Europe left winter with storage levels just 28% full, near the bottom of the five-year range, and thus an above average injection rate will be critical to meet the EU’s mandated storage fill levels.

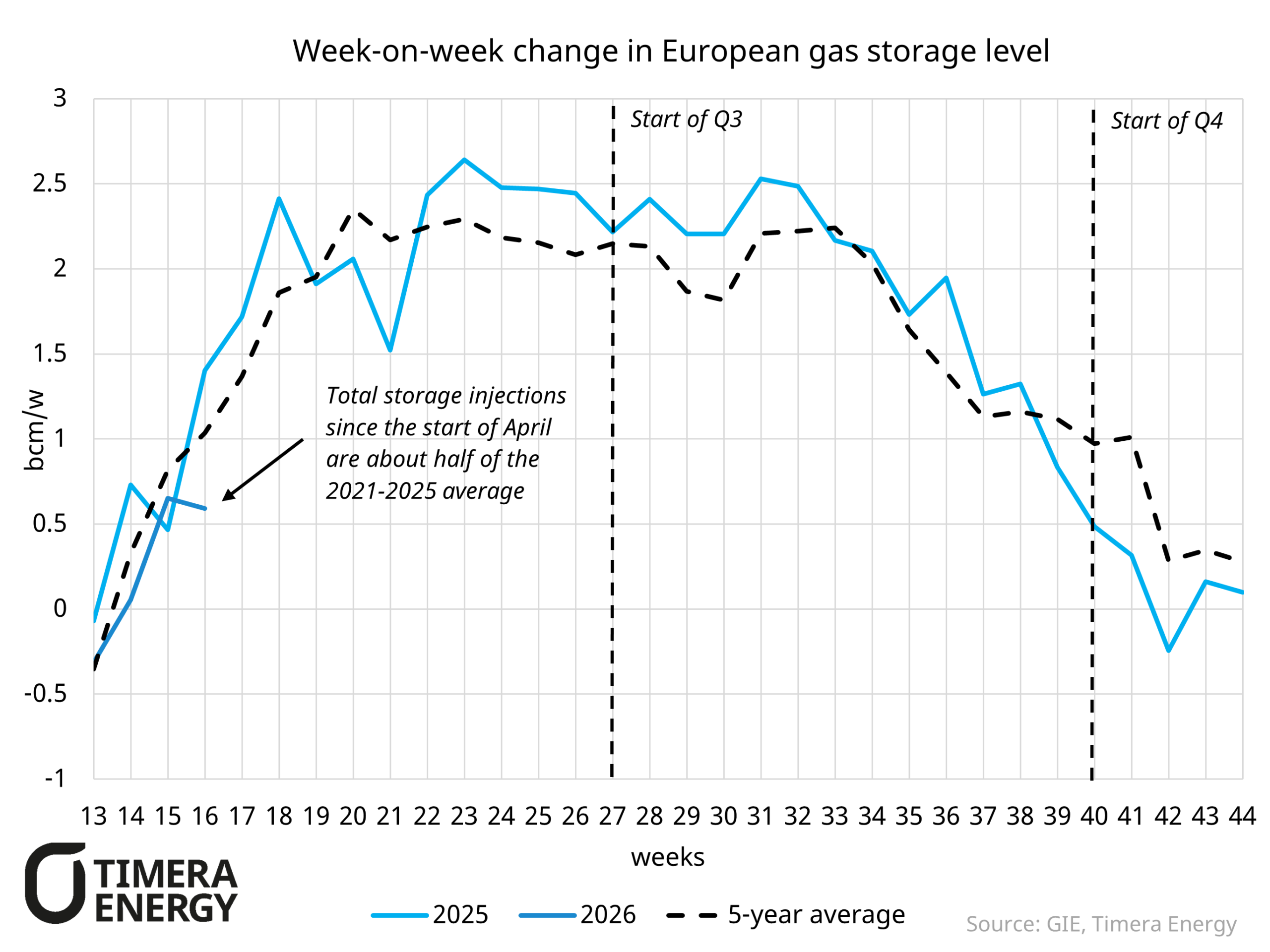

However, three weeks into injection season European gas storage injections are lagging both 2025 and the five-year average. The largest culprit is the ongoing disruption to LNG supply in the Middle East which has taken ~15% of global LNG supply off the market. Additionally, backwardated price curves, driven by expectations of a resolution to the Middle Eastern supply crisis, are reducing the economic incentive for storage capacity holders to inject.

The slow start to storage injections highlights the challenge ahead for Europe. Since the 2022 energy crisis, the EU Commission has mandated minimum storage fill levels ahead of the winter withdrawal season. This year’s target has already been relaxed to 80% between October 1st and December 1st, down from 90% last year. Existing policy would allow mandates to be brought down further to 75% if justified by “persistent unfavourable market conditions”. Germany’s national mandate sits even lower at roughly 70% in aggregate, reflecting reduced site-level targets at large facilities like Rehden whose slow injection rates qualify for exemptions on a technical basis under the EU rules.

Given low storage levels at the start of April, reaching even the relaxed 80% threshold would require injections roughly in line with last summer. For now, a subdued European injection rate is helping to balance the global market at a lower price point. But if Europe is to hit mandates, the pace of injections will need to increase. Without a rapid resolution to the crisis in the Middle East, sourcing sufficient LNG for injections will likely require European buyers bidding up prices aggressively to displace Asian LNG demand.