8-11% BESS structural revenue uplift today from congestion in Scotland… but with major risks in play

Backward-looking revenue indices are a useful gauge of how GB BESS are doing. They show what assets are actually capturing and help benchmark relative performance. But strong historic revenues don’t always translate into forward-looking value. This is particularly true in the case of BM congestion revenue uplift.

In today’s article we focus on Repetitive Re-Trading (RRT) as a BESS value driver and the risks around value erosion. RRT is where a storage asset behind a transmission constraint keeps re-selling the same power as the system operator (NESO) repeatedly bids it down.

RRT is an important source of storage asset revenue today, but it faces some major policy risks going forward.

Value capture will evolve with asset trading strategy

One big reason for a breakdown between historical and future returns is trading strategy. A lot of the value captured today comes from optimisers exploiting inefficiencies in current market design – through routes such as Virtual Trading Party (VTP) registration, legacy ancillary services, and Repetitive re-trading (RRT) behind constraints.

There is nothing wrong with this; a good optimiser should work every option the market rules allow. The question for investors is whether value capture is structural or transitional, and how much survives the next round of policy reforms.

Ofgem’s 19 June publication put the balancing-cost impact of RRT at around £99m in FY25/26, up from £64m the year before. That is a substantial cost to the consumer that may trigger policy reform to curtail the strategy at short notice. It is a clear example of why separating bankable congestion value from riskier upside matters.

How Repetitive re-trading (RRT) works

An asset schedules its export based on national wholesale prices, which do not reflect local constraints. When constraints are active, the system operator (NESO) bids the asset down.

Because every curtailed MWh frees up capacity, the asset can re-sell the same power later, and the cycle can repeat until the constraint clears as shown in the animation in Chart 1.

Chart 1: Animated illustration of RRT

Source: Timera

As such the asset can worsen the constraint rather than resolving it, while NESO pays replacement generation elsewhere to cover the gap.

Pumped storage (PHES) drives most of the RRT balancing cost today, but the BESS share is climbing fast as more capacity sits behind constraints.

Crucially, Ofgem has made clear that RRT itself is not a breach of the Transmission Constraint Licence Condition (TCLC), the key regulation on generators behind constraints. The licence condition only governs bid pricing in constraint periods, prohibiting operators from securing an excessive benefit from being bid down.

Options for policy reform and their value impact

Despite RRT not breaching the current market rules, the scale of consumer cost means NESO is now weighing a range of options to reduce RRT related costs. We set out several of these in Table 1.

Table 1: Policy options to address RRT

*NESO is currently working on potentially splitting the GB ancillary procurement across 12 zones in GB to ensure capacity is contracted with units who do not face constraints in delivering the services.

Some of these options could significantly disrupt how storage operates in the markets today. They risk having the effect of turning ownership of storage in a congested area into a relative penalty, if assets can no longer trade against genuine national price signals.

Given this risk to the storage business case, and the potential for stranded assets, it remains to be seen whether any of these proposals are adopted. But quantifying risk and value impact is important for BESS asset owners & investors.

Underlying congestion value capture vs RRT uplift

Constraints drive additional value for storage assets such as BESS and pumped hydro (PHES) in Scotland. Repetitive re-trading enhances that value, but even if the strategy is reined in, a base level of congestion value capture would remain. That underlying value is central to the Scottish business case, particularly given the higher transmission network charges (TNUoS) that assets in the region face.

Our analysis of current Scottish BESS value capture shows a meaningful slice of congestion revenue achieved by some assets today is attributable to RRT-type strategies rather than to the underlying constraint.

The fundamental, structurally-driven component of congestion value is the part that can be considered bankable. The rest should be modelled as upside that can be removed at short notice with regulatory reform.

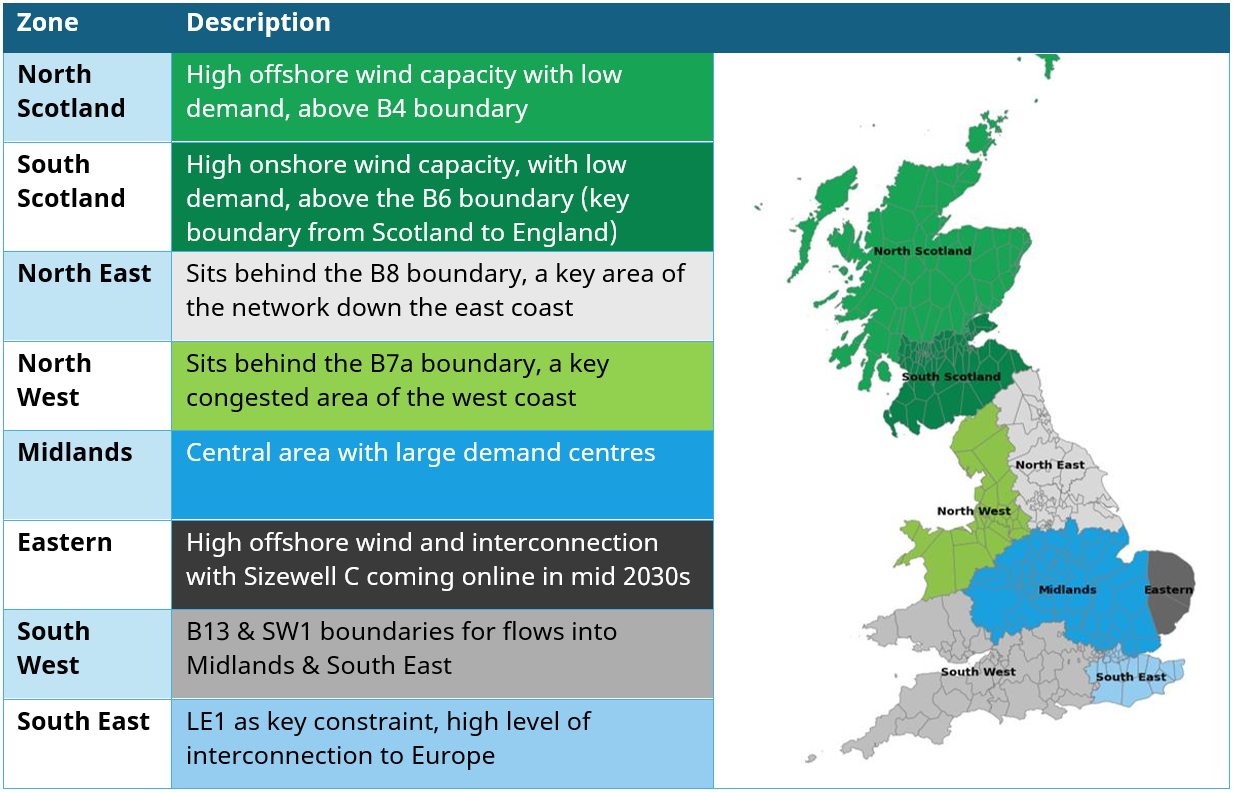

Analysis of GB BESS congestion value capture

At Timera we have built our own stochastic modelling suite for congestion. It uses our proprietary pan-European market model, configured with the key constraint boundaries in GB as set out in Table 2.

Table 2: Key GB transmission constraint boundaries

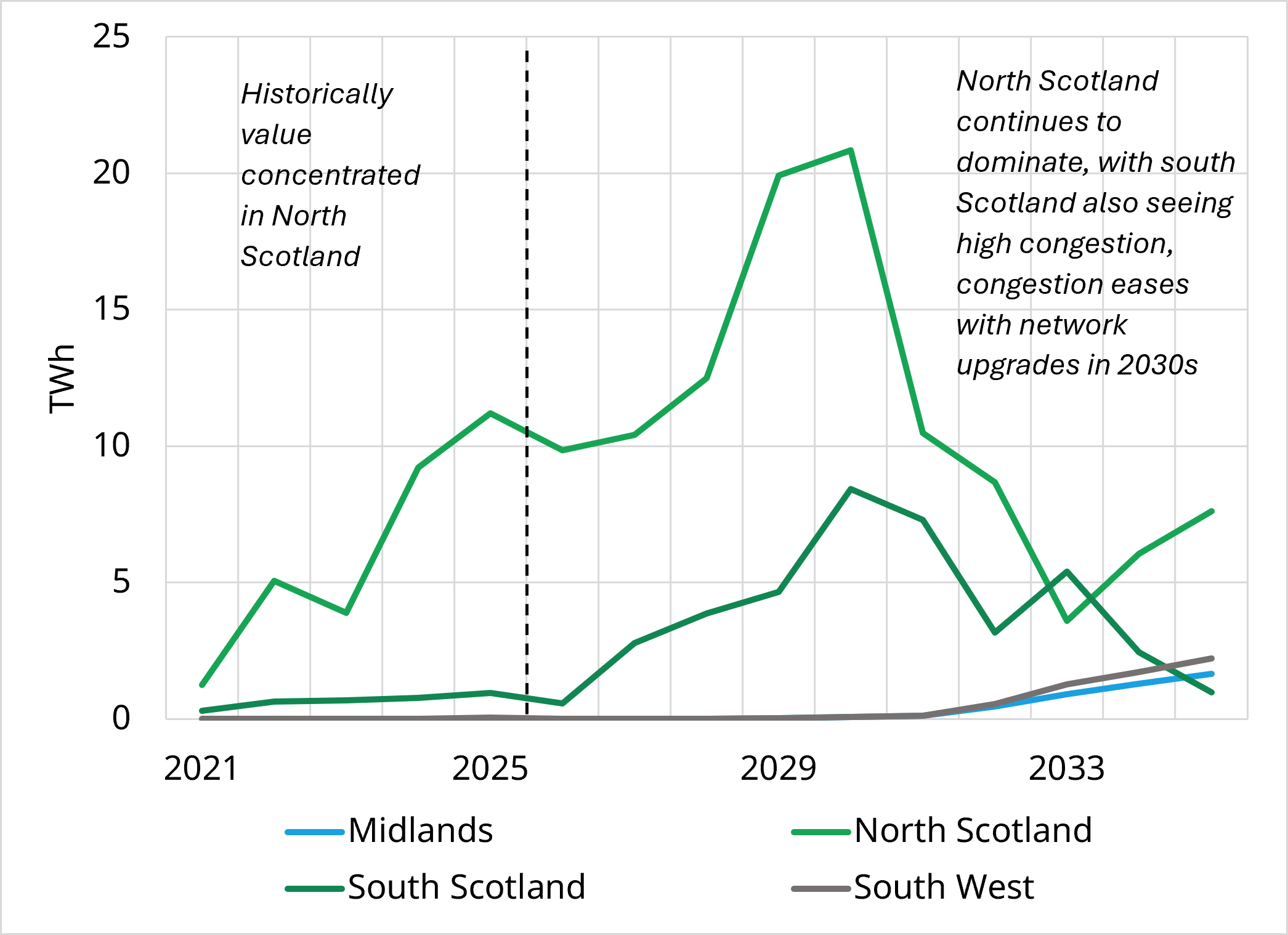

Using this we model how bid and offer activity evolves over time as network capacity changes, across hundreds of different simulations of weather and demand profiles. Chart 2 shows an illustrative scenario of projected constraint volumes across some selected boundaries.

Chart 2: Illustrative scenario of projected thermal constraint volumes in some zones

Source: Timera, NESO

Moving from congested volume (TWh) to asset value uplift is the next step, and it requires modelling of:

- The bid stack and how it evolves. As older RES contracts (ROCs, legacy CfDs) expire, deeply negative bids become less common – even without code-mod reform.

- A sustainable BM bidding strategy. One that is TCLC-compliant and holds up over a multi-year horizon, not just a favourable window. More aggressive strategies are upside, but carry regulatory-breach risk.

- Value capture that doesn’t rely on RRT. Revenue dependent on continuous re-trading carries significant risk – NESO is already weighing measures to curb it.

- Competition from other assets, including LDES via the cap and floor scheme, which reshapes the merit order in each zone.

The output of this modelling process is asset specific value uplift that can be split between structural underlying congestion value and RRT related uplift.

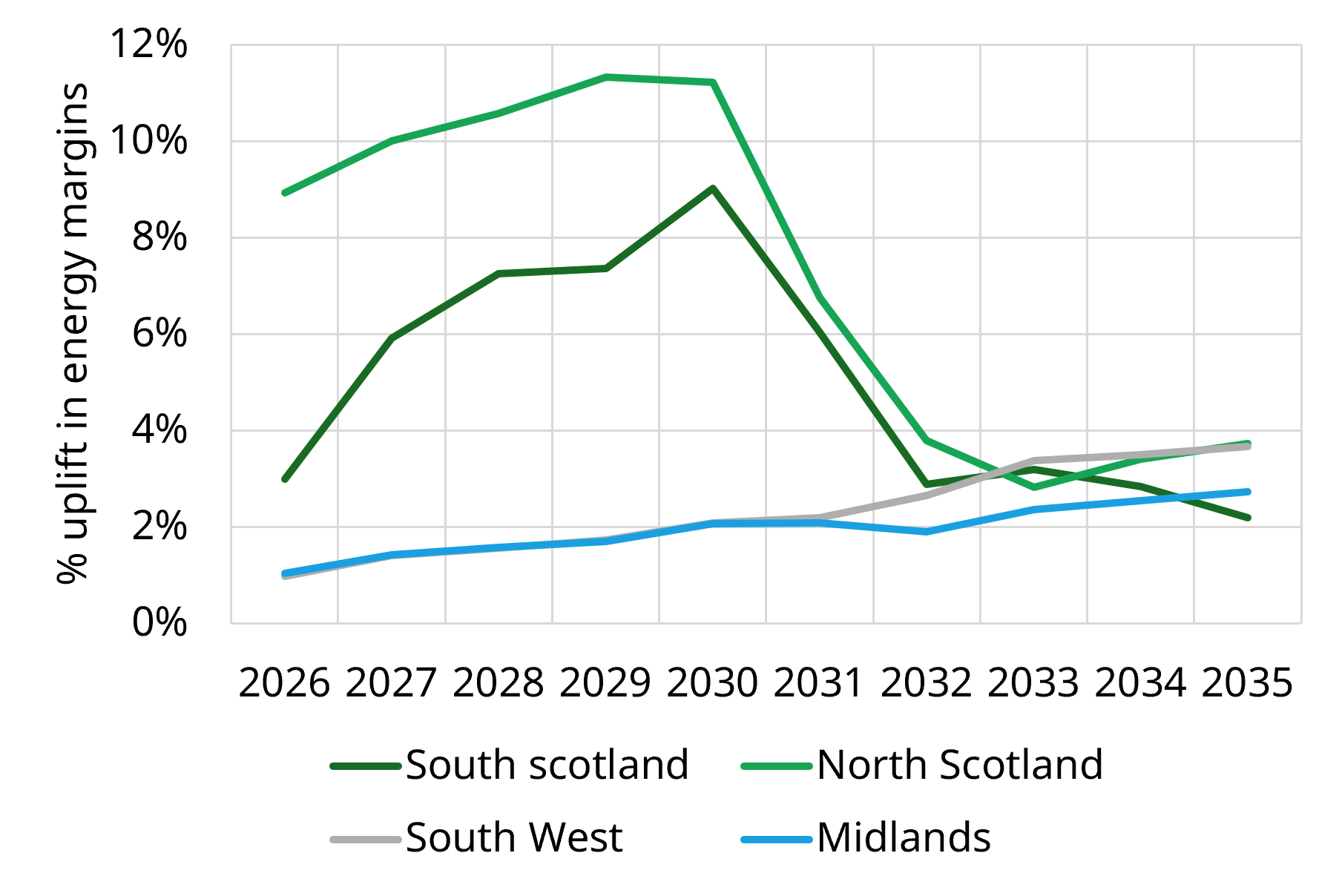

Margin uplift from congestion rents

Let’s talk numbers. Chart 3 shows percentage uplift in BESS energy margins from BM congestion revenues for some example zones. Analysis is based on an illustrative market scenario with hundreds of simulations of load, wind & solar profiles – to capture a full distribution of congestion value capture.

Chart 3: BESS energy margin uplift from BM congestion rents (2 hr duration)

Source: Timera

The headline takeaway is that North Scotland and South Scotland can achieve an uplift of up to 8 to 11%, even without RRT strategies or aggressive bidding in the BM. However, that uplift is at risk of eroding quickly through the 2030s as competition builds and network upgrades come through. That means assets coming online over the next few years stand to gain the most.

Our modelling framework enables us to layer on sensitivities such as delays to network upgrades, changes in RES build, or demand growth.

This matters not only for BESS but also for PHES & LDES assets, given congestion value capture is typically higher for longer duration assets. With LDES cap and floor scheme results due soon, this will be a core area to analyse for assets being developed in Scotland.

The result is a bankable view of congestion value to inform locational strategy, treating trading strategies such as RRT as additional upside rather than guaranteed uplift.

How can Timera help?

We have supported many clients on system BM modelling and sensitivities, including the impact of RRT and P462, alongside wider locational strategy work spanning congestion, network charges and grid connections.

We will soon release our Q2-26 update of our GB BESS revenue curves, which includes full congestion modelling as set out above. For our views on the GB market for storage or any other flexible assets, please reach out to Arshpreet Dhatt, Principal (arshpreet.dhatt@timera-energy.com).