Last month, Dragon LNG, a regas facility in southern UK, launched a binding capacity auction for more than 9 bcm/y of regasification capacity available from August 2029. The auction represents one of few opportunities to secure long-term primary LNG regasification capacity in Northwest Europe, with capacity available in tranches as small as approximately 1.2 bcm/y and a minimum contract term of 10 years.

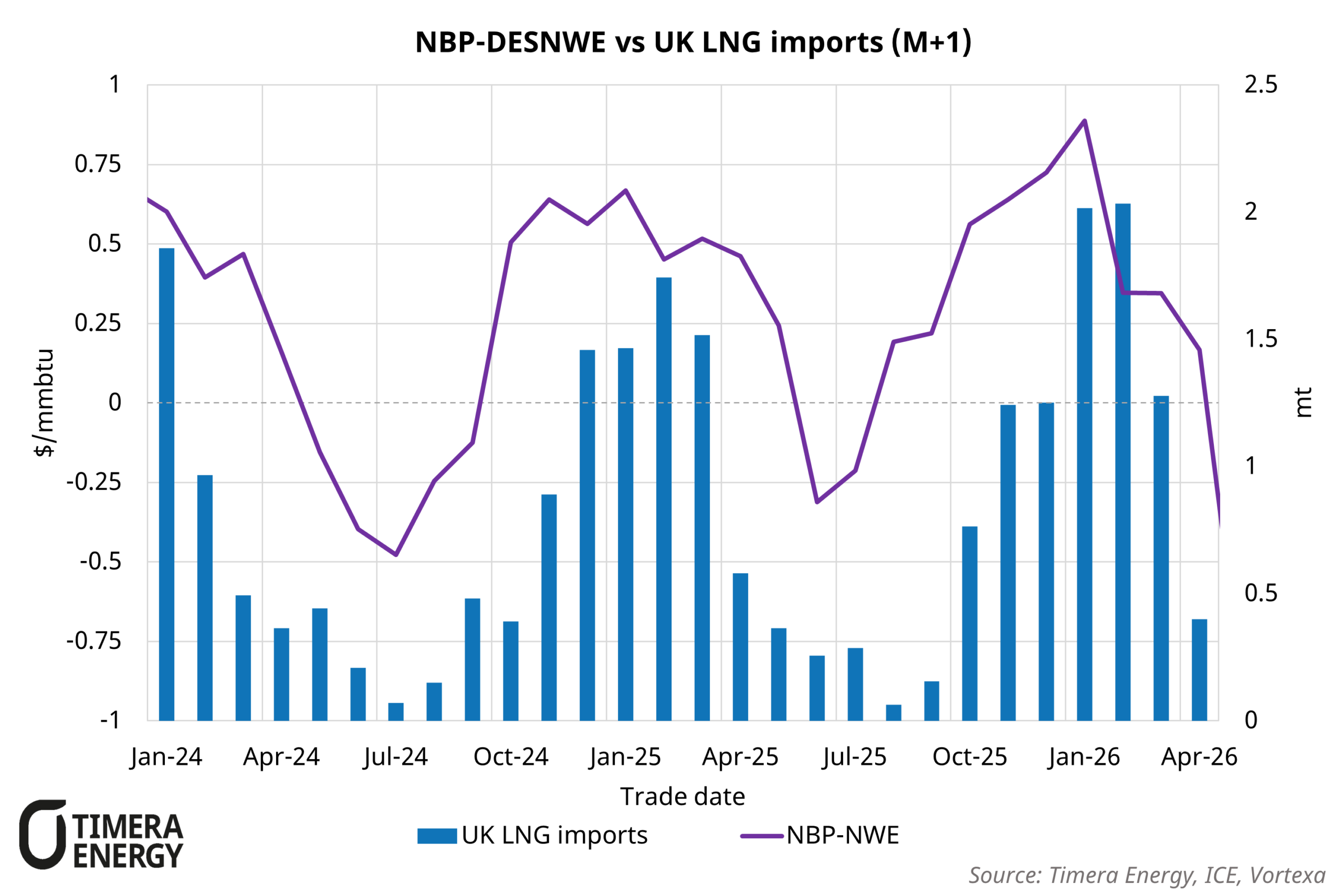

Within Europe, UK regas capacity has distinct value drivers. The GB gas market’s lack of underground storage forces LNG to play a more important role in balancing seasonal demand than in other Northwest European markets. This is reflected in steep seasonal swings in UK onshore–offshore gas spreads: regas utilisation rises sharply in winter as LNG spot cargo importers look to capture NBP prices driven higher by seasonal heating demand, before falling away in summer.

LNG imports across Europe have declined year-on-year in March and April following a sharp spike in gas prices stemming from the closure of the Strait of Hormuz, in turn weighing on regas value as capacity holders find less use for their own slots and fewer takers for unused ones. The impact has been particularly acute in the UK, with Vortexa data showing LNG imports down 20% year-on-year in March and April.

Timera provides regas auction support

We support LNG players on European market access strategy & individual opportunity evaluation. This is underpinned by (i) fundamental modelling that drives future price formation and (ii) stochastic modelling of merchant & portfolio value, using LNG Bridge.

Our support includes:

- European market access strategy

- Primary capacity auction bidding strategy & valuation

- Bilateral deal negotiation & valuation support

- M&A transaction support (market context, valuation, commercial due diligence)

For further insight, please contact our LNG & Gas Director David Duncan david.duncan@timera-energy.com.