grid fee combinations that support a 10% unlevered IRR hurdle rate (4hr BESS)

Source: Timera; based on BKZ of €120k/MW overcoming 10% 20-yr IRR hurdle rate, based on 2030 Commercial Operation Date

Takeaways:

- BESS investment economics are impacted quickly by even modest capacity & variable fee charges

- Capacity charges erode IRR faster per unit than working charges, because they are payable regardless of dispatch and offer no natural hedge.

- Longer BESS durations are more resilient to the introduction of grid charges (e.g. 4 hr duration economics fairs better than 2 hr given CAPEX declines).

In summary grid fees are a big deal – they do not destroy the German BESS investment case, but robust quantification of their impact on project configuration and location has become important.

Flexible Connection Agreements trade speed for revenue

Given the scale of the German BESS connection queue (more than 700 GW), Flexible Connection Agreements (FCAs) are transitioning from exception to default for bringing new BESS capacity online.

The trade off is faster grid access in exchange for accepting one or more of:

- Import and export caps on grid flows.

- Ramp-rate limits on how quickly the asset can change output.

- Ancillary service restrictions.

- Trading schedule freezes.

Not all of these constraints bite equally. Export caps can be particularly damaging because they can hit high value intraday opportunities. Ramp-rate limits compress fast-response ancillary revenues, particularly where pre-qualification thresholds for FCR require full activation in tight timeframes.

FCAs are also project-specific and vary by grid operator, which means generalised impact figures hide wide dispersion across locations.

A further distinction matters commercially: static constraints can be priced into tolls, while dynamic constraints involving real-time curtailment are much harder to underwrite and can break standard tolling structures.

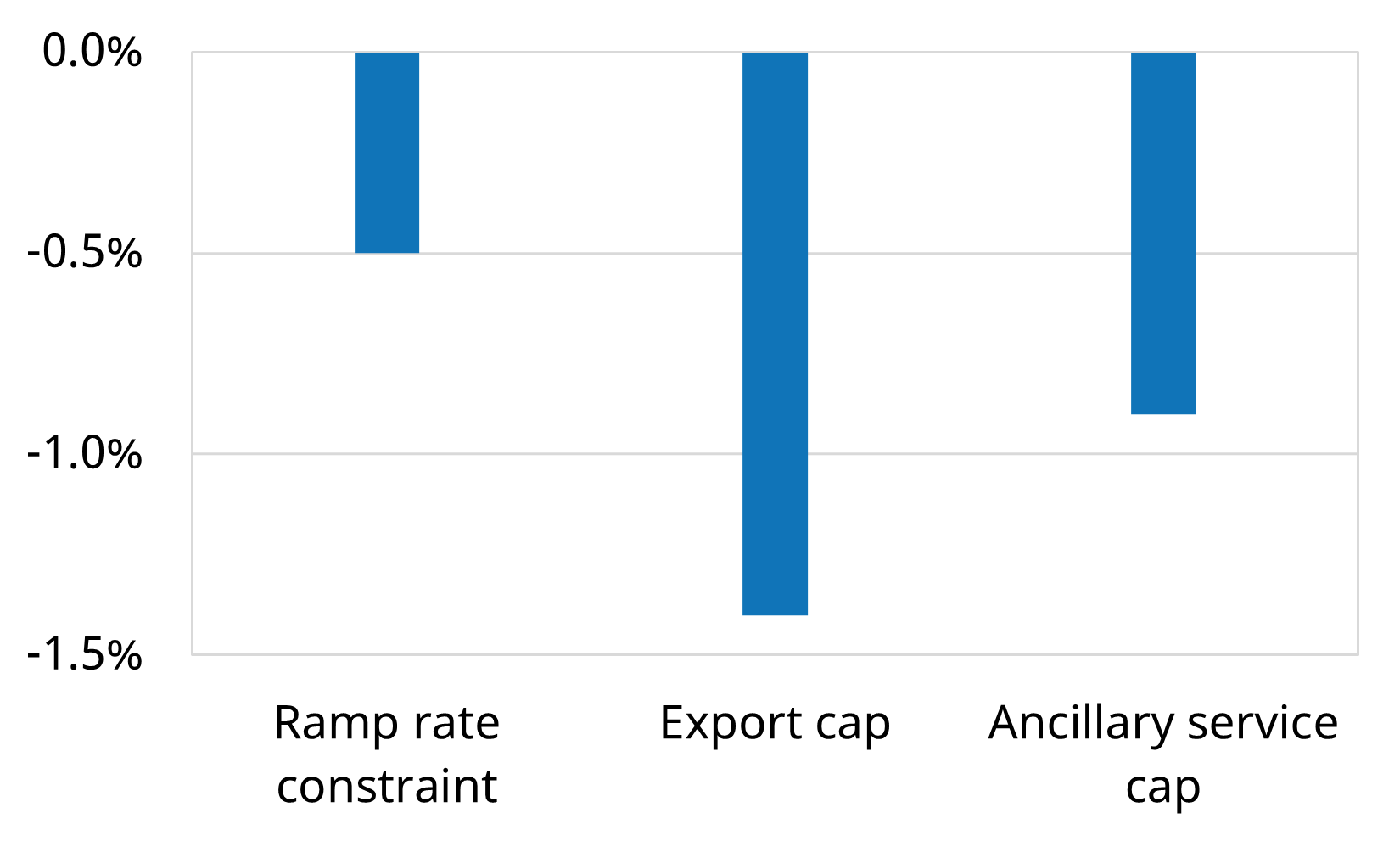

Chart 2 shows the indicative IRR impact of individual FCA constraint types on a reference 4hr BESS asset, expressed as differences versus an unconstrained baseline.

Chart 2: Indicative IRR impacts for 4hr BESS

Source: Timera; note: 2030 commercial operation date

In our illustrative case study, a static time-of-day export cap reduces IRR by roughly 1.4%; a ramping constraint of 10% by around 0.5%, and a 30% ancillary service participation cap by approximately 0.9%.

Individually these are manageable, but FCAs typically bundle multiple constraints, and the quantifying the cumulative effect is important for investment case definition.

Reform risk is cumulative but not additive

Grid fees and FCAs do not simply add together – they interact. FCAs constrain revenue capture, cutting upside during the hours when the asset is curtailed; grid fees impose a cost floor, with the Leistungspreis capacity fee payable regardless of operation.

Together they narrow BESS margin distributions from both ends. The three overlapping reforms are summarised in Diagram 1 below – taken together, they reshape the commercial architecture of the German BESS investment case more fundamentally than any one of them does in isolation.

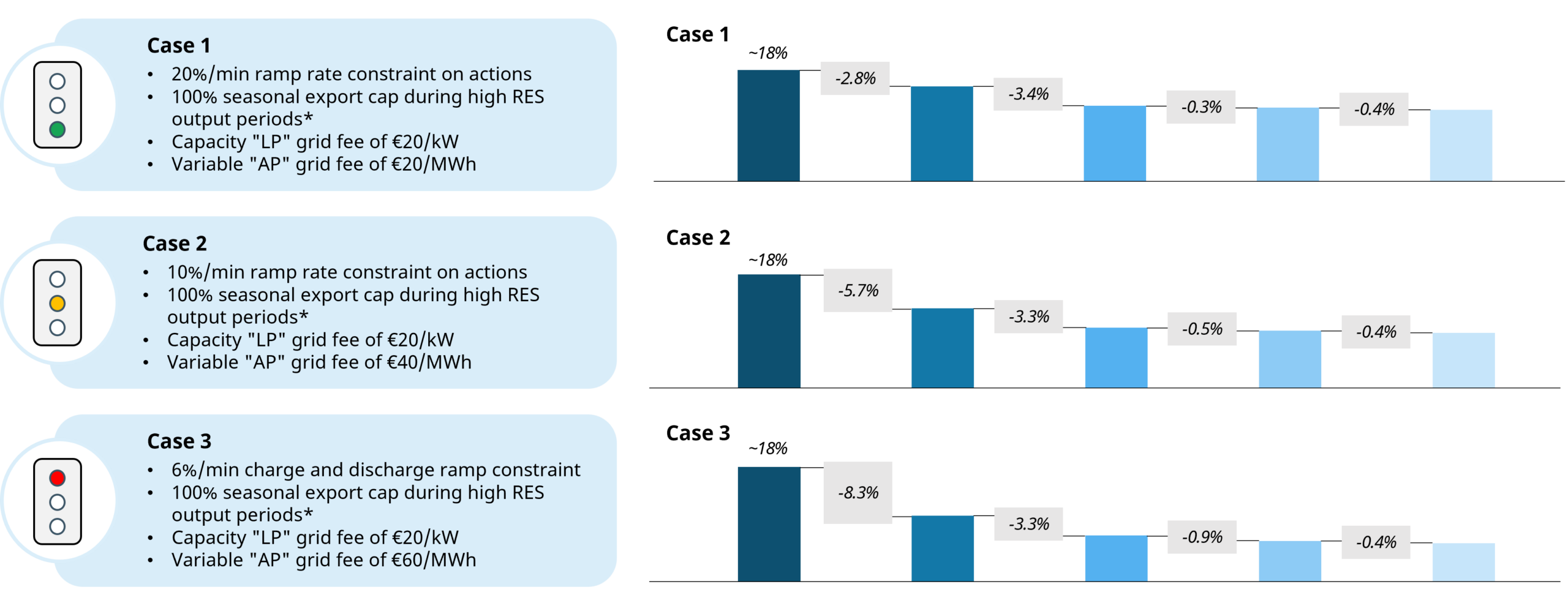

Chart 3 shows the incremental IRR impact for three different BESS cases, with varying grid fee and FCA conditions. A summary of the conditions applied to each case is also below.

Chart 3: Project IRR impact across three 4 hour BESS asset case studies

Source: Timera

Probabilistic analysis is key to quantifying these risks

Deterministic IRR analysis – still the dominant industry approach – materially understates the cumulative risk created by these reforms, because it ignores the correlations between wholesale price paths, curtailment incidence and dynamic grid fee signals. A stochastic BESS valuation framework with hundreds of simulated outcomes is required to capture a robust distribution of margin outcomes. The material risk sits in the left tail – low-price, high-curtailment, high-fee combinations – while the value sits in the right, in combinations that averaged cases similarly obscure.

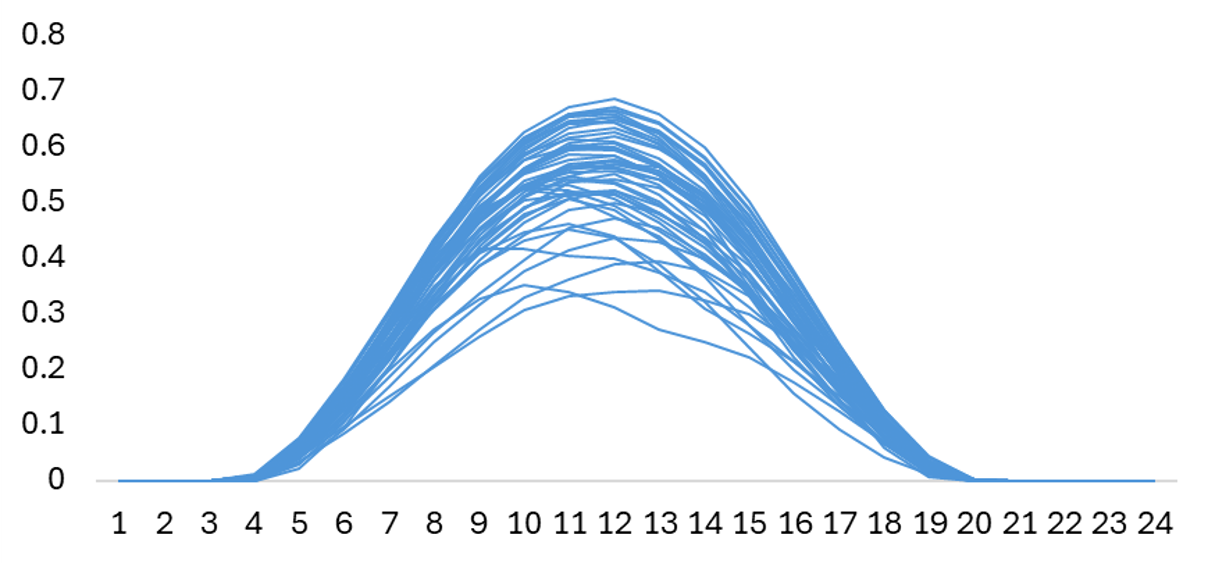

Chart 4 shows a fan of sampled solar load factor paths from the Timera power market model, illustrating the distributional nature of the inputs that drive price formation, curtailment incidence and ultimately BESS revenue.

Chart 4: Distribution of German summer solar load factor profiles (hourly)

Source: Timera

The chart is not about solar per se – solar is just one example of many input variables that drive the distribution of BESS revenue outcomes. A single deterministic run hides the dispersion of outcomes that reform risk interacts with; only sampling the full distribution reveals the combined impact of grid fees, FCAs and redispatch clearly.

5 key takeaways on reform impact on the German BESS investment case

The reforms point to five conclusions for German BESS investors:

1. Reforms create 2 major new risks that need to be priced: A potentially retroactive grid fee regime introduces fixed, variable & locational charges. FCAs constrain BESS flexibility, compressing both tails of margin distributions. Reform impacts flows straight through to project economics and need to be effectively quantified.

2. Reforms interact dynamically with BESS value capture: Simple rules of thumb do not work in quantifying reform value impact. Both grid fee and FCA reforms dynamically impact BESS margin capture & operation, with dependencies on project configuration & location. Impacts are not directly additive.

3. BESS offtake and financing bankability is directly impacted: Virtual tolling, capacity-tranched arrangements and reform-contingent pricing are becoming standard in order to secure offtake – understanding and transferring reform risk to parties better placed to carry it is important for enabling project bankability.

4. Quantifying reform risk requires a distributional view: BESS asset duration, location and offtake structure interact dynamically with grid fees and FCAs to drive value via shifts in the tails of BESS revenue stack distributions – magnifying downside, curtailing upside. Capturing this requires stochastic distribution analysis of how the reforms interact with BESS assets, not single-point IRR scenarios.

5. Reforms also present opportunities. The reforms are creating much greater locational value and risk differentiation across projects. Investors who can effectively quantify & filter projects for reform impacts have a competitive advantage.

Timera supports a range of investors navigating the impacts of multi-dimensional reform risk in Germany. For a discussion of our German BESS analytical framework or bespoke project-level analysis, contact Sam Kayne, Principal, at sam.kayne@timera-energy.com .