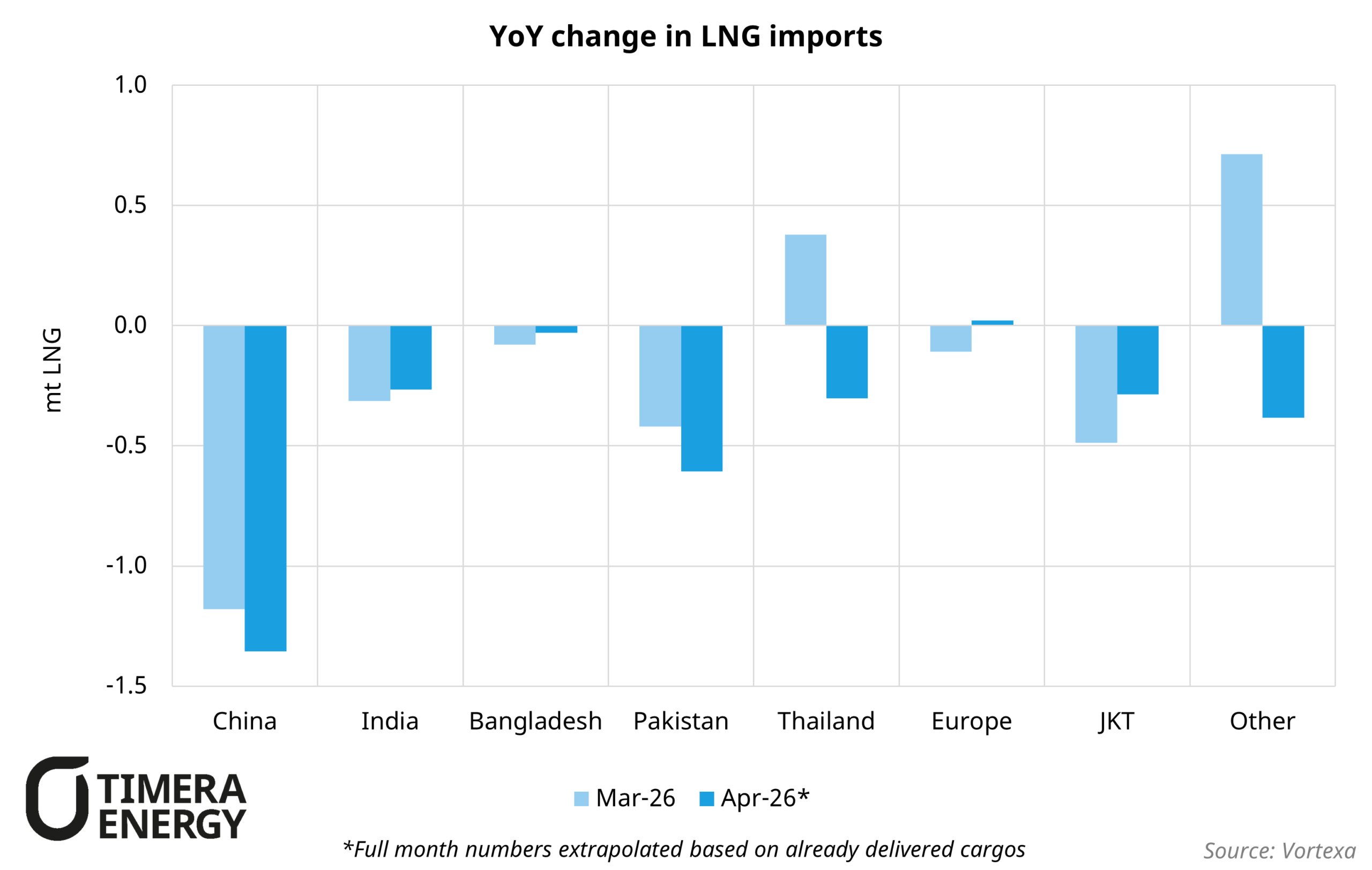

Early data suggest the burden of rebalancing the global LNG market during the current supply shock has fallen disproportionately on China. LNG arrivals into the world’s second-largest import market fell 23% year-on-year in March and are tracking around 28% lower in April, as summer JKM prices have surged from ~$10.7/mmbtu pre-crisis to $16.6/mmbtu on April 14th.

The drop stands out even against a broader Asian retrenchment with South Korea down 8% in March, India down 16% and Bangladesh down 11%. Chinese exposure to Qatari LNG exports is high at 25% of total LNG imports in 2025, pushing some buyers into the spot market, but relatively low compared to countries like India (~40%) or Bangladesh (~70%).

China’s LNG import-flex is enabled by its energy system. Coal power plants can substitute for gas plants relatively easily while competing oil-based fuels can replace gas across many industrial process heat applications. A March 2026 ban on oil product exports, extended into April, has kept competing fuel prices (i.e. diesel, fuel oil) lower vs international levels, reducing the incentive to pay for expensive spot LNG cargos. Significant storage capacity, on the order of 50-55 bcm (40 mt of LNG equivalent) also allows China to spread the impact of the crisis out across the year. The government has given some policy support to gas, with US LNG being imported after a one-year hiatus; but overall Chinese LNG demand has weakened as prices have risen.

By comparison, countries traditionally considered to be more price sensitive such as Bangladesh and India have seen smaller falls in imports as governments have stepped in to help secure spot replacements for lost cargos. Pakistan, with its massive exposure to Qatari LNG, has seen the starkest drop in imports so far, down more than 70% in March. Other major LNG markets have proven less responsive to high prices, though not immune. While European imports are flat year on year, pre-crisis expectations were that Europe would see a significant jump in imports over summer year on year to help refill depleted storages. As such, the flat signature is telling of a tighter European balance, with lower deliveries being offset by coal to gas switching in the power sector and a reduction in net injections over summer to date.