Ofgem has published its minded-to decisions for ‘Window 1’ of the GB long duration electricity storage (LDES) cap & floor scheme. It lists 16 projects totalling 7,645 MW, with final awards due Autumn 2026. It gives the first, provisional signal as to which technologies, durations and locations the scheme will back.

Under the cap & floor scheme, consumers top up operators’ revenues to a guaranteed floor price and are paid back anything above a pre-determined cap price, essentially trading downside protection for capped upside to make high-capex, long-build LDES investable.

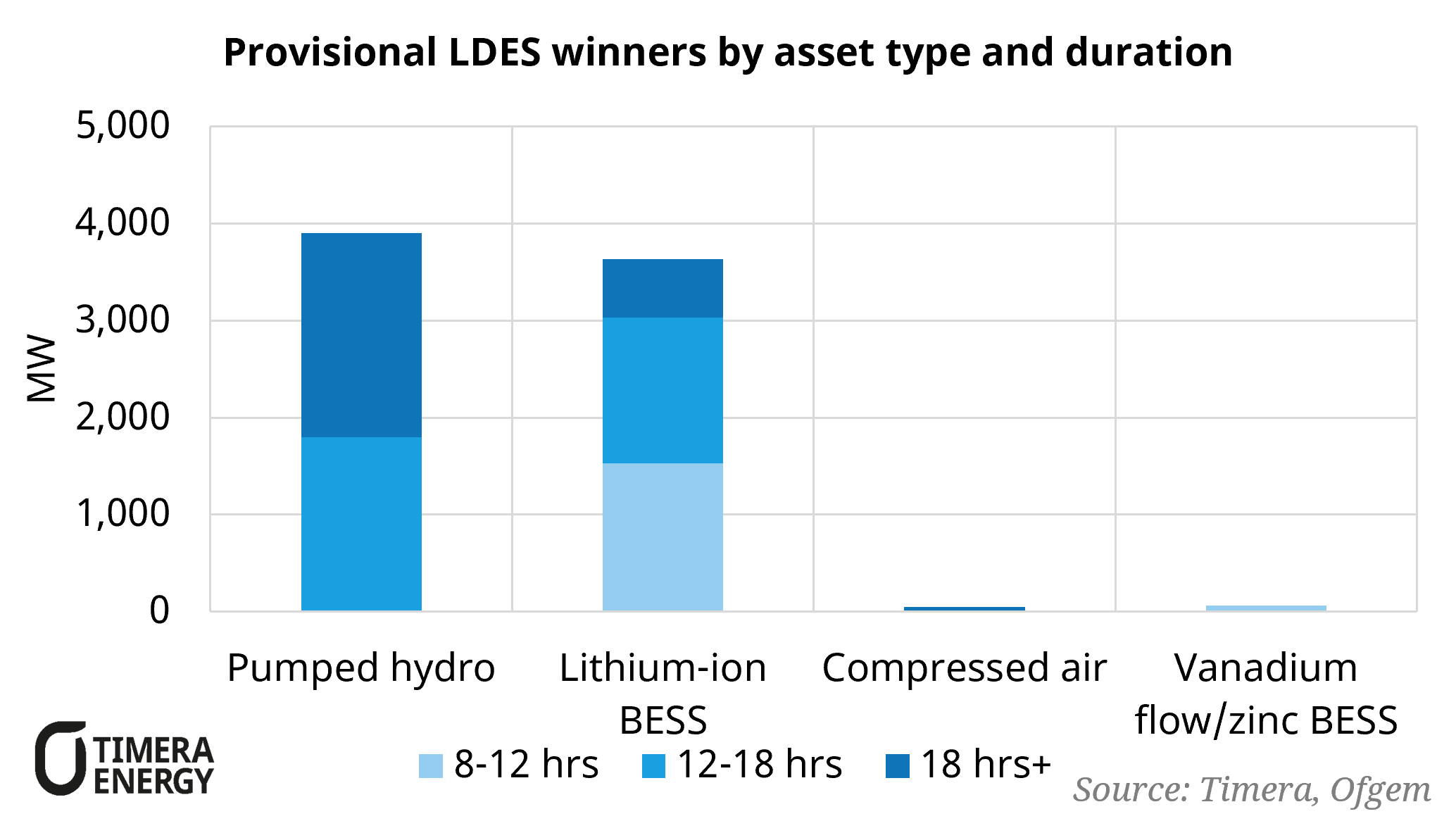

Li-ion BESS wins on number of projects, pumped hydro on capacity. Based on number of projects alone, Li-ion BESS dominates, making up 11 of the 16 winners. By capacity, however, three pumped hydro projects (Earba (1,800 MW), Coire Glas (1,440 MW) and Loch Kemp (660 MW)) constitute 51%, with compressed air (TeesCAES, 50 MW) and a vanadium flow/zinc battery (Frontier Legacy, 65 MW) rounding out the mix. Five of the 11 Li-ion BESS projects have durations beyond 15 hours, territory long dominated by pumped hydro. At roughly 3,630 MW, the awarded BESS capacity runs ahead of our in-house build view for the window, while the ~3,900 MW of PHES sits broadly in line with our projections.

Delivery risk has been pushed downstream. Ofgem ranked projects on economic, strategic and financial merit, with deliverability one input rather than the sole decider. The 7,645 MW total sits just below the upper limit of NESO’s advised range (7,700 MW) as Ofgem states that the gap “provides headroom for a reasonable degree of attrition”. Planning, grid connection and supply chain are therefore live concerns, particularly for those assets which hold only Gate 1 offers from NESO and will need to progress through the updated Gate 2 process before connecting to the grid and being able to participate in the scheme.

North Scotland is the winner, focussing on soaking up excess RES rather than displacing thermal turn up. Roughly three-quarters of the list sits in North Scotland, including all three PHES schemes and four Field BESS assets. Sited there, LDES capacity is well placed to soak up surplus wind that would otherwise be curtailed and to earn related uplift in the Balancing Mechanism on top of wholesale spreads. However, this does not help to alleviate the more expensive congestion issue, namely paying thermal generators to turn up to meet demand in the south.

For investors entering future auctions, robust stochastic LDES modelling, capturing renewable patterns, demand dynamics, correlated price volatility and system constraints, is essential to quantify risk-adjusted value. Timera’s in-house modelling suite is purpose built for exactly this; to discuss LDES or other flexible assets, contact our Power Director Steven Coppack (steven.coppack@timera-energy.com).