“Storage targets are colliding with weak injection economics”

European gas storage fill is lagging behind last year’s levels, with injection rates tracking below the five-year average through the summer to date. This matters because storage remains one of Europe’s main buffers heading into winter. Lower stocks increase market exposure to cold weather, LNG disruption and price spikes if demand rises quickly.

The shortfall is being driven by two linked factors: reduced Qatari LNG supply and a backwardated (downward sloping) TTF curve. Tightness from the ongoing Middle East disruption is supporting near term summer prices. At the same time, winter prices are being weighed down by expectations of new LNG supply and some recovery in Qatari volumes later this year.

The forward curve shape is important. Storage is normally cycled with gas injection in summer and withdrawal in winter. But when winter prices sit below summer prices, there is no market price signal to inject. This creates a major challenge for Europe to reach its 80% storage fill target.

We have just released our latest quarterly near term gas market outlook. Our modelling shows storage filling to around 70–75% by the start of winter. This is the case under both (i) a Middle East De-escalation scenario and (ii) a more Sustained Disruption scenario. However, these two scenarios have substantially different market price implications.

Analysis shows why market risk is asymmetric

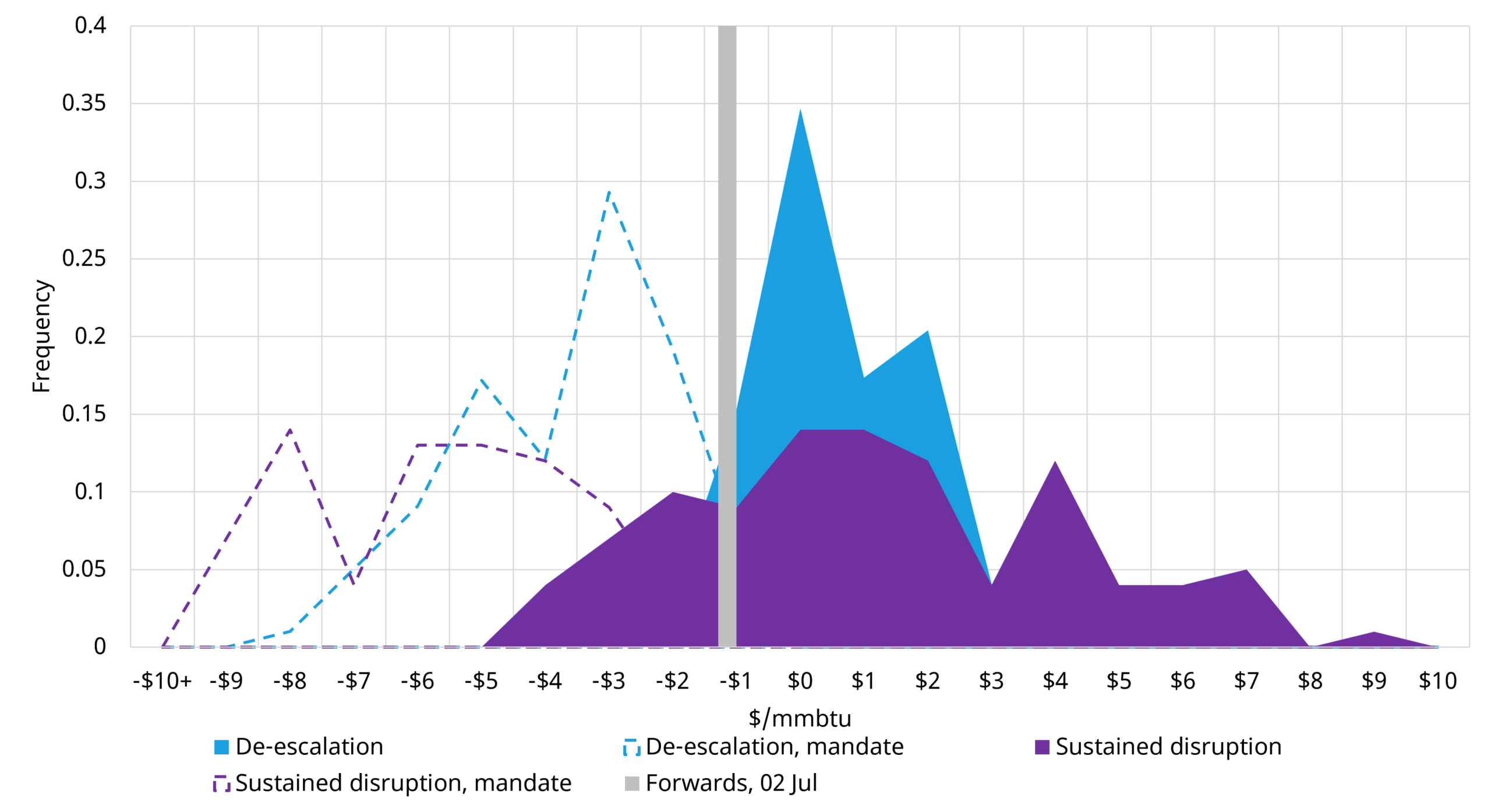

Chart 1 shows the projected distribution for the W26 – Q3’26 TTF spread under our two scenarios: De-escalation, Sustained Disruption. It also remains unclear as to how strictly European authorities will enforce storage mandates for this winter – so we consider each scenario with and without storage mandate enforcement.

Chart 1: TTF Winter-Summer price spread distribution under 2 scenarios (Q3 26 vs Winter 26)

Source: Spark, CME, Timera Energy

The current forward curve, shown by the grey bar, sits in slight backwardation. In our no-mandate De-escalation case, the mean outcome moves to a small $0.12/mmbtu contango. This reflects a market where Middle East disruption eases, LNG supply recovers and storage fill remains below the 80% target.

But the distribution around that mean remains wide. Even in the De-escalation case, weather can still move the market sharply. A cold winter would increase storage withdrawals and tighten the balance into Q1 2027.

The Sustained Disruption case shows the larger risk with a much wider distribution and stronger right tail. This captures the risk of low stocks coinciding with continued LNG supply disruption and cold weather. In those simulations, prices move sharply higher into winter as Europe has to compete harder for flexible supply. This is transmitted directly into higher global LNG prices (e.g. JKM).

The scale and timing of Qatari recovery is therefore central. The disruption has already cut Qatar’s LNG export capacity by an estimated 7–8 mt/month since March. If disruption persists into Q1 2027, Europe would need larger winter storage drawdowns, leaving lower end-winter stocks and increasing the risk that next summer starts from a weaker base.

Mandate enforcement could steepen backwardation

The policy question is what happens if Europe pushes harder to reach the 80% target. Storage mandates have already been softened to tolerate lower fill levels.

If the 80% target is enforced, injections may need to happen even when the market spread does not support them. Chart 1 shows the impact clearly. In both the de-escalation and sustained disruption cases, mandate enforcement pushes the spread into deeper backwardation than current forward levels.

In practical terms, stronger mandated injections would lift European LNG demand over summer. That would support stronger summer prices and narrower cross-basin spreads. It would also mean storage operators face a tougher commercial environment, with a greater focus in extrinsic value capture, but less winter upside risk given a stronger storage build.

Three important commercial implications are:

· Q1 2027 pricing risk is highly exposed to supply recovery: Qatari recovery,the pace of the new LNG supply wave and stock levels are key drivers of late-winter pricing risk.

· Storage value is shifting away from simple seasonal spread capture: in a backwardated market, value capture is focused on volatility, optionality and deliverability.

· Portfolio flexibility is increasingly important: the broad spread of outcomes in Chart 1 highlights the value of e.g. destination flexibility, diversion rights and timing optionality across Gas & LNG portfolios.

Our latest near term gas market outlook helps clients quantify these risks across storage, LNG and portfolio exposure. To discuss the scenarios behind the outlook, contact Luke Cottell, Associate Director (luke.cottell@timera-energy.com).