The UK government’s announcement to abolish Carbon Price Support (CPS) from April 2028 is Labour’s first step to reduce the influence of gas and carbon costs on GB power prices — a debate brought sharply into focus by the 2022 energy crisis and ongoing Middle East tensions, which have repeatedly demonstrated the consumer impact that flows from the structural link between gas and power prices when supply shocks hit. CPS, an £18/tonne CO₂ top-up tax on fossil fuel generators sitting above the UK ETS, was originally introduced in 2013 to close the gap between low EUA prices as well as getting carbon pricing to a level sufficient to drive coal off the system, a job it has now done, with the government arguing the matured ETS can carry the decarbonisation signal alone.

We have modelled the impact using our pan-European stochastic power stack model; in our Central scenario we had already assumed CPS would ratchet down and phase out by the early 2030s, so the effect primarily manifests in the 2028–2030 window.

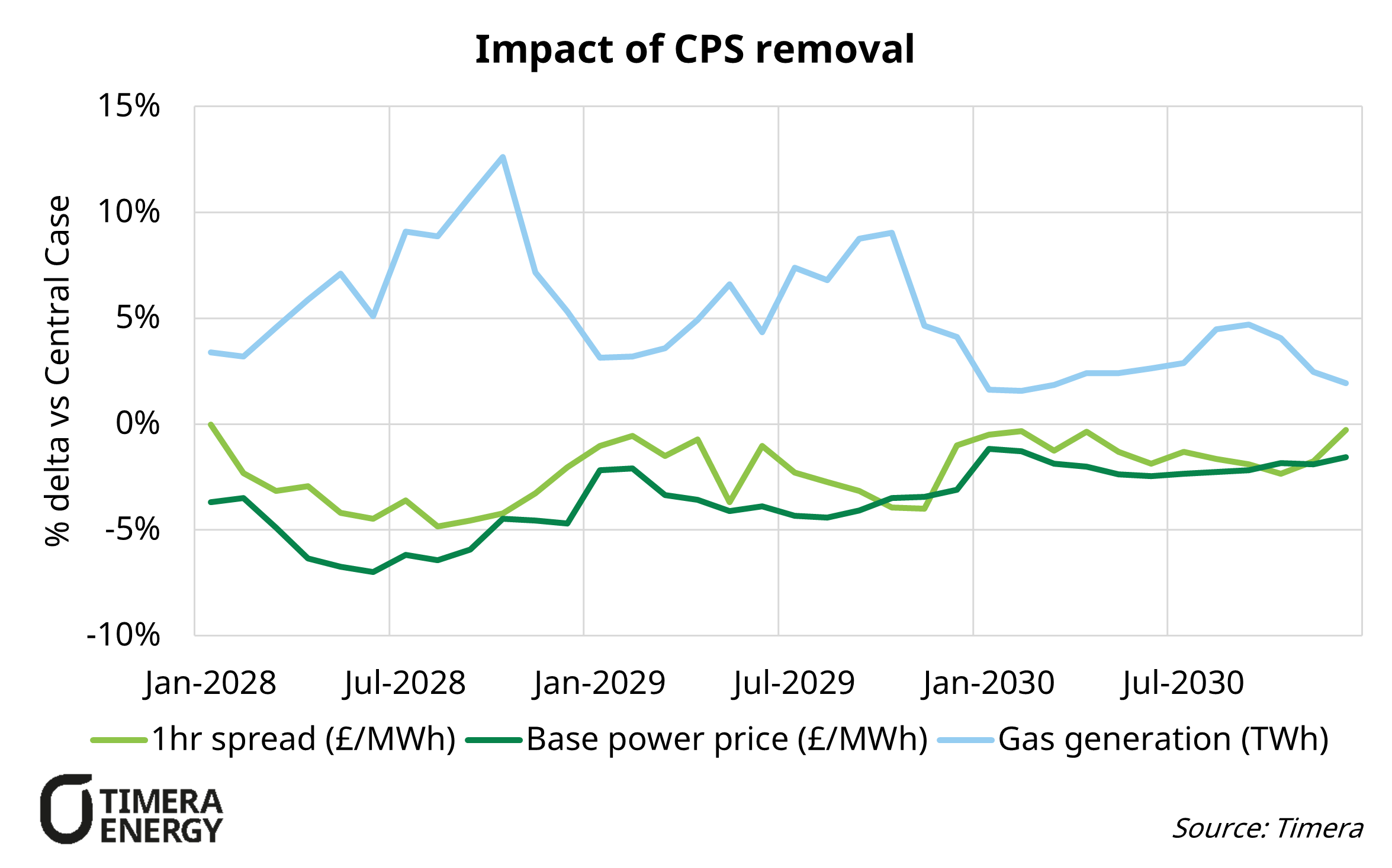

What our modelling shows

Power prices: With gas-fired generation continuing to set the marginal price across much of the late 2020s, the reduction in generator costs flows directly through to wholesale power prices, which we project to fall ~4% on average over 2028–2030 relative to our Central case.

Daily price spreads (BESS): spreads compress by ~2%, a slight headwind for merchant battery revenues, as lower the gas generation marginal cost weighs disproportionately on the sell leg.

Gas generation & interconnectors: gas generation increases by ~5%, offset by a similar TWh-scale reduction in net imports from Europe.

Clean Spark Spreads: Removing CPS reduces the operating cost of gas-fired generation and the implied impact on CSS averages an increase of ~£2.4/MWh. This is greatest in 2028 but largely erodes by 2030 as power prices reprice downward.

The bigger picture

This is unlikely to be Labour’s last intervention. The government has already confirmed an increase to the Electricity Generator Levy and is progressing voluntary CfDs, and with energy affordability remaining a live political issue, further structural interventions could occur in the future e.g. strategic reserves of gas plant capacity.

This is also not uniquely a GB story: Italy’s DL Bollette is a recent example of the same political pressure playing out across Europe, and with Middle East tensions continuing to push gas prices higher, governments across the continent are increasingly inclined to act.

How Timera can help

Quantifying the market and asset valuation impact of policy shifts like CPS removal is central to what we do. Timera’s pan-European stochastic power stack model allows clients to stress-test asset portfolios against a range of policy and market scenarios, providing a rigorous basis for investment decisions.

Our Q1 2026 BESS Subscription Services provides updated revenue stack projections and a comprehensive review of GB market policy risks and uncertainties, designed to underpin bankable investment cases.

For more information, contact Arshpreet Dhatt (Principal) arshpreet.dhatt@timera-energy.com or Steven Coppack (Power Director) steven.coppack@timera-energy.com.