European gas inventories have got off to a sluggish start to the 2026 injection season, currently sitting around 7.2 bcm (17%) below last year’s level. The culprit is a TTF forward curve that has been pushed into backwardation by ongoing Middle Eastern supply disruption, removing the economic incentive to inject at pace. With near-term prices elevated relative to winter delivery, storage economics don’t stack up, and the market is thus under filling at present against the rate required to meet the European Commission’s 80% mandate.

Even if Middle Eastern flows were to resume tomorrow, a quick fix looks unlikely. Reports point to a multi-month staged return to full loadings, meaning summer is set to remain constrained. Meanwhile greater volumes of new Atlantic LNG supply capacity will be online by winter, potentially coinciding with the full resumption in Middle Eastern volumes. As a result, the curve is likely to remain backwardated and Europe may enter winter with gas in store below the EU’s mandate.

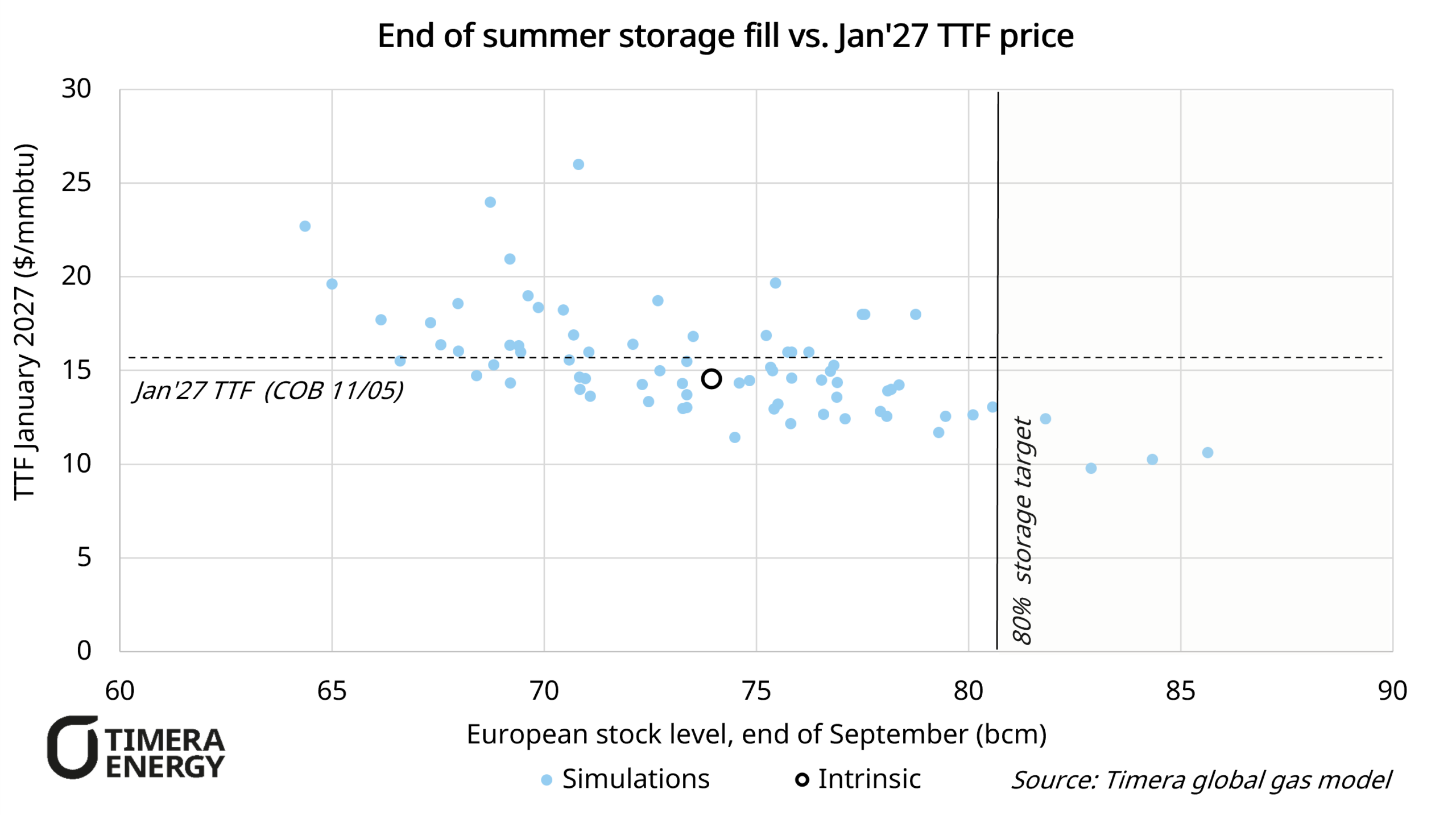

What would this mean for winter price risk? The chart above shows outputs from our stochastic global gas model. The scenario shown assumes a gradual resumption of Middle Eastern LNG supply from May, with full loadings from August (see previous article for further details). We run 75 simulations capturing key uncertainties such as weather, maintenance, demand variability etc to assess the distribution of winter price outcomes against end of summer storage fill.

The directional relationship is clear: lower storage pushes winter prices higher, with roughly $0.40/mmbtu of Jan-27 TTF upside per 1 bcm less gas in store at end-September. That said, the correlation is modest, with weather and subsequent demand uncertainty also key in winter price setting.

In the majority of scenarios, Europe gets through winter without significantly elevated prices relative to current futures, with global LNG supply growth providing a meaningful offset to lower European stocks entering winter. That said, the tail risk remains real, but it requires a combination of low storage and a cold winter to materialise.

One of the most important swing factors in the shape of the futures curve is how firmly the EU mandate is enforced. Running the model with a forced 80% fill constraint shifts the distribution significantly: without it, the majority of simulations fall short of the EU target, and the left tail of low storage, high price outcomes widens materially. With it, the storage distribution compresses and winter upside reduces materially, but at the cost of higher prompt prices and thus poorer injection margins.